“What is perfection in love? Love your enemies in such a way that you would desire to make them your brothers … For so did He love, Who hanging on the Cross, said ‘Father, forgive them, for they know not what they do.’” (Luke 23:34)

All

The Real Debt Problem

The Real Debt Problem

Paul Craig Roberts

Someone sent me an article from something called Patriot Alerts, “Morgan Stanley Sounds Alarm On ‘Death Of US Dollar.’”

The death of the US dollar is not blamed on the Federal Reserve printing trillions of new fiat currency during the years of Quantitative Easing in order to bail out the difficulties of the 5 large banks. It is not blamed on the thoughtless US sanctions imposed on Russia, Iran, and other countries, the only effect of which is to encourage countries to abandon the dollar based system, thus causing a drop in the demand for dollars and US Treasury debt.

Instead, the dollar’s peril is blamed on Russia, China, Iran, “oil-soaked Saudi Arabia” and “our neighbor Mexico.” In other words, it is a cover-up for the Fed and Biden regime’s catastrophic mistakes.

It turns out that the report is nothing but an advertisement for how to protect your pension and bank accounts by obtaining a copy of “US Dollar Collapse Guide.”

This marketing nonsenses provoked me to write this article.

As I have made crystal clear in my 4-Part series “The Great Dispossession,” you have already lost ownership of your banking, pension, and investment accounts. Your “ownership” has been reduced to permission to use your assets until the financial intermediary holding them gets into financial trouble. At that moment, they cease to be your property and become the property of the creditors of the intermediary that holds your accounts, whether it be Merrill Lynch, Schwab, Wells Fargo, TIAA, or whoever. Your dispossession was done quietly over many years by regulatory agencies. This is what Klaus Schwab of the World Economic Forum means when he tells you that “you will own nothing.” You already don’t.

The US dollar is in trouble, but it is trouble of Washington’s making. Republicans and the financial press, to the extent that one still exists, blame the dollar’s trouble on rising public and private debt. The US runs massive trade and budget deficits. These deficits for decades have been alleged to mean the death of the dollar. The narrative was that the dollar would be weakened by having to finance rising trade and domestic debt. When I was in the Congressional staff and later as Assistant Secretary of the US Treasury for Economic Policy, I had to deal with this ignorance, and it was frustrating. No one in Congress, on Wall Street, in the banks, or in the economics departments of universities understood the meaning of the US dollar as reserve currency.

When a country’s currency is the reserve currency, a role the US seized from Great Britain as its World War II victory prize, it means that there is unlimited demand for your debt. The reason is that your debt is the reserves of the world’s central banks. An increase in US debt is an increase in the reserves of the world banking system. As central banks desire more reserves, there was always a demand for US Treasury debt. There was zero financing problem.

All of the nonsense we heard for decades about the impossibility of paying off the US debt was unbridled ignorance. The debt did not need to be payed off. If it had been, the reserves of the world banking system would have collapsed, and the Great Depression that the Americans experienced in the 1930s, due entirely to the Fed’s failure to expand bank reserves, would be worldwide.

Being the world currency, a role Roosevelt stole from England, means the US can pay its international bills by printing money or issuing debt.

What has put this American privilege in danger is Washington’s stupid, indeed mindless, imposition of economic sanctions that then are evaded by ceasing to use the US dollar as world money. When countries cease settling their international balance of payments accounts in dollars, as Russia, China, Iran and other countries are doing, demand for Treasury debt drops. This means as the sanctioned central banks move to gold and non-Western currencies as reserves, that the demand for US Treasury debt drops, and for the first time in recent history, financing America’s tremendous public debt becomes a problem.

To be completely clear, the ONLY reason the US dollar is in danger of a large reduction in its value, is that Biden’s sanctions are driving countries away from the dollar. US debt can become a problem only from the abandonment of the dollar as world money. As US debt is denominated in US dollars, the Federal Reserve can always pay off the US debt no matter how large it is by printing money and buying the bonds.

The problem is not that the debt can’t be paid. The problem is whereas the Fed can print dollars to meet any debt payments, it cannot print foreign currencies with which to buy dollars in foreign exchange markets. When US Treasury debt is redeemed, the debt holders (largely foreign central banks) receive dollars. If they have lost confidence in the dollar, they sell the dollars in the currency markets, and the enormous supply of dollars drive down its value.

When the dollar’s value is driven down, the offshored production of American firms, who produce in Asia and Mexico the products they sell to Americans and which comes in as imports, rise in price, thus causing domestic inflation, reducing the dollar’s purchasing power and causing more exit from the dollar.

In other words, it is a death scenario–one produced by the Federal Reserve, the incompetent or bought-and-paid-for American economists, a mindless American government, and the mindless financial press.

The minute the dollar goes, American power goes with it.

Most of the world can hardly wait for it to happen.

Fighting to the Last Ukrainian

Fighting to the Last Ukrainian

Paul Craig Roberts

Ukraine has lost almost half a million troops

https://www.rt.com/russia/596458-ukraine-lost-almost-half-million-troops-shoigu/

And it looks like US/UK/EU “aid” packages will cost Ukraine another half-million soldiers. https://www.rt.com/news/596436-uk-largest-ever-military-aid-ukraine/

The UK PM justifies the destruction of Ukraine with this mindless reason: “Defending Ukraine against Russia’s brutal ambitions is vital for our security and for all of Europe. If Putin is allowed to succeed in this war of aggression, he will not stop at the Polish border.”

Why is the UK PM lying through his teeth? Or is it possible that he really is completely stupid? No intelligence agency anywhere has provided a scrap of evidence that Russia has an expansionist policy toward Europe. Moreover, as the Russian government has repeatedly made clear by words and deeds, there is no Russian invasion of Ukraine. There is a limited military operation to clear Ukrainian forces out of the Russian populated territories that seceded from Ukraine after the US coup that overthrew the Ukrainian government and installed an anti-Russian government that persecuted Ukraine’s Russian population. Everyone knows this, but the West pretends it is an invasion.

It is the US, UK, and EU that are turning a limited operation into a general war. Putin did not realize that this would be the consequence of his limited operation. Putin misjudged the West and blundered. He should have knocked out Ukraine immediately and got it over before the West had time to intervene.

So, who is destroying Ukraine? Russia or the West?

American Police Behaving as Israeli Enforcers Continue to Discredit Themselves

American Police Behaving as Israeli Enforcers Continue to Discredit Themselves

https://www.rt.com/news/596449-propalestinian-protest-new-york-university/

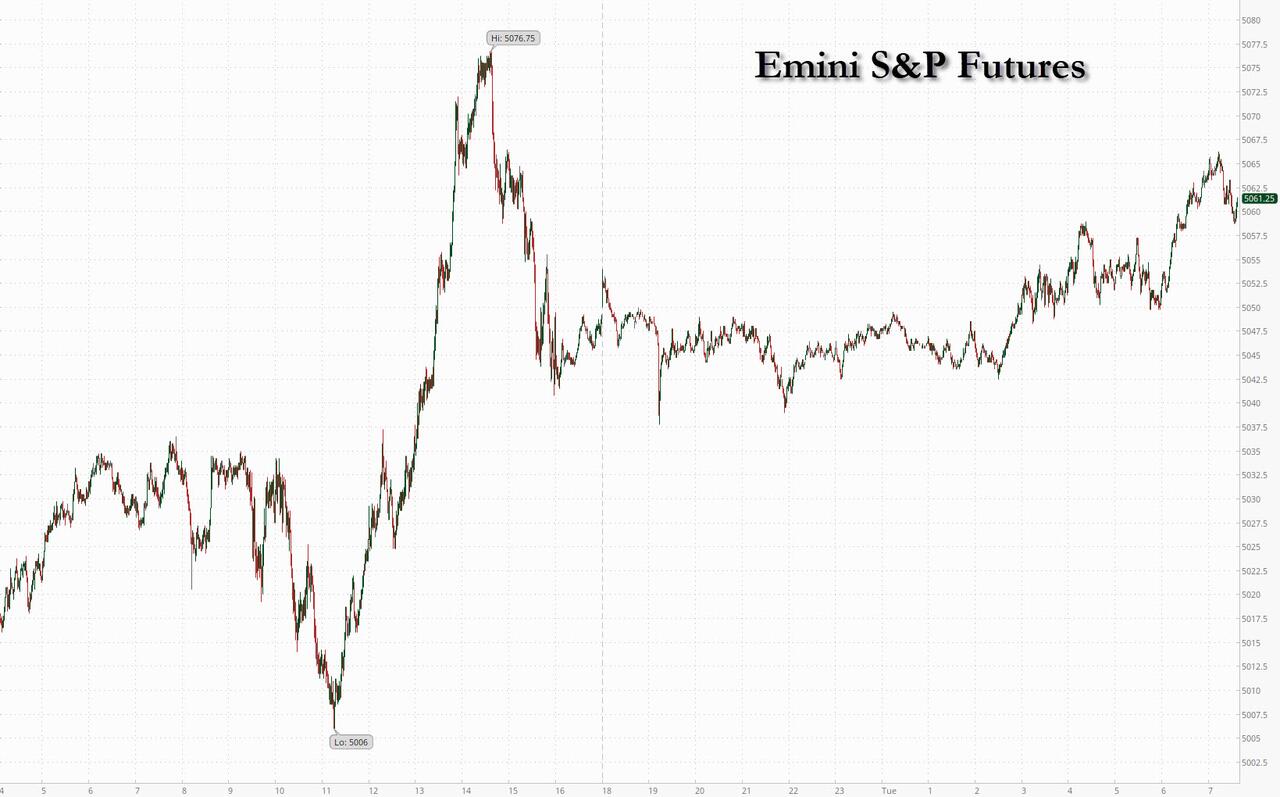

Futures Extend Rebound Into Second Day Ahead Of Tesla Earnings Despite Rising Yields

Futures Extend Rebound Into Second Day Ahead Of Tesla Earnings Despite Rising Yields

Tyler Durden

Tue, 04/23/2024 - 08:19

US equity futures are higher for the second day, even as small-caps underperform after bond yields rise about +4bps and trade near session highs. As of 7:40am S&P and Nasdaq futures were 0.3% higher after Wall Street’s rebound from a $2 trillion selloff; European stocks also rose on broad-based strength, with only commodity-related sectors in the red; the UK’s FTSE 100 index hit a record high as a rebound that took hold on Monday gathered momentum. Ahead of Tesla's earnings today, the Mag7 are mixed with semis higher pre-mkt after the recent rout. Commodities are stronger led by Ags and Energy with a flat USD. The macro data focus is on Flash PMIs, Home Sales, Regional Mfg Activity indicators; earnings are skewed towards the Industrials sector with TSLA the first Mag7 stock set to report. We will see if the last few trading sessions sufficiently squared positions and if realized stock moves can match the implied moves, expected to be the largest in 1.5 years.

Early results Tuesday were mostly positive, with shares of United Parcel Service and General Motors rising in premarket trading after earnings beats. PepsiCo slipped after reporting falling volumes in North America. But the main event will be the “Magnificent Seven” cohort of tech megacaps, with Tesla set to be the first to report after today’s market close. Next up is Meta Platforms on Wednesday, followed by Microsoft and Alphabet on Thursday. Here are some other notable premarket movers:

- Abeona Therapeutics shares slumped 48.1% after the biotechnology company’s drug for a rare connective tissue disorder failed to win approval from the US Food and Drug Administration.

- Cadence Design shares drop 5.8% after the maker of semiconductor design software’s revenue and adjusted earnings per share forecast for 2Q fell short of average analyst estimates. Additionally, the company reported 1Q product and maintenance revenue that missed expectations.

- JD Sports shares gained after the British sportswear and sneakers retailer agreed to buy Hibbett (HIBB US) for about $1.1 billion to speed up its US expansion, in a deal expected to be accretive in the first full year of ownership. Hibbett gained 19%.

- Roblox shares rose 4.2% after the game maker was upgraded to overweight from neutral at JPMorgan, which said it sees a “compelling” entry point for a company that has bookings growth of around 20%, exiting a heavy investment cycle and ramping new revenue streams in advertising as well as commerce.

- Sunnova Energy shares fell 2.4% after the renewable energy company is cut to sector weight from overweight by KeyBanc Capital Markets. The downgrade reflects a cautious industry-wide stance, despite Sunnova’s “undemanding valuation,” analyst Sophie Karp writes in a note.

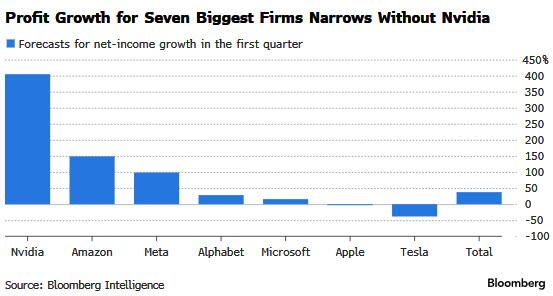

Earnings will stay front and center of investors’ minds this week with about 180 companies — over 40% of the S&P 500 market value — report results. The focus on corporate profits comes after a rout fueled by geopolitical fears and signals the Federal Reserve will be in no rush to lower rates. "Whether markets see further consolidation from here is likely to hinge on the assessment of the sustainability of AI demand ahead following the earnings releases," said Eddie Cheung, a senior strategist at Credit Agricole CIB.

The challenge to S&P 500 returns is that companies will have to produce earnings, and outlooks, that support the already elevated multiples. Profits for the Magnificent Seven are forecast to rise 38% in the first quarter from a year ago, dwarfing the overall S&P 500’s 2.4% anticipated year-over-year earnings growth, according to Bloomberg Intelligence. But excluding Nvidia, the leading chipmaker for AI technology, expected net income growth for the group falls to 23%. Nvidia, which Goldman Sachs Group’s trading desk dubbed “the most important stock on planet Earth,” doesn’t report its earnings for another month.

“We remain focused on the current earnings season, which could re-focus investor attention on solid underlying fundamentals,” Citigroup Inc. strategists Mihir Tirodkar and Beata Manthey wrote in a note. “We would view the recent pullback as a buying opportunity."

Meanwhile, Investor positioning on megacap growth and tech stocks continues to be cut, down from the 97th percentile in early March to the 77th percentile now, according to Deutsche Bank strategists. The group is still the only sector where positioning is above historical average, even if no longer extreme, the strategists wrote, countering the self-serving and incorrect observations by JPM's Marko Kolanovic.

In Europe, the Stoxx 600 index climbed 1%, with technology and retail shares leading gains, while the mining sector lagged. SAP SE jumped more than 4% as a boom in demand for artificial intelligence fueled the German software company’s growth. Drugmaker Novartis AG added as much as 5% after lifting full-year guidance. Here are some other notable premarket movers:

- JD Sports shares gain as much as 7.5% after the British sportswear and sneakers retailer agreed to buy Hibbett for about $1.1 billion to speed up its US expansion

- Novartis shares advance as much as 5%, the most in more than 9 months, after the Swiss drugmaker reported results for the first quarter that impressed analysts

- Nordnet rises as much as 9.7%, the most since October, after the digital bank reported its first-quarter results. Both Citi and Morgan Stanley highlight the company’s higher-than-expected brokerage income

- SAP shares jump as much as 4.4% in Frankfurt after the software company reported quarter-over-quarter acceleration in the growth rate of current cloud backlog, a key indicator of cloud revenue to be booked within next 12 months

- Akzo Nobel shares fall as much as 6.6%, to the lowest since November, after the coatings maker failed to raise its profit forecast for the year. The stock had risen in five of the six sessions leading up to Tuesday’s earnings report

- DNB falls as much as 3.9%, the most since October, after the Norwegian lender reported a net interest income miss for the third quarter in a row, with analysts also flagging a low-quality profit beat due to it being attributable to provision income

- Anglo American falls as much as 3.9% in London after the miner reported first-quarter earnings. Analysts noted that sales were behind production in copper and iron ore, leading to temporary inventory builds

- Kuehne + Nagel shares drop as much as 3.9% after reporting first-quarter earnings in which pricing and cost performance were offset by lower volumes, according to Citigroup

- Boliden declines as much as 5.9% after its first-quarter results, with analysts flagging that headline operating profit missed, but underlying operations performed reasonably well

- OVH shares slide as much as 17%, the biggest drop since March 2023, as weaker-than-expected 2Q growth led the IT services provider to lower its forecast for growth and capex for the year

PMI data on Tuesday reinforced the positive mood in Europe. Private-sector activity advanced to the highest level in almost a year, driven by a buoyant services sector and Germany’s return to growth. And yet, barring any economic surprises, a rate cut in June is a “fait accompli,” European Central Bank Vice President Luis de Guindos said.

Earlier in the session, Asian stocks also rose for a second day as sentiment toward China continued to improve, with easing fears of a wider Middle East conflict offering additional support. The MSCI Asia Pacific Index rose as much as 0.8%, with TSMC and Tencent among the biggest boosts. Most regional markets advanced, though mainland China stocks fell for a third day and Japanese shares trimmed gains as the yen strengthened after Finance Minister Shunichi Suzuki’s comments on possible intervention. Hong Kong stocks led the region’s gains after UBS upgraded Chinese stocks to overweight, citing resilient earnings and a growing focus on shareholder returns. Investors are turning more upbeat on the nation’s assets thanks to green shoots in the economy as well as signs of improving corporate performance.

- Hang Seng and Shanghai Comp. were mixed with outperformance in Hong Kong due to tech strength, while the mainland lagged amid the PBoC's continued tepid liquidity operations and with the US drafting sanctions that threaten to cut some Chinese banks off from the global financial system for aiding the Russian war effort.

- Nikkei 225 traded indecisively and on both sides of 37,500 after briefly wiping out all of its opening gains.

- ASX 200 was led by strength in real estate and tech, while the latest flash PMIs from Australia were varied.

“What makes us more positive now on earnings are the early signs of a pick-up in consumption,” UBS strategists including Sunil Tirumalai wrote in a note. “Any rebound in consumer confidence for us means the possibility of household savings flowing into consumption” and eventually markets.

In rates, treasuries are under modest pressure with front-end yields higher by ~2bp before a flurry of bond auctions that will test investors’ appetite after yields hit the highest in 2024: the latest weekly supply cycle (2-, 5- and 7-year auctions) is set to kick off with record $69b 2-year later today. US 10-year yields around 4.645%, higher by nearly 4bps on the day. In Europe, gilts underperform their German counterparts after the UK raised its planned gilt issuance for the fiscal year more than expected, as the government’s budget shortfall overshot forecasts; the belly of gilts curve cheapened after DMO announcement, with 5-year UK yields higher by around 2bp. Treasury coupon auctions resume at 1pm New York time with $69b 2-year, followed by 5- and 7-year notes Wednesday and Thursday. The WI 2-year yield at around 4.965% is ~37bp cheaper than last month’s, which tailed by 0.5bp

In commodities, oil prices advance, with WTI rising 0.4% to trade near $82.20. Gold extends Monday’s drop, down 1% on the day; Monday’s 2.7% drop was biggest in nearly two years. Bitcoin is modestly softer and holds around the USD 66k mark.

Looking at today's calendar, US economic data slate includes April Philadelphia Fed non-manufacturing activity (8:30am), S&P manufacturing and services PMIs (9:45am), March new home sales and April Richmond Fed manufacturing index (10am). From central banks, we’ll hear from the ECB’s Panetta and Nagel, and the BoE’s Haskel and Pill as Fed members have entered quiet period ahead of May 1 policy announcement. Finally, today’s earnings releases include Visa, Tesla, PepsiCo, General Electric, UPS and General Motors.

Market Snapshot

- S&P 500 futures up 0.1% to 5,052.75

- STOXX Europe 600 up 0.6% to 505.15

- MXAP up 0.6% to 170.25

- MXAPJ up 0.9% to 524.40

- Nikkei up 0.3% to 37,552.16

- Topix up 0.1% to 2,666.23

- Hang Seng Index up 1.9% to 16,828.93

- Shanghai Composite down 0.7% to 3,021.98

- Sensex up 0.3% to 73,852.66

- Australia S&P/ASX 200 up 0.4% to 7,683.51

- Kospi down 0.2% to 2,623.02

- Brent Futures up 1.0% to $87.85/bbl

- Gold spot down 0.9% to $2,305.32

- US Dollar Index down 0.14% to 105.93

- German 10Y yield little changed at 2.50%

- Euro up 0.2% to $1.0680

Top Overnight News

- The U.S. is drafting sanctions that threaten to cut some Chinese banks off from the global financial system, arming Washington’s top envoy with diplomatic leverage that officials hope will stop Beijing’s commercial support of Russia’s military production, according to people familiar with the matter. WSJ

- Chinese universities and research institutes recently obtained high-end Nvidia artificial intelligence chips through resellers, despite the U.S. widening a ban last year on the sale of such technology to China. RTRS

- China QE drumbeat grows louder as the country’s finance minister expresses support for the PBOC to resume trading gov’t bonds (although many doubt this would lead to Fed/ECB-style QE). WSJ

- AAPL's iPhone sales in China fell 19% during the March quarter, according to data from an independent research firm that marked the gadget’s worst performance there since Covid struck around 2020. BBG

- Japanese Finance Minister Shunichi Suzuki said last week's meeting with his U.S. and South Korean counterparts has laid the groundwork for Tokyo to act against excessive yen moves, issuing the strongest warning to date on the chance of intervention. RTRS

- ECB’s Luis De Guindos says a June cut is all but guaranteed, but what happens beyond that could depend on the actions of the Fed. WSJ

- Europe’s flash PMIs for April point to firmer growth (and inflation), with the slump in manufacturing showing signs of easing while services rose to 52.9 (up from 51.5 in Mar and above the Street’s 51.8 forecast), and overall price pressures intensified slightly. S&P

- Tesla headlines today’s earnings after seven straight days of declines. Margins, its robotaxi and the fate of its lower-cost EV will be the focus. The company is also being sued in California by a former employee who claims it failed to provide required notice for layoffs. BBG

- MSFT launches smaller AI models that provide “good enough” capabilities for many, but at a fraction of the cost (the models don’t need high-end Nvidia chips to function). NYT

Earnings

- Nucor Corp (NUE) Q1 2024 (USD): EPS 3.46 (exp. 3.66), Revenue 8.14bln (exp. 8.26bln). Expects earnings to decrease in Q2 vs Q1 due to decreased earnings in the steel mills segment. Average scrap and scrap substitute cost per gross ton USD 421 (exp. 399.58). Sales tons to outside customers 6.22mln (exp. 6.41mln).

- SAP (SAP GY) Q1 24 (EUR): Adj. EPS 0.81 (exp. 0.89), adj. revenue 8.04bln (exp. 8.03bln). Adj. cloud and software revenue EUR 6.96bln (exp. 6.93bln). Adj. cloud revenue EUR 3.93bln (exp. 3.94bln). Adj. cloud revenue in constant currencies +25% (exp. +24.5%). Adj. operating profit EUR 1.53bln (exp. 1.7bln). GUIDANCE: Cloud revenue view between 17.0-17.3bln (prev. 13.66bln in 2023). Cloud and software revenue view at EUR 29.0-29.5bln (prev. 26.92bln in 2023) Adj. Operating profit view EUR 7.6-7.9bln (prev. 6.51bln in 2023). Raises 2023 dividend 7% to EUR 2.20/shr vs 2022 dividend. (Newswires) SAP ADR (SAP) rose 2.1% in the US after-hours. Index Weightings: DAX 40 (10.9% - largest), Euro Stoxx 50 (5% - third largest), Stoxx 600 (1.3%).

- Renault (RNO FP) Q1 (EUR): Revenue 11.71bln (exp. 11.7bln). Sales +2.6% Y/Y. Strong order book in Europe, reflecting a very good start to the year. Co. is progressing well toward its target of cost reduction to lower EV costs by 40%. The EV market is a bit slower than had expected a few years ago. Talks with Geely and Aramco on the ICE powertrain JV are at an advanced stage.

- Novartis (NOVN SW) Q1 (USD): Revenue 11.8bln (exp. 11.5bln). Core EPS 1.80 (exp. 1.73); Raises FY24 Net Sales and Core Operating Income guidance. Strong sales momentum in Entresto (+36% cc), Cosentyx (+25% cc), Kesimpta (+66% cc), Kisqali (+54% cc), Pluvicto (+47% cc) and Leqvio (+139% cc). Free cash flow 2.0bln (-24%) - declined due to a prior-year one-timer and timing of payments. Novartis proposes Dr. Giovanni Caforio as Chair of the Board of Directors at AGM 2025. Index Weightings: SMI (15.9% - second largest), Stoxx 600 (2%). Net Sales are expected to grow high-single to low double-digit digits. Core operating income is expected to grow low double-digit to mid-teens.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with a mild positive bias after the tech-led rebound stateside. ASX 200 was led by strength in real estate and tech, while the latest flash PMIs from Australia were varied. Nikkei 225 traded indecisively and on both sides of 37,500 after briefly wiping out all of its opening gains. Hang Seng and Shanghai Comp. were mixed with outperformance in Hong Kong due to tech strength, while the mainland lagged amid the PBoC's continued tepid liquidity operations and with the US drafting sanctions that threaten to cut some Chinese banks off from the global financial system for aiding the Russian war effort.

Top Asian News

- US is reportedly drafting sanctions that threaten to cut some Chinese banks off from the global financial system as it hopes to stop Beijing's commercial support of Russia's military production, according to WSJ.

- BoJ Governor Ueda reiterated that monetary policy will be data dependent and will depend on the economy and inflation, while he said they don't have any pre-set idea on the timing and pace of future rate hikes and if trend inflation accelerates in line with their forecast, they will adjust the degree of monetary support through an interest rate hike. Ueda also stated if their price forecast changes, that will also be a reason to change policy but noted it is hard to say beforehand how long the BoJ should wait in gathering enough data to change policy and would like to leave some scope for adjustment by not pre-committing to a certain policy too much.

- Japanese Finance Minister Suzuki said the government is ready to respond appropriately to excessive FX moves and is closely watching FX moves with a high sense of urgency, while they won't rule out any option and will deal appropriately with excessive FX moves. Suzuki also said he closely communicated with the US and South Korea on forex in Washington and won't deny that last week's discussions in Washington have laid the groundwork for Japan to take appropriate FX action.

- Senior Japanese ruling party official said recent JPY falls are excessive and out of line with fundamentals; said Japanese authorities could intervene to prop up the JPY at any time

- Japan Business Lobby Keidanren Chair Tokura said he think Government will make appropriate decision on intervention, via Kyodo

European bourses, Stoxx600 (+0.6%) began the session on a strong footing, and has remained at elevated (albeit contained) levels throughout the European morning. There was little reaction to the EZ Flash PMI data. European sectors hold a positive tilt; Tech takes the top spot, benefiting from US tech gains in the prior session, and post-earning strength in SAP (+3.9%). Basic Resources is found at the foot of the pile, amid broader weakness in metals prices. US Equity Futures (ES +0.1%, NQ +0.2%, RTY U/C) are tentative ahead of a busy earnings slate and the key US PMI data.

Top European News

- ECB's de Guindos said a June rate cut looks like a set deal, if there are no surprises; end of inflation fight is in sight; largest remaining threat stems from services inflation. There's a clear slowdown in wage dynamics. Inclined to be very cautious what happens after June. Need to take into account what's happening in the US. What the Fed decides is crucial for the global economy. Beed to take impact of FX movements into account. Indicators point toward modest H2 Euro-area recovery.

- BoE's Haskel said UK food price inflation is "unusually high"; UK labour market is is "extremely tight", via Bloomberg. Inflation will stay high unless the job market weakens.

- Kantar UK Supermarket update (Apr): Grocery price inflation has fallen to 3.2% over the four weeks to 14 April, marking the fourteenth monthly drop in a row

FX

- DXY softer having briefly dipped under 106 amid gains in the EUR. Ultimately though, the index is in consolidation mode ahead of GDP and PCE metrics later this week and FOMC on May 1st. For now, the next downside target comes via last week's low at 105.74.

- EUR is boosted by PMI metrics which saw strong services and composite PMIs overshadow a soft outturn for the manufacturing sector. EUR/USD as high as 1.0695 with the 1.07 level not breached since 12th April; 1.0729 was the high that day.

- GBP: After a soft session yesterday which dragged the pair to a low of 1.23, Cable is on the front foot thanks to a strong showing for services PMI. 1.2388 is the high watermark thus far.

- JPY is steady vs. the USD but made another multi-decade high at 154.85. The closer the pair moves to 155, the louder the calls for intervention will get. For now, jawboning is providing minimal help for JPY.

- Antipodeans are varied the USD with slight outperformance in Aussie after AUD/NZD extended above 1.0900. AUD/USD saw little follow-through from PMI data overnight with the pair lingering around yesterday's best levels after printing a YTD low on Friday.

- PBoC set USD/CNY mid-point at 7.1059 vs exp. 7.2437 (prev. 7.1043).

Fixed Income

- USTs initially remained in overnight ranges, though succumbed to selling pressure, sparked by EZ-PMIs, which dragged EGBs lower. USTs matched yesterday's 107.31 high earlier in the session before pulling back to circa 107.25, and further downside could bring Monday's 107.17 low into view.

- Bunds looked as if they wanted to venture higher in early trade in an extension of yesterday's gains and with de Guindos labelling June as a done deal. However, EZ-wide and regional PMIs acted as a drag thereafter with a strong showing for the services sector, helping composite metrics to beat expectations. 131.47 was the peak before prices made a low at 130.98.

- Gilts started the session on the back foot thanks to an unwind of yesterday's Ramsden-induced gains and higher-than-expected public borrowing figures which saw the UK DMO revise higher its 2024/25 Gilt issuance remit. Gilts down as low as 96.90 with yesterday's trough at 96.71.

- UK DMO revises higher its 2024/25 Gilt issuance remit to GBP 277.7bln (prev. GBP 265.3bln)

- Italy sell EUR 2.5bln vs exp. EUR 2-2.5bln 3.20% 2026 BTP Short Term and EUR 2.5bln vs exp. EUR 2-2.5bln 1.50% 2029 & 1.80% 2036 BTPei:

- Germany sells EUR vs exp. EUR 5bln 2.90% 2026 Schatz: b/c 2.7x (prev. 2.31x) & avg. yield 2.91% (prev. 2.84%) and retention 18.6% (prev. 17.7%)

Commodities

- Upside across the crude complex underpinned by the Flash PMIs from Europe which (although manufacturing fell short of expectations) pointed to a services-led recovery; however, prices have pulled back from best levels in recent trade. Brent June meanwhile trades in a USD 86.97-97.95/bbl range.

- Softer trade across precious metals despite the softer Dollar as the geopolitical unwind from yesterday continues, with relatively broad-based losses seen across spot gold, silver and palladium; XAU fell under USD 2,300/oz to find current intraday support around USD 2,291/oz.

- Base metals are lower across the board with sizeable intraday losses despite the softer Dollar and risk-on tone across the rest of the market. There has been no obvious catalyst for this pullback but some desks cite Asian investors being cautious of the recent rally driven, in part, by speculative trading.

- Anglo American (AAL LN) Q1 Copper Production 198k tonnes (exp. 191.3k tonnes)

Geopolitics: Middle East

- Israeli occupation forces reportedly stormed the city of Jericho in the eastern West Bank, while it was also reported that Israeli gunboats targeted the seashores in the city of Khan Younis in the southern Gaza Strip. In relevant news, sirens sounded in the town of Metulla and the Kiryat Shmona area in northern Israel on suspicion of rocket fire, according to Al Jazeera.

- Hezbollah fired dozens of rockets into northern Israel on Monday which drew retaliatory strikes, while it said its attack was in response to recent Israeli strikes on towns and villages in southern Lebanon, according to Associated Press.

- Israeli raids were reported on the town of Yaroun in southern Lebanon, according to Al Jazeera.

- Hamas said it condemns the statements of US Secretary of State Blinken and his attempt to hold the group responsible for obstructing reaching an agreement, according to Sky News Arabia. Hamas said Blinken's statements contradict the fact that the movement has provided flexibility more than once to facilitate an agreement, while it added that the movement's demands are a permanent ceasefire, the withdrawal of the occupation and the return of the displaced to their homes in all areas of the Gaza Strip.

- US defence official said the Al-Asad airbase in Iraq came under attack from an Iranian proxy group today which is the second attack on a US base in two days, according to Fox.

Geopolitics: Other

- UK PM Sunak is to unveil an extra GBP 500mln of military funding to Ukraine and announce the largest supply of munitions to Kyiv on Tuesday as he travels to Poland and Germany, according to FT.

- North Korean state media reported that leader Kim guided the first nuclear counterstrike drills, while it stated that the drills are a clear warning sign to enemies.

US Event calendar

- 08:30: April Philadelphia Fed Non-Manufactu, prior -18.3

- 09:45: April S&P Global US Composite PMI, est. 52.0, prior 52.1

- 09:45: April S&P Global US Services PMI, est. 52.0, prior 51.7

- 09:45: April S&P Global US Manufacturing PM, est. 52.0, prior 51.9

- 10:00: Revisions: Retail Sales

- 10:00: April Richmond Fed Business Conditio, prior -8

- 10:00: April Richmond Fed Index, est. -8, prior -11

- 10:00: March New Home Sales MoM, est. 1.1%, prior -0.3%

- 10:00: March New Home Sales, est. 669,000, prior 662,000

DB's Jim Reid concludes the overnight wrap

It may not be saying a lot, but markets had their best performance in some time yesterday, as investors became a bit more optimistic about the near-term outlook. Equities recovered, and the S&P 500 (+0.87%) finally managed to advance after a run of 6 consecutive declines. Adding to the positive sentiment were growing hopes that a further escalation in the Middle East would be avoided, and Brent crude oil prices (-0.33%) fell back to their lowest level so far this month, at $87.00/bbl. So there were several pieces of better news for investors, but there’ll be no let-up on the calendar today, as we’ve got lots of earnings reports, including Tesla after the US close. While the Magnificent 7 were up +0.94% yesterday, Tesla was down -3.40%, extending its decline this year to -42.8% and having halved since last July. It's maybe a slight warning for the darlings of the current AI boom that things can change quickly if profits don't follow very high expectations as new technologies grow. Talking of which Nvidia bounced back from their -10.0% decline on Friday and rose +4.35% yesterday.

On top of earnings today, we’ll get an initial indication about how the global economy has performed in Q2, as the April flash PMIs are coming out for the major economies. These will be of particular interest for assessing the nascent recovery in the euro area economy. In March the composite PMI rose above the 50 level for the first time in 10 months. There will also be attention on the price components within the PMIs, especially in the US, where the composite output price index posted a 10-month high of its own last month.

We’ll have to see how those events pan out, but before all that, risk assets managed to post a strong recovery on both sides of the Atlantic. That made a change after three weeks of losses for global equities, with the major indices including the S&P 500 (+0.87%), the NASDAQ (+1.11%) and the STOXX 600 (+0.60%) all advancing. Information technology (+1.28%) and financials (+1.20%) outperformed within the S&P 500. Alongside that, the VIX index of volatility (-1.8pts) fell to 16.94pts, which is its lowest level since Iran launched their recent missile strike on Israel . And here in the UK, the FTSE 100 (+1.62%) even closed at an all-time high, aided by the weakness in sterling (-0.19%), which hit its weakest level against the US Dollar since November.

Henry did a piece yesterday (link here) looking at what happens next after the S&P 500 has seen 6 consecutive declines as we saw before last night's positive close. The subsequent 1-month and 6-month performances have mostly been positive in recent history. Moreover, if the S&P had posted a 7th consecutive decline yesterday, that would have taken us into unusual territory, as it’s something we haven’t seen since February 2020 as Covid-19 spread globally. Indeed, the examples of 7 consecutive losses for the S&P 500 (in the 21st century at least) have either been during a crisis (GFC, US debt ceiling crisis, Euro Crisis, Covid-19) or in anticipation of a pivotal event with significant uncertainty (2016 US election).

As discussed at the top, sentiment was bolstered by the lack of any further escalation in the Middle East. Indeed, yesterday saw Iran’s foreign ministry spokesman say that Israel had received the “necessary response at this stage”. The apparent easing in tensions helped oil prices fall back, and there was also a sharp move lower in gold (-2.59%), which had its biggest daily decline since June 2021. It's down another -0.90% this morning.

The more positive tone was evident across sovereign bonds too. They were supported by the drop in oil prices, which added to hopes that any spike in inflation would prove temporary, and the 1yr US inflation swap (-1.2bps) fell back for a 4th session to 2.71%. In turn, that meant investors grew a bit more hopeful about the prospect of rate cuts, and the amount of Fed rate cuts priced by the December meeting (+1.2bps) inched up to 40bps. Similarly at the ECB, the number of rate cuts priced by December’s meeting (+4.2bps) rose to 78bps.

With more rate cuts being priced in, that helped to push down yields, with those on 10yr bunds (-1.4bps), OATs (-2.7bps) and BTPs (-8.7bps) all moving lower. Admittedly, there was a decent intraday turnaround, as the 10yr bund yield had risen to 2.55% at one point, its highest level since November, before reversing course and ending the day lower at 2.48%. Meanwhile in the US, there was a decline in the 2yr Treasury yield (-1.5bps) to 4.97%, whilst the 10yr Treasury yield (-1.2bps) fell to 4.61%, as it also pared back its earlier losses, having still being above at 4.66% as Europe finished lunch.

In Asia the Hang Seng (+1.64%) is leading gains on a broker upgrade, with the Nikkei (+0.27%), the KOSPI (+0.20%) and the S&P/ASX 200 (+0.41%) seeing minor gains. Chinese stocks are the worst performers with the CSI (-0.56%) and the Shanghai Composite (-0.41%) both trading lower. US stock futures are broadly flat as I type.

Early morning data showed that key gauges of Japan’s manufacturing and service activity improved in April to its highest levels in nearly a year. The au Jibun Bank flash manufacturing PMI rose to 49.9 in April, as against a level of 48.2 in March. The services PMI advanced to 54.6 in April up from 54.1 in March indicating that the service sector continues to remain the primary driver of growth.

Elsewhere, Australia’s Judo Bank PMI data for April showed the manufacturing PMI rising to 49.9 from 47.3. Meanwhile, the service sector PMI came off slightly from 54.4 to 54.2, though still registering a decent growth environment. The composite PMI hit a 24-month high of 53.6 in April, an improvement from the previous month's 53.3.

To the day ahead now, and the main data highlight will be the April flash PMIs from Europe and the US. Elsewhere, we’ll get US new home sales for March, UK public finances for March, and the Richmond Fed’s manufacturing index for April. From central banks, we’ll hear from the ECB’s Panetta and Nagel, and the BoE’s Haskel and Pill. Finally, today’s earnings releases include Visa, Tesla, PepsiCo, General Electric, UPS and General Motors.

'Our Pesah with a place at the table for the innocent victims of Gaza'

The hostages in the hands of Hamas, but also the starving civilians in the Strip and the victims of settler violence, in the prayer published in Israel by Rabbi Arik Ascherman - of the 'Torah of Justice' movement - on the evening when Jews celebrate through the rite of the seder the liberation from Egypt."It is all too easy to become oppressed and oppressor at the same time.Stay with us, so that our fears do not become our masters".

The Feast of St George

St George has the distinction of being one of the earliest examples of a Saint whose biography was recognized to be historically doubtful. A document of the early 6th century known as the Gelasian Decree mentions him twice, once to say that his acts are not read by the Roman church, “lest even a slight occasion for mockery arise,” and again on a long list of “apocryphal” books. The term “Gregory DiPippohttp://www.blogger.com/profile/13295638279418781125noreply@blogger.com0

iPhone Sales In China Tumble 19% In Worst Quarter Since 2020

iPhone Sales In China Tumble 19% In Worst Quarter Since 2020

Tyler Durden

Tue, 04/23/2024 - 07:45

Apple shares are marginally lower in premarket trading in New York following a report that first-quarter iPhone sales in China had been the worst since early Covid. This comes ahead of an earnings report from the world's most valuable company next week and other souring reports from independent research firms tracking the slide in iPhone sales in China.

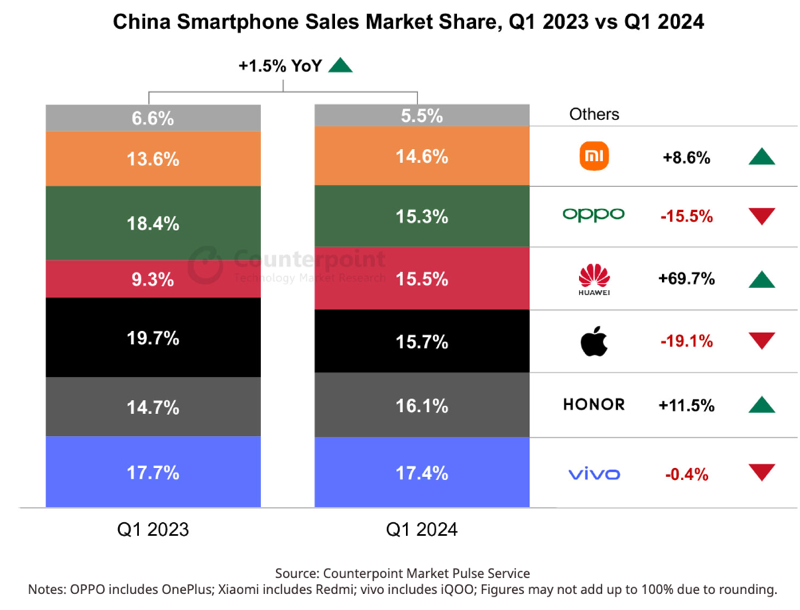

Counterpoint reports that overall, China, the world's largest handset market, recorded growth upwards of 1.5% year-over-year in the first quarter, marking the second consecutive quarter of positive year-over-year growth. Huawei is a rising star and the best performer of all major brands, growing 69.7% year-over-year, mainly because of the release of its 5G-capable Mate 60 series last fall. Meanwhile, Apple iPhone sales tumbled 19% in the quarter.

Here are the highlights of the report:

- China's smartphone sales grew 1.5% YoY and 4.6% QoQ in Q1 2024, marking the second consecutive quarter of positive YoY growth.

- Huawei stood out as the best performer among all OEMs during the quarter, enjoying 69.7% YoY growth; HONOR also saw double-digit growth.

- vivo took the top spot, followed by HONOR and Apple.

- Apple's sales dropped 19.1% YoY in Q1 as Huawei's comeback directly impacted the premium segment.

- The market is expected to see low single-digit YoY growth in 2024.

"Momentum seems to be building on a recovery as China's smartphone sales continued their growth trajectory and grew 4.6% QoQ in Q1 2024. The sales promotions during the Chinese New Year festivities were the biggest growth driver. The average weekly sales during the four weeks leading up to the Chinese New Year saw a robust growth of 20% when compared to a normal week, according to Counterpoint's China Smartphone Weekly Model Sales Tracker," Counterpoint's Associate Director Ethan Qi wrote in a statement.

Counterpoint's Senior Research Analyst Ivan Lam said on the iPhone recovery story, "We are seeing slow but steady improvement from week to week, so momentum could be shifting. For the second quarter, the possibility of new color options combined with aggressive sales initiatives could bring the brand back into positive territory; and of course, we are waiting to see what its AI features will offer come WWDC in June. That has the potential to move the needle significantly longer term."

Counterpoint's data was published one week after International Data Corporation reported that iPhone shipments plunged by 10% in the quarter.

Since early January, institutional desks, Barclays, Piper Sandler, and Jefferies have warned about a downturn in iPhone sales, mainly because of a slowdown in the world's largest handset market.

While Goldman removed Apple from its "Conviction List" and Evercore ISI dropped Apple from its "Tactical Outperform" list earlier this year, Bank of America analyst Wamsi Mohan named Apple the top pick for 2024, citing a "rich catalyst path with defensive cash flows."

Apple shares have been widely underperforming the S&P500 index on numerous reports this year on weaker iPhone demand in China.

Just 56% of the analysts tracked by Bloomberg have buy ratings on Apple, while the percentage of bulls for Microsoft, Nvidia, Alphabet, Amazon, and Meta Platforms is around 85%.

Besides waning iPhone sales in China, investors have been given the impression that the company lags in the artificial intelligence race. Just weeks ago, there were reports that the company nuked its car project. Plus, the $4,000 Apple Vision Pro goggles do not appear to be taking off as expected.

iPhone Sales In China Tumble 19% In Worst Quarter Since 2020

iPhone Sales In China Tumble 19% In Worst Quarter Since 2020

Tyler Durden

Tue, 04/23/2024 - 07:45

Apple shares are marginally lower in premarket trading in New York following a report that first-quarter iPhone sales in China had been the worst since early Covid. This comes ahead of an earnings report from the world's most valuable company next week and other souring reports from independent research firms tracking the slide in iPhone sales in China.

Counterpoint reports that overall, China, the world's largest handset market, recorded growth upwards of 1.5% year-over-year in the first quarter, marking the second consecutive quarter of positive year-over-year growth. Huawei is a rising star and the best performer of all major brands, growing 69.7% year-over-year, mainly because of the release of its 5G-capable Mate 60 series last fall. Meanwhile, Apple iPhone sales tumbled 19% in the quarter.

Here are the highlights of the report:

- China's smartphone sales grew 1.5% YoY and 4.6% QoQ in Q1 2024, marking the second consecutive quarter of positive YoY growth.

- Huawei stood out as the best performer among all OEMs during the quarter, enjoying 69.7% YoY growth; HONOR also saw double-digit growth.

- vivo took the top spot, followed by HONOR and Apple.

- Apple's sales dropped 19.1% YoY in Q1 as Huawei's comeback directly impacted the premium segment.

- The market is expected to see low single-digit YoY growth in 2024.

"Momentum seems to be building on a recovery as China's smartphone sales continued their growth trajectory and grew 4.6% QoQ in Q1 2024. The sales promotions during the Chinese New Year festivities were the biggest growth driver. The average weekly sales during the four weeks leading up to the Chinese New Year saw a robust growth of 20% when compared to a normal week, according to Counterpoint's China Smartphone Weekly Model Sales Tracker," Counterpoint's Associate Director Ethan Qi wrote in a statement.

Counterpoint's Senior Research Analyst Ivan Lam said on the iPhone recovery story, "We are seeing slow but steady improvement from week to week, so momentum could be shifting. For the second quarter, the possibility of new color options combined with aggressive sales initiatives could bring the brand back into positive territory; and of course, we are waiting to see what its AI features will offer come WWDC in June. That has the potential to move the needle significantly longer term."

Counterpoint's data was published one week after International Data Corporation reported that iPhone shipments plunged by 10% in the quarter.

Since early January, institutional desks, Barclays, Piper Sandler, and Jefferies have warned about a downturn in iPhone sales, mainly because of a slowdown in the world's largest handset market.

While Goldman removed Apple from its "Conviction List" and Evercore ISI dropped Apple from its "Tactical Outperform" list earlier this year, Bank of America analyst Wamsi Mohan named Apple the top pick for 2024, citing a "rich catalyst path with defensive cash flows."

Apple shares have been widely underperforming the S&P500 index on numerous reports this year on weaker iPhone demand in China.

Just 56% of the analysts tracked by Bloomberg have buy ratings on Apple, while the percentage of bulls for Microsoft, Nvidia, Alphabet, Amazon, and Meta Platforms is around 85%.

Besides waning iPhone sales in China, investors have been given the impression that the company lags in the artificial intelligence race. Just weeks ago, there were reports that the company nuked its car project. Plus, the $4,000 Apple Vision Pro goggles do not appear to be taking off as expected.

Which Major City Will Completely Collapse First – Los Angeles, Chicago, Or New York City?

Which Major City Will Completely Collapse First – Los Angeles, Chicago, Or New York City?

Tyler Durden

Tue, 04/23/2024 - 07:20

Authored by Michael Snyder via The End of The American Dream blog,

In 2024, virtually all major U.S. cities have certain things in common. First of all, if you visit the downtown area of one of our major cities you are likely to see garbage, human excrement and graffiti all over the place. As you will see below, some of our core urban areas literally look like they belong in a third world country. Most of our politicians don’t seem too concerned about doing anything to clean up all the filth, and so it shouldn’t be a surprise that rat populations are absolutely exploding all over the country. In some of our largest cities, the total rat population is numbered in the millions. Meanwhile, rampant theft, out of control violence, endless migration, predatory gangs and the worst drug crisis in the entire history of our nation have combined to create a “perfect storm” of social decay that is unlike anything that any of us have ever seen before. Millions of law-abiding citizens and countless businesses have been fleeing America’s largest cities, and property values in our core urban areas have been absolutely crashing. We really are in the early stages of a full-blown societal “collapse”, and things just keep getting worse with each passing day.

In this article, I want to focus on the three largest metropolitan areas in the United States: New York, Los Angeles and Chicago.

John Williams recently took his camera with him as he walked through downtown Los Angeles, and he described what he witnessed as “hell”…

Decades of failed policies have transformed one of the greatest cities in the entire country into one of the worst.

At this point, theft has become so rampant that even the ultra-progressive politicians in California have come to the conclusion that something must be done.

So several bills that would “crack down on shoplifting” have been introduced in the state legislature…

Shoplifters beware.

The California Assembly has introduced a comprehensive package of seven bills aimed at addressing the rising concerns over retail theft across the state.

One of the key initiatives is Assembly Bill 2943, jointly authored by Assemblymember Rick Chavez Zbur (D) and Speaker Robert Rivas (D). The bill targets serial retail thieves by introducing a new crime with penalties of up to three years behind bars for possession of stolen property with intent to resell. It also allows for the aggregation of similar thefts from different victims to charge grand theft, under specific criteria.

Hopefully something will get done, because right now a criminal in the state of California can “literally walk into a retail store every single day of the year and steaI $949 worth of merchandise” and never spend a single minute in jail.

"You can literally walk into a retail store every single day of the year and steaI $949 worth of merchandise"

"And you will NEVER do a minute in jail"

"Under California law, assauIt on a peace officer with anything other than a fully automatic weapon is not a vioIent crime"… pic.twitter.com/jX0l4OK6pA

Los Angeles has become a paradise for shoplifters, but many would argue that things are even worse in the Big Apple.

As I discussed a few days ago, New York City has “a $4.4 billion shoplifting economy”.

And approximately 90,000 packages are stolen in New York City every single day.

This is just one of the reasons why we have seen a mass exodus.

Countless New Yorkers have already left for greener pastures, and lots more are thinking of leaving…

About 7 million New Yorkers plan to leave the state, a new survey revealed this month.

In a new Marist poll, 37 percent of New Yorkers—roughly 7 million people—said they plan to move away. The number was slightly more concentrated among Republicans, as 46 percent said they plan to leave the state compared to just 29 percent of Democrats.

Unsurprisingly, many of those that are fleeing are heading to Florida…

For many, Florida remains one of the top places to move, but Southern states in general have been recording the biggest influx in transplants.

According to Realtor.com, Philadelphia, Miami, Atlanta, Tampa and Orlando remain some of the top locations for New Yorkers to start again.

I wouldn’t want to live in the Big Apple either.

The rat problem alone would be enough for me to move.

It just continues to escalate, and politicians are now proposing to use “rat contraceptives” to deal with “the millions of rats lurking in subway stations and empty lots”…

In New York City, the idea to distribute rat contraceptives got fresh attention in city government Thursday following the death of an escaped zoo owl, known as Flaco, who was found dead with rat poison in his system.

City Council Member Shaun Abreu proposed a city ordinance Thursday that would establish a pilot program for controlling the millions of rats lurking in subway stations and empty lots by using birth control instead of lethal chemicals. Abreu, chair of the Committee on Sanitation and Solid Waste Management, said the contraceptives also are more ethical and humane than other methods.

Unfortunately, New York City doesn’t have the worst rat problem in America.

That title actually belongs to the city of Chicago…

Chicago has once again been declared the rattiest city in the U.S. according to Orkin’s annual ranking.

Los Angeles surpassed New York on this year’s list now holding the #2 spot and bringing the Big Apple down to #3, Orkin shared.

Other notable shifts included Houston, which moved 10 spots up to #20, and Charlotte, North Carolina that rose 16 spots to #21.

Somehow, the rat problem in Chicago has gone to an entirely new level in 2024.

In fact, one local resident says that it is now the worst that she has ever seen in her entire lifetime…

A resurgence of rats has gotten out of control in Chicago’s Portage Park neighborhood, multiple residents explained Friday as they called for city leaders to take further action.

Diana Gazda, a resident of the Far Northwest Side community for seven decades, said she has never seen an infestation like it.

“We never had a rat problem like this,” she stated. “I’ve been here 71 years in my house.”

In addition to being world famous for rats, the Windy City is also world famous for violence.

In Chicago, you can be gunned down at any time of the day or night.

Nobody is safe, and that is especially true for police officers…

A Chicago police officer was shot to death early Sunday in Gage Park on the Southwest Side in what sources are saying was an apparent carjacking.

Officers responded to a ShotSpotter alert about 2:55 a.m. and found Officer Luis Huesca with multiple gunshot wounds in the 3100 block of West 56th Street, a police spokesperson said in a statement.

Huesca, 30, was driving home from work, according to city officials. Huesca, who was still wearing his uniform, was taken to University of Chicago Medical Center, where he was pronounced dead.

So which of these cities will completely collapse first?

I think that is a very good question.

They are all headed downhill very rapidly, and they are all being run by radical leftists.

Of course the exact same things could be said about dozens of other U.S. cities.

For years, I have been warning my readers about the “cultural transformation” that has been taking place in America.

How we raise our kids really matters.

We have been failing them for decades, and now the consequences can be very clearly seen in the streets of our major cities.

A horrific societal collapse is upon us, and yet this nation continues to refuse to change direction.

* * *

Michael’s new book entitled “Chaos” is available in paperback and for the Kindle on Amazon.com, and you can check out his new Substack newsletter right here.

Post Earth Day: Six Things To Do And Share

Earth Day is now beyond us. I am sure you will be exhausted from hearing your leftist neighbour go on and on about the celebrations. This little guide is a help on useful things to do (and not to do) the day after. So let us start without further ado: Do not kill and compost […]

Conservatives Are Wrong on Economics. Here's How to Fix the Problem.

While conservatives and followers of Austrian economics often have much in common, many conservatives are against free trade and free exchange. Austrians need to carefully explain why those beliefs are harmful.

Adherents of Austrian Economics Should Try to Influence Conservatives

While conservatives and followers of Austrian economics often have much in common, many conservatives are against free trade and free exchange. Austrians need to carefully explain why those beliefs are harmful.

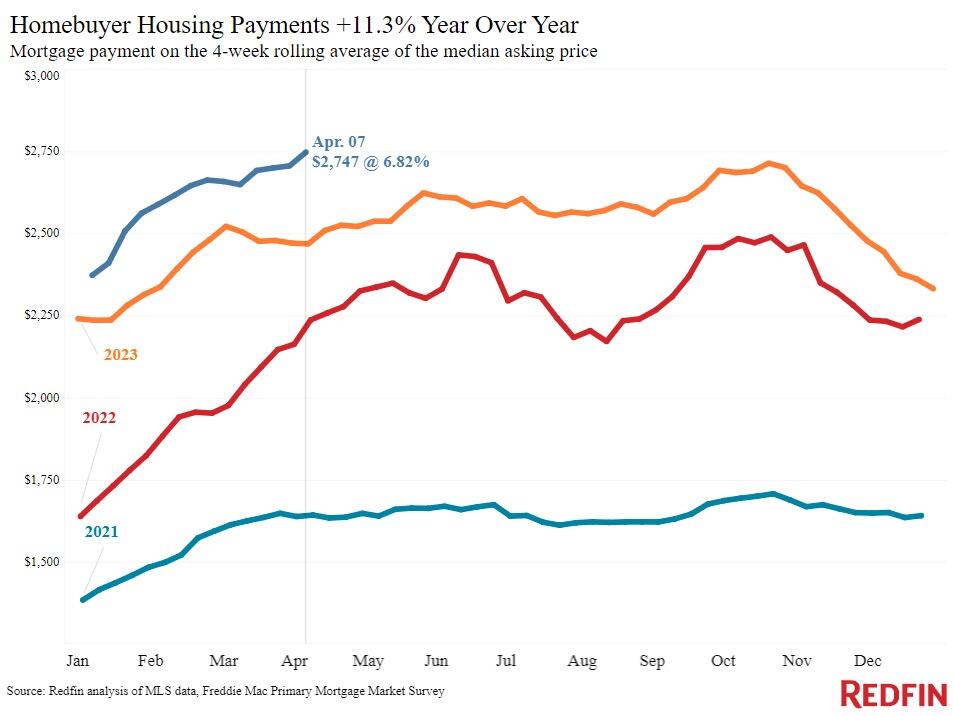

Homebuyer Payment Hits Record High As Mortgage Rates Climb Back Above 7% For The First Time In 2024

Homebuyer Payment Hits Record High As Mortgage Rates Climb Back Above 7% For The First Time In 2024

Tyler Durden

Tue, 04/23/2024 - 06:55

Mortgage rates in the United States climbed to the highest level since November 2023 last week, as higher-than-expected inflation readings have dashed hopes of the Fed starting to cut rates soon.

As Statista's Felix Richter reports, according to Freddie Mac, the average rate for a 30-year fixed mortgage increased to 7.10 percent in the week ended April 18, making it difficult for many would-be homebuyers to afford a house.

You will find more infographics at Statista

Along with the Fed's aggressive rate hikes, mortgage rates have climbed by almost 4 percentage points since the beginning of 2022, threatening to push more and more potential buyers out of the market, especially as high rents and other costs of living make it increasingly difficult to save for a significant down payment.

Making things even more difficult, high mortgage rates don't just affect the demand side of the market.

Supply is also constrained as prospective sellers stay put to avoid taking out a new mortgage at a much higher rate than their current one.

Source: Bloomberg

This in turn has kept home prices elevated, or at least kept them from fully reflecting the significantly higher mortgage rates compared to two years ago.

"When rates go up, people hunker down and don’t spend," mortgage broker Rocke Andrews told Realtor.com.

"They’ve been told for so long that rates are coming down, so they just postpone."

And they made need a little more patience.

Last week, Fed chair Jerome Powell said that policymakers were in no rush to cut rates, making it unlikely for mortgage rates, which tend to follow the same trajectory as the Fed's policy rate, to come down meaningfully anytime soon.

In fact, according to brokerage Redfin, U.S. homebuyers face the prospect of having to pay a “record” amount in monthly mortgage payments to buy a house amid extremely high prices and elevated mortgage rates.

“The median U.S. home-sale price increased 5 percent from a year earlier during the four weeks ending April 14, bringing it to $380,250 - just $3,095 shy of June 2022’s all-time high,” said an April 18 press release from Redfin.

“The average daily mortgage rate this week surpassed 7.4 percent, the highest level since last November, after a hotter-than-expected inflation report and the Fed’s confirmation that interest-rate cuts will be delayed.”

The 12-month inflation had jumped 0.3 percent, to 3.5 percent in March.

“The combination of high mortgage rates and prices have brought homebuyers’ median monthly housing payment to a record $2,775, up 11 percent year over year.”

According to a recent analysis by Bankrate, Americans now need an annual income of $110,871 to afford a median-priced home of $402,343. This is an almost 50 percent increase over a period of just four years.

A six-figure annual income is now mandatory to afford a median-priced home in 22 states and the District of Columbia.

Four years ago, only six states and the District of Columbia had such a high requirement.

Homebuyer Payment Hits Record High As Mortgage Rates Climb Back Above 7% For The First Time In 2024

Homebuyer Payment Hits Record High As Mortgage Rates Climb Back Above 7% For The First Time In 2024

Tyler Durden

Tue, 04/23/2024 - 06:55

Mortgage rates in the United States climbed to the highest level since November 2023 last week, as higher-than-expected inflation readings have dashed hopes of the Fed starting to cut rates soon.

As Statista's Felix Richter reports, according to Freddie Mac, the average rate for a 30-year fixed mortgage increased to 7.10 percent in the week ended April 18, making it difficult for many would-be homebuyers to afford a house.

You will find more infographics at Statista

Along with the Fed's aggressive rate hikes, mortgage rates have climbed by almost 4 percentage points since the beginning of 2022, threatening to push more and more potential buyers out of the market, especially as high rents and other costs of living make it increasingly difficult to save for a significant down payment.

Making things even more difficult, high mortgage rates don't just affect the demand side of the market.

Supply is also constrained as prospective sellers stay put to avoid taking out a new mortgage at a much higher rate than their current one.

Source: Bloomberg

This in turn has kept home prices elevated, or at least kept them from fully reflecting the significantly higher mortgage rates compared to two years ago.

"When rates go up, people hunker down and don’t spend," mortgage broker Rocke Andrews told Realtor.com.

"They’ve been told for so long that rates are coming down, so they just postpone."

And they made need a little more patience.

Last week, Fed chair Jerome Powell said that policymakers were in no rush to cut rates, making it unlikely for mortgage rates, which tend to follow the same trajectory as the Fed's policy rate, to come down meaningfully anytime soon.

In fact, according to brokerage Redfin, U.S. homebuyers face the prospect of having to pay a “record” amount in monthly mortgage payments to buy a house amid extremely high prices and elevated mortgage rates.

“The median U.S. home-sale price increased 5 percent from a year earlier during the four weeks ending April 14, bringing it to $380,250 - just $3,095 shy of June 2022’s all-time high,” said an April 18 press release from Redfin.

“The average daily mortgage rate this week surpassed 7.4 percent, the highest level since last November, after a hotter-than-expected inflation report and the Fed’s confirmation that interest-rate cuts will be delayed.”

The 12-month inflation had jumped 0.3 percent, to 3.5 percent in March.

“The combination of high mortgage rates and prices have brought homebuyers’ median monthly housing payment to a record $2,775, up 11 percent year over year.”

According to a recent analysis by Bankrate, Americans now need an annual income of $110,871 to afford a median-priced home of $402,343. This is an almost 50 percent increase over a period of just four years.

A six-figure annual income is now mandatory to afford a median-priced home in 22 states and the District of Columbia.

Four years ago, only six states and the District of Columbia had such a high requirement.

If We Want Something As Good But More Reliable, It'll Cost Much More Money

If We Want Something As Good But More Reliable, It'll Cost Much More Money

Tyler Durden

Tue, 04/23/2024 - 06:30

By Eric Peters, CIO of One River Asset Management

Utopia?

“We added solar and wind like it was going out of style,” said the CIO of the well-regarded US fund. “We have ample land, wind in the middle of the country.” Federal subsidies make electricity almost free. “But it’s a Catch-22 where we’re adding capacity, but reliability is declining.” In Feb 2021 Texas suffered a catastrophic electrical grid failure. Renewables went offline when they were most needed. Gas turbines froze too. 4mm homes went without power. Hundreds died. “Now policymakers across the spectrum seem to be acknowledging the need for both renewables and hydrocarbons.”

“Back in 2018 there was a utopian vision,” continued the same CIO.

“The economics were there, the physics allowed it, all we needed was political will.”

Net zero could be achieved painlessly, while boosting growth.

“But we’ve learned wind turbines frequently break, and don’t recycle well. They kill lots of large birds. Electric cars take a year to repair when you crash them.”

The residual values are lousy when you sell them.

“So now we’re asking better questions and considering the true costs and benefits. The tradeoffs. We’re growing up.”

“Asking good questions is always better for society,” said the CIO.

“There is pushback on the dogmatic view that the future of the world hangs in the balance, and those taking the most extreme positions on the matter have been undermined by an unwillingness to consider nuclear at any price,” he said.

“European banks will not fund hydrocarbons, it’s almost a religious belief at this point. But we will fund them because they’re a vital part of tomorrow’s energy mix and we can earn double-digit returns doing so.”

“If we want to build BMWs using windmills, it’s going to cost a lot to do it, and historically that’s the kind of thing the government must subsidize,” said the CIO. “It’s a societal good, like building parks in cities.” It is not a purely economic decision from the private sector’s standpoint. “A chip factory is being built in Taylor Texas with $6bln in Federal subsidies. Samsung is investing more than $30bln. That’s a societal good too. Because for security reasons, we may all sleep better at night buying some of our chips from Taylor instead of Taipei. But they may well cost more.”

“Ultimately, these decisions are about whether we’re willing to settle for something less good in exchange for something more reliable,” continued the CIO.

“If we want something as good and more reliable, it’ll cost more money. A way to think about these increased costs is a form of insurance.”

Insuring our children’s futures against the risk of cataclysmic climate change. Insuring our access to advanced chips against military conflict over Taiwan.

“Thinking through long-term risks is always a healthy exercise, and insuring against them sometimes requires government funding.”

“Europe made some naïve choices when they went through this exercise,” he said. “Germany shut all its nuclear power plants.” Which required it to increase its dependency on cheap Russian gas, strengthening Putin’s hand, which he then played in Ukraine. “They were going the opposite way; they were essentially selling insurance instead of buying it.”

This of course, is why it is vital that societies ask good questions and consider the true costs and benefits of big decisions.

“And the consequence is that Europe is deindustrializing. It’s stunning.”

Record Catholic deputies in Seoul: 80 out of 300 in the new parliament

âThe largest number in the Democratic Party that emerged victorious from the 10 April vote.Catholics make up 11.3% of the country's population.The bishops had urged the laity not to neglect their responsibility for the common good.This theme also emerged in the commemoration of the 10th anniversary of the Sewol ferry massacre, which remains without a single culprit.

Are Americans Moving From Blue To Red States?

Are Americans Moving From Blue To Red States?

Tyler Durden

Tue, 04/23/2024 - 05:45

In the last couple of years, large U.S. states where a majority of voters support Democrats – so-called blue states – have been losing population, while some large red states, where there is majority support for Republicans, have gained residents.

An analysis of Census Bureau data shows that there are in fact some big movements of people from states currently defined as blue to those currently defined as red.

However, as Statista's Katharina Buchholz reports, the situation is more accurately described as more people exiting certain blue states – for example New York and California – and heading to other states in general, may they be red or blue.

In 2005 and 2022 alike, those moving from blue states have been almost equally splitting up between blue and red states.

Only their total number has been increasing, from 3.7 million or 2.4 percent of blue states’ population to 4.6 million or 2.7 percent of population in the given years, boosting migration to both red and other blue states.

You will find more infographics at Statista

At the same time, migration from red states has not changed as much – increasing only from 3.3 million in 2005 to 3.6 million in 2022. As in blue states, the split of destinations has stayed almost exactly constant over the years, with red staters choosing other red states 61-62 percent of the time and blue states only 38-39 percent of times.

This means that compared with the mid-2000s, blue states now transfer more than 500,000 more residents towards red states annually (and about as many within blue states). Inflows from red states to blue states have only increased by a little more than 100,000 per year in this time frame.

So while it might be true that a high cost of living and a (perceived) low quality of life is driving people away from certain blue states, this is not driving them towards red states more than in the past, relatively speaking.

Migration from abroad is also boosting U.S. populations.

In 2022, around 1 million more people immigrated into the United States than left the country. International migrants had traditionally chosen larger cities in both red and blue states, but this type of migration has diversified over the past decades.

While this leaves both states like Texas and New York with fewer (official) international arrivals, it has had a more detrimental effect in blue states that already suffer from domestic out-migration.

For the sake of this analysis, states are assigned the designation blue or red based on their vote in the last three presidential elections. For comparability, the definition of red states and blue states was not changed for 2005. Colorado, Virginia and Nevada – where domestic immigration has boomed recently – would technically be defined as red states, not blue, in 2005. However, patterns of migrations for these states are consistent between 2005 and 2022 instead of changing upon their reorientation, also supporting the hypothesis that U.S. migration flows are relatively constant and dependent on factors like location and proximity rather than politics.

Meet the Reverend Thomas Blackburn, of Ripon (1)

In March, 1570, there was an unusual spectacle in the mighty Church of S Peter at Ripon (one of great S Wilfrid's great foundations). The sight to be seen was of a once-senior priest of that Church in church on a Sunday morning, wearing a white sheet. This fate was known as Doing Penance; it was a humiliation commonly reserved for adulterers and fornicators.Blackburn had been found Fr John Hunwickehttp://www.blogger.com/profile/17766211573399409633noreply@blogger.com0

World Cup of Great Catholic Leaders - nominations, please!

Well, the

World Cup of Misused Churches

has been a bit of an anti-climax, as the polling

was probably the slowest of any of these World Cups.

Maybe we can do better this time.

Various people (some of them extremely

implausible) have been described as Catholic Leaders, or similar. So we will vote to see

who best deserves that description.

The rules:

1. Candidates must be living Catholic priests/bishops/etc.

So hard luck, Austen Ivereigh, Taylor Marshall, Joe Biden, ...

2. We will, as usual, do this by Twitter polls.

3. Marko Rupnik is disqualified.

4. The umpire's decision (mine) is final.

So far I have the following nominations (ranging from the

sublime to the ridiculous, but you will be able to decide which is which):

Athanasius Schneider

Carlo Maria Viganò

Charles Chaput

Dwight Longenecker

Gerhard Ludwig Müller

James Martin

John Zuhlsdorf

Joseph Strickland

Joseph Zen

Mario Grech

Pope Francis

Raymond Burke

Robert Barron

Robert Sarah

Thomas Reese

Timothy Dolan

Víctor Manuel Fernández

Wilfrid Napier

Wilton Gregory

You are encouraged to nominate further candidates, either by replying to this

post or by replying to the advert on Twitter. If I have never

heard of your nominee, then he probably isn't eligible,

however #saved he may be.

Also disqualified!

This one is SERIOUS, even though you may agree that some of the candidates

are complete no-hopers.

Also disqualified!

This one is SERIOUS, even though you may agree that some of the candidates

are complete no-hopers.

Pages

Telegram Channels

Today's Mass

Traditional Liturgical Calendar

Tags

abortion

anti-Catholicism

anti-Christianity

anti-Russian propaganda

apostasy

Bergoglio anti-Catholicism

Bergoglio effect

Bergoglio heresy

Bergoglio homosexualism

Bergoglio idiocy

Bergoglioism

Bergoglio pontificate failure

Bp. Athanasius Schneider

CallMeJorge

Cardinal Müller

Cardinal Robert Sarah

Cdl. Raymond Burke

China

Church in Germany

Church revival

Covid19 coronavirus totalitarianism

culture of death

diabolical disorientation

DNC

Donald Trump

E.U.

EponymousFlower

euthanasia

feminism

Fr. Allan J. McDonald

Fr. John Hunwicke

Fr. John Zuhlsdorf

Fr. Peter Carota

Fr. Ray Blake

France

Germany

GlobalResearch

Gloria.tv

Gregory DiPippo

Holy Communion for lechers

homosexualism

homosexuality

intra-Church persecution

ISIS

Islam

Islamisation

Laura Wood

leftism

LifeNews

LifeSiteNews

Louie Verrecchio

Maike Hickson

marriage

Matthew Archbold

Michael Matt

modernism

Mundabor

Novus Motus Liturgicus

Novus Ordo

Novus Ordo apostasy

Novus Ordo filth

Novusordoism

Novus Ordo Missae

NovusOrdoWatch

OnePeterFive

papal heresy

papal piracy

papal scandal

persecution

Peter Hitchens

Peter Kwasniewski

political correctness

Pope Benedict XVI

Roberto de Mattei

Ron Paul Institute

Rorate Caeli

Russia

SSPX

Steve Skojec

StrategicCulture.org

Sweden

Syrian war

Tantumblogo

The Remnant

totalitarianism

traditionalism

transgenderism

Tridentine Mass

U.K. decline

U.S. circus

U.S. decline

U.S. militarism

U.S. roguery

Ukraine

Vatican II

Vladimir Putin

VoxCantoris

Western civilisation downfall

Western decadence

Western intervention