The Eucharist is "the source and summit of the Christian life."

Distinction Matter - Subscribed Feeds

-

Site: Mundabor's blogSome interesting things are happening, which I think deserve a little reflection from a Catholic point of view. Three companies are either bankrupt (Hooter’s), on their way to bankruptcy (Weight Watchers, now WW), or severely beaten (Harley Davidson). Let’s see what their troubles tell us. Hooter’s. This seems to me a typical example of “get […]

-

Site: Mises InstituteMark Thornton exposes the real threat to our economy—and it’s not what you’ve been told.

-

Site: Real Jew News

Stairway To Heaven

April 11 2025___________________________________

More Vids!

+BN Vids Archive! HERE!

___________________________________

Support The Brother Nathanael Foundation!

Br Nathanael Fnd Is Tax Exempt/EIN 27-2983459

Or Send Your Contribution To:

The Brother Nathanael Foundation, POB 547, Priest River, ID 83856

E-mail: brothernathanaelfoundation([at])yahoo[dot]com

Scroll Down For Comments

-

Site: Rorate CaeliThe following post, by Dan Sevigny, first appeared at OnePeterFive and is reprinted here with permission. I will add that I know Dan personally, have visited the ranch, and have seen the incredible work they are doing. This apostolate fully deserves whatever support people can send their way! - PAKIn a world where traditional Catholic values are increasingly challenged, Sanctus Ranch stands as a Peter Kwasniewskihttp://www.blogger.com/profile/05136784193150446335noreply@blogger.com

-

Site: The Remnant Newspaper - Remnant ArticlesThis is Part 3 in an essential series if one seeks to better understand Israel's Zionist-backed war in the Middle East. Part 1 is here. Part 2 is here.

-

Site: Euthanasia Prevention CoalitionThe Care NOT Killing Alliance in the UK sent an update urging supporters to contact elected representatives in (London UK) and in Scotland, to oppose the assisted suicide bills. The message stated:

Dear Friends:

We learned this week that the Leadbeater Bill’s Report Stage will now commence on Friday 16 May, a delay of several weeks, while the Scottish Daily Express reported today that ‘a vote on the private member's Bill from Liberal Democrat MSP Liam McArthur is expected in the first two weeks of next month, and it must take place before May 23.’

In these next few weeks, we all have an opportunity to influence politicians as they weigh up the risks posed by these bills, and while it’s easy to be cynical, a great many are giving this serious and sincere thought. As SNP MSP Michelle Thomson said today:

‘I started looking at it and instinctively, I was in favour of it. I saw my mother die of cancer and all that she went through… But I’m not making decisions just for my mother, I’m not making it just for me, I’m making decisions for huge sectors of society and that’s why I hope that everybody will look into the matter really carefully and consider all these constituent groups too.’Care NOT Killing urges their supporters to contact elected representatives. The letter continues:

It was reassuring to hear that Health Secretary Wes Streeting will once again vote against the Leadbeater Bill. Remember, he voted FOR a similar bill in 2015 — parliamentarians can and do change position in light of the evidence.

If the law did change, how would legalised assisted suicide sit alongside existing healthcare concerns? It was reported this week that:

‘Hospitals will receive an “incentive payment” for each patient they remove [from their waiting lists], and a payment cap of 5% of a trust’s waiting list is being scrapped, according to documents seen by the Guardian. It means there is no limit to the payments NHS trusts could receive for taking patients off their lists… The strategy is likely to raise concerns among patient charities that some people may be wrongly removed.’ The letter continues with Professor Kevin Yuill of Humanists Against Assisted Suicide and Euthanasia commented:

‘Nothing bad could possibly come of [the Leadbeater Bill’s] provisions that doctors can bring the topic [of assisted suicide] up and that it will be outsourced to for-profit companies. Everything is fine!’ The letter then looks at what is happening in Canada:Ultimately, what could healthcare look like a few years after legalisation, when the law has already been extended and people have become desensitised? Dr Ramona Coelho, a member of Ontario (Canada)’s MAiD Death Review Committee (MDRC), pointed this week to this story:

‘Mr. C, diagnosed with metastatic cancer, [who had] initially expressed interest in MAiD but then experienced cognitive decline and became delirious. He was sedated for pain management. Despite the treating team confirming that capacity was no longer present, a MAiD practitioner arrived and withheld sedation, attempting to rouse him. It was documented that the patient mouthed “yes” and nodded and blinked in response to questions. Based on this interaction, the MAiD provider deemed the patient to have capacity. The MAiD practitioner then facilitated a virtual second assessment, and MAiD was administered.’

‘If we truly value dignity, we must invest in comprehensive care to prevent patients from being administered speedy death in their most vulnerable moment, turning their worst day into potentially their last.’They conclude their letter with a statement from former Peterborough MP Lord Jackson has written this week:

‘Vulnerable people across the UK require MPs to survey the horizon, assess the risks and legislate for the weakest. The Bill process so far has proven us to be inept in this. We must do better. Kim Leadbeater must do better. Objectively, this Bill deserves to fail.’More articles on the topic:

- British MP who supported assisted suicide is opposing the assisted suicide bill (Link).

- The UK assisted dying bill gets more dangerous by the day (Link).

- UK assisted suicide bill is losing support and can be defeated (Link).

- Follow the money. Members of Scottish parliament accept money from? (Link).

- Scotland's assisted suicide bill is dangerous (Link).

-

Site: Novus Motus LiturgicusIn yesterday’s article, I described the Roman station church of Passion Thursday as a place of exile for Eastern iconodule monks whom the persecution of the iconoclast Byzantine emperors had driven into Italy. This basilica is dedicated to St Apollinaris, the first bishop of Ravenna, who is traditionally said to have been a disciple of St Peter, sent there by him to evangelize the northern Gregory DiPippohttp://www.blogger.com/profile/13295638279418781125noreply@blogger.com0

-

Site: Real Investment Advice

Inside This Week's Bull Bear Report

- Basis Trade Sends Yields Soaring

- How We Are Trading It

- Research Report - Stock Market As Recession Indicator

- Youtube - Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Tariff Reprieve Sends Stocks Surging

Last week, we noted that the market was not expecting retaliation from China.

"Rather than coming to the table to negotiate, China responded with a reciprocal 34% tariff on the U.S. plus export controls on rare earth metals needed for technological production. China is playing "hardball" negotiating tactics with Trump. This was a smart move from a negotiating standpoint by China, allowing President Xi to open tariff discussions from a point of strength. However, without some resolution to the extraordinary tariffs, the market will remain in turmoil for quite some time."

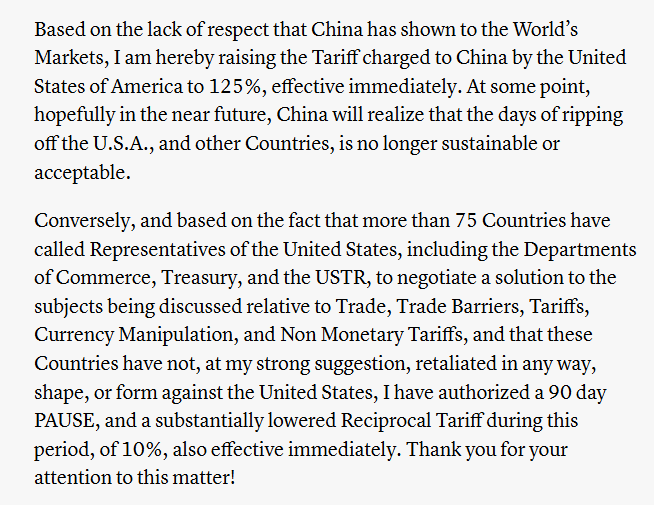

That battle persisted this week as Trump raised tariffs on China to 104%, and China then retaliated with a further tariff increase of 84%. However, as we said last week, any good news would cause the market to rally sharply. On Wednesday, President Trump announced a 90-pause on the full effect of new tariffs. Interestingly, the same headline sent stocks surging on Monday but was quickly deemed "fake news" by the White House. I suspect that Monday was a "leak" by the White House to test the market response, and President Trump kept that announcement handly to stave off a further decline in the markets. Whatever the reason, the markets needed the break. Here is Trump's full statement:

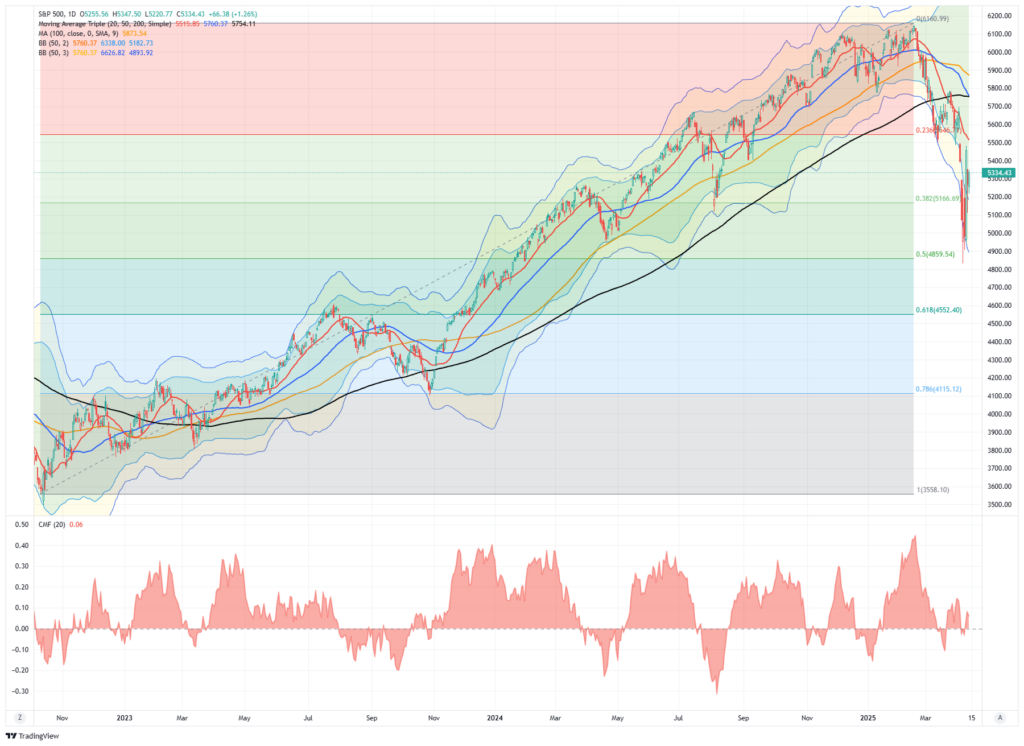

From a technical view, the market completed an expected retracement from the October 2022 lows. Last week, we laid out the potential correction levels.

- The recent lows are around 5500. (That level was violated)

- Immediately below that is the 38.2% retracement level at 5134 (Is being challenged)

- Lastly, the 50% retracement level at 4816 should hold, barring the onset of a fiscal event or recession.

Notably, we stated that:

"The market should be able to find some support at this level and muster a short-term rally next week. However, there is a downside risk to 4816, which would be a 50% retracement of the bull market rally. Any positive announcements over the weekend could spark a relatively robust reversal rally, given the more than three-standard deviation gap between where the market closed and the 50-DMA."

That 38.2% retracement level, using the bull market from October 2022 lows, was broken early Monday morning as stocks plunged lower amid rising tariff concerns and a blowup in the bond market. However, the market finally tested the 50% retracement level on Wednesday morning. Given the deep oversold condition, President Trump's announcement to pause tariffs led to the 3rd largest single-day rally since WWII. For now, the market should be able to hold support at the previous lows and hopefully find a bit more relief into next week.

As I noted in the previous two weeks, we strongly lean toward the potential of the markets beginning a more extensive corrective process, much like in 2022. We will revisit that analysis in this weekend's newsletter. However, while we are concerned about a continued correction process as markets realign prices to forward earnings expectations, there will still be strong intermittent rallies. As noted last week, nothing in the market is guaranteed. Therefore, we continue managing risk accordingly, and as we stated last week and executed on Wednesday, we are now in "sell the rally" mode until the markets find equilibrium. When that will be, we are uncertain, so we continue to watch the technicals, make small moves within portfolios, and reduce volatility risk as needed.

This week, we will revisit the 2022 scenario and the "basis trade," which threatens the financial markets.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Credit Spreads Sending A Warning

As discussed in "Credit Spreads," the one market signal worth your attention is "credit."

Credit spreads reflect the perceived risk of corporate bonds compared to government bonds. The spread between risky corporate bonds and safer Treasury bonds remains narrow when the economy performs well. This is because investors are confident in corporate profitability and are willing to accept lower yields for higher risks. Conversely, during economic uncertainty or stress, investors demand higher yields for holding corporate debt, causing spreads to widen. This widening often signals investors are growing concerned about future corporate defaults, which could indicate broader economic trouble.

The two charts above show that credit spreads are essential for stock market investors. Watching spreads provide insights into the health of the corporate sector, which is a major driver of equity performance. When credit spreads widen, they often precede liquidity events, reduced corporate earnings, economic contractions, and stock market downturns. Widening credit spreads are commonly associated with increased risk aversion among investors. Historically, significant widening of credit spreads has foreshadowed recessions and major market sell-offs. Here’s why:

- Corporate Financial Health: Credit spreads reflect investor views on corporate solvency. A rising spread suggests a growing concern over companies’ ability to service their debt. Particularly if the economy slows or interest rates rise.

- Risk Sentiment Shift: Credit markets tend to be more sensitive to economic shocks than equity markets. When credit spreads widen, it typically indicates that the fixed-income market is pricing in higher risks. This is often a leading indicator of equity market stress.

- Liquidity Events: As investors become more risk-averse, they shift capital from corporate bonds to safer assets like Treasuries. The flight to safety reduces liquidity in the corporate bond market. Less liquidity potentially leads to tighter credit conditions that affect businesses’ ability to invest and grow, weighing on stock prices.

The recent market disruption caused by Trump's trade war has undoubtedly widened spreads between "risk-free" treasury yields and corporate bonds. However, while those spreads have widened, they remain well below the long-term averages. With inflation and economic growth slowing, this week's violent turmoil in the Treasury bond market is a signal of more than just recession concerns. As we noted in our Daily Market Commentary:

"On Monday, Treasury bonds had a sharp decline far beyond what the economic or tariff data suggested would be the case. We suspect that on Monday, there was forced liquidation through either margin calls or demand redemption of an institutional fund. The outsized selling and volume on a single day for bonds is highly unusual. The media excuses of “tariffs” or “economic concerns” are issues the bond market has known about for quite some time."

That type of sharp liquidation has historically been the issue of some liquidity events in the bond market. In this case, it appears to be the heavily leveraged arbitrage trade used by hedge funds.

The "Basis Trade" - A Near LTCM Moment

For a simple explanation of the basis trade, I asked Grok:

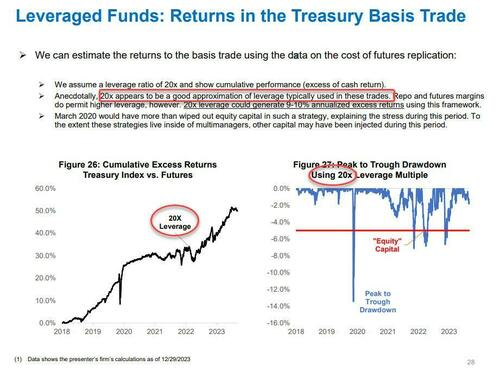

"The "basis trade" in the Treasury bond market is a strategy commonly used by hedge funds to profit from small price discrepancies between Treasury bonds (the cash market) and Treasury futures contracts. Here’s how it works: hedge funds buy Treasury bonds while simultaneously shorting Treasury futures (or vice versa), betting that the price gap, or "basis," between the two will converge. This trade relies heavily on leverage—often 20 to 56 times the initial investment—borrowed through the repurchase (repo) market, where Treasuries are used as collateral. The goal is to capture small, consistent profits from this arbitrage, amplified by the leverage while assuming the relationship between cash bonds and futures remains stable."

While the Fed suggests that the hedge fund basis trades leverage is above 50x, the Treasury Borrowing Advisory Committee wrote in January that "20x appears to be a good approximation of leverage typically used in these trades."

If you don't understand that math, it simply means that a 5% loss at 20x leverage is a 100% loss on the trade.

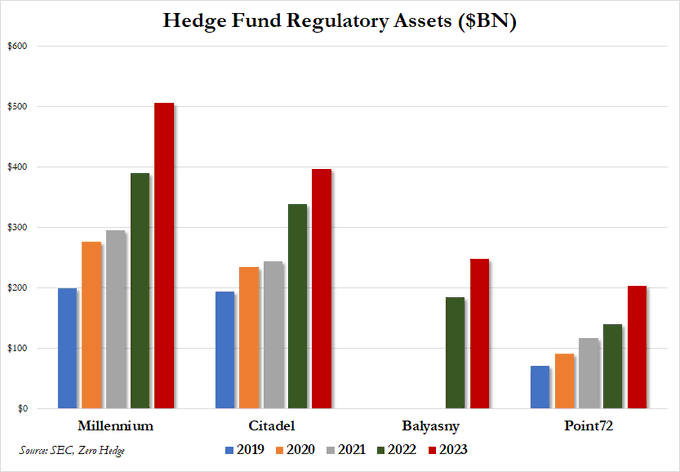

Furthermore, just for context, when Long Term Capital Management (LTCM) blew up over an unexpected move in interest rates, it cost the Fed $100 billion to keep financial markets afloat. As shown below, the current magnitude of today's hedge fund giants running these "basis trades" are multiples of LTCM.

As of this past week, the market liquidity event appears to be the "basis trade" unraveling. This turbulence is driven by hedge funds being forced to unwind their basis trade positions as Treasury prices drop (and yields rise.) That change in the value of the collateral backing those leveraged bets decreases, triggering margin calls from lenders. To meet those margin calls, hedge funds must sell their Treasury holdings, which exacerbates the downward pressure on bond prices, increasing yields, which triggers more liquidations.

This "liquidation event" in the bond market is very reminiscent of the "Repo Crisis" in 2019 and the "Dash For Cash" during the COVID-19 pandemic. It also reminds us of the "Silicon Valley Bank Crisis" in 2023. In all three events, the Federal Reserve stepped in to provide liquidity to the Treasury market. As Deutsche Bank noted on Wednesday:

"As far as the market circuit-breakers go, if recent disruption in the US Treasury market continues we see no other option for the Fed but to step in with emergency purchases of US Treasuries to stabilize the bond market (“emergency QE”). This would be very similar to the Bank of England intervention following the gilt crisis of 2022. While we suspect the Fed could be successful in stabilizing the market in the short-term, we would argue there is only one thing that can stabilize some of the more medium-term financial market shifts that have been unleashed: a reversal in the policies of the Trump administration itself."

For a deeper dive into the "basis trade," watch the following excerpt from the RealInvestmentShow:

The reversal of Trump's tariffs on Wednesday was not a "master class in negotiation." It was the admission that a terrible mistake was made, and the bond market drove that reversal.

However, is the problem resolved? It does not appear to be due to yields continuing to rise. Both credit spreads and interest rates are sending warning signs but are not yet at levels suggesting the entire funding market is broken. The bond market is functioning, and the 10-year auction on Wednesday went well. Furthermore, hopefully, the administration's 90-day pause on tariffs is the first step in the right direction to end the trade war entirely or at least reduce it significantly.

Regardless, I doubt that we are done with market volatility. The damage done to the bond market so far is likely not over yet, and while we may get a short-term reprieve, I suspect there will be another round of bond market stress before we are done.

That is particularly the case given the recent triggering of our most crucial risk-management signal.

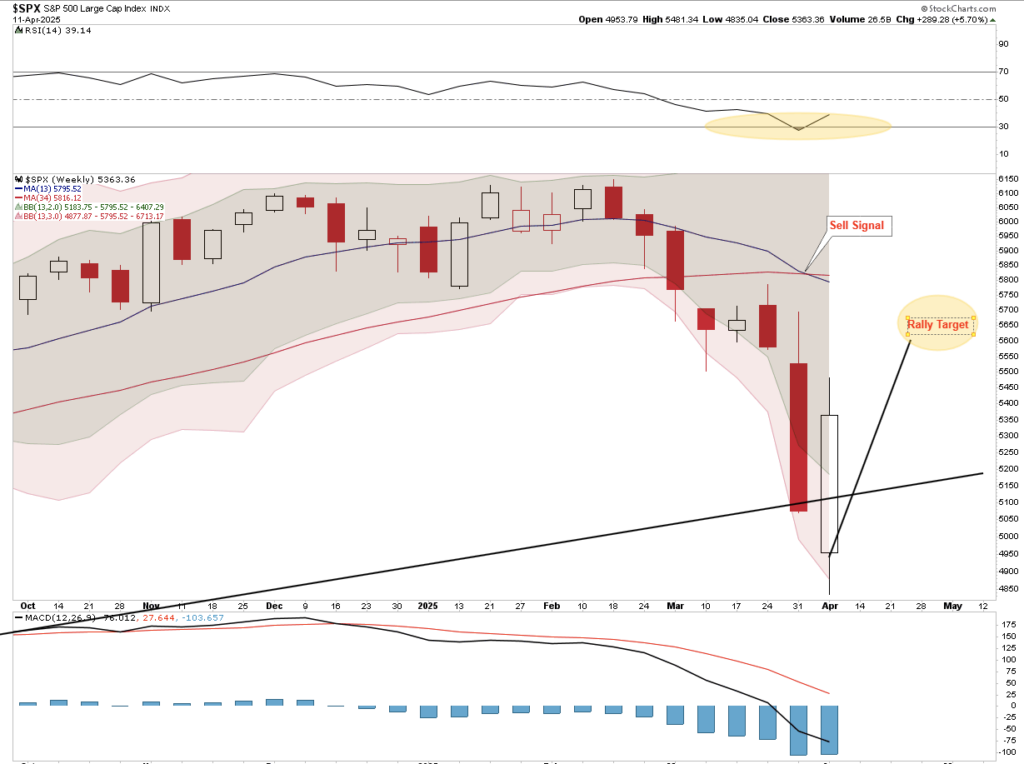

Despite The Tariff Reprieve - Sell Signal Triggers

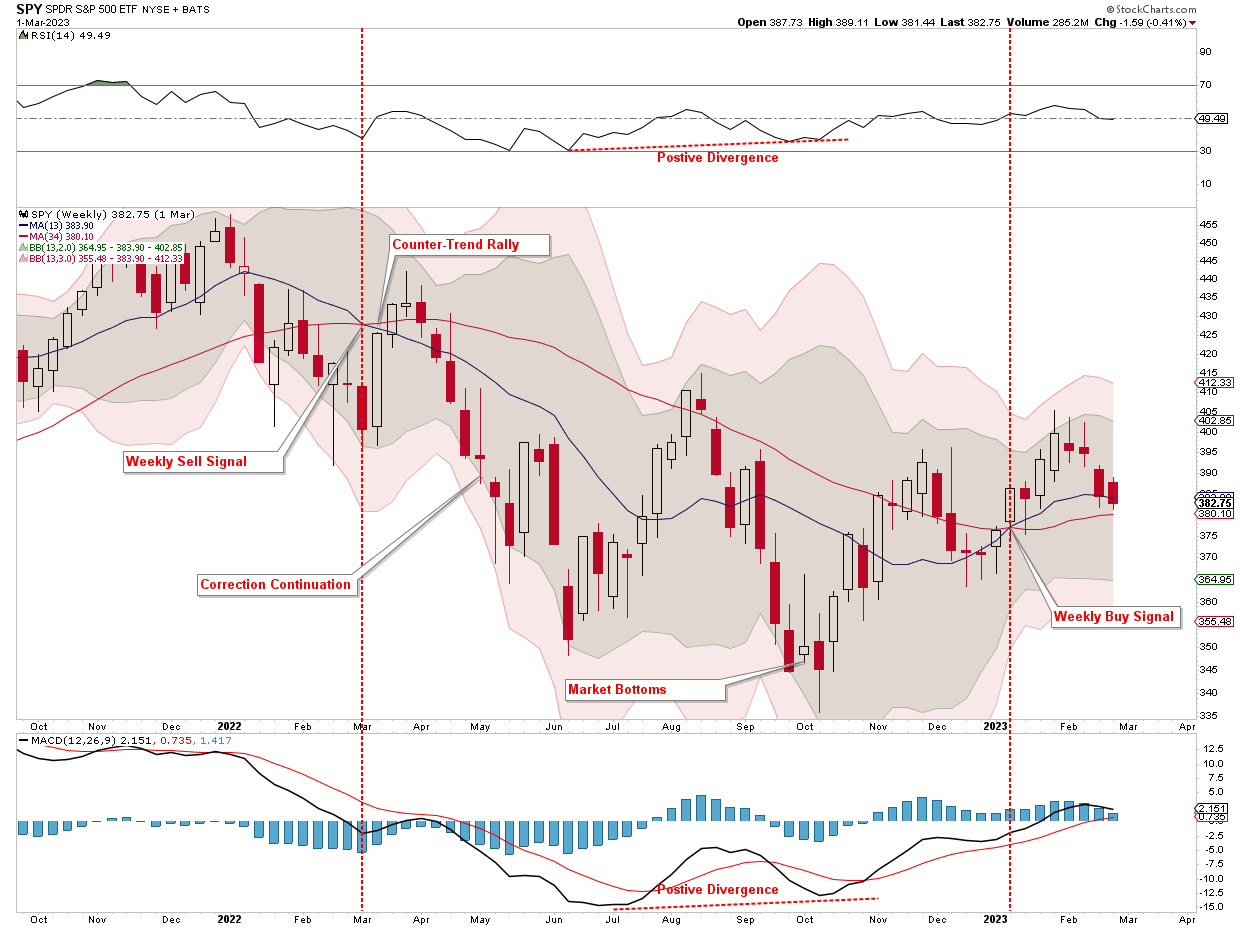

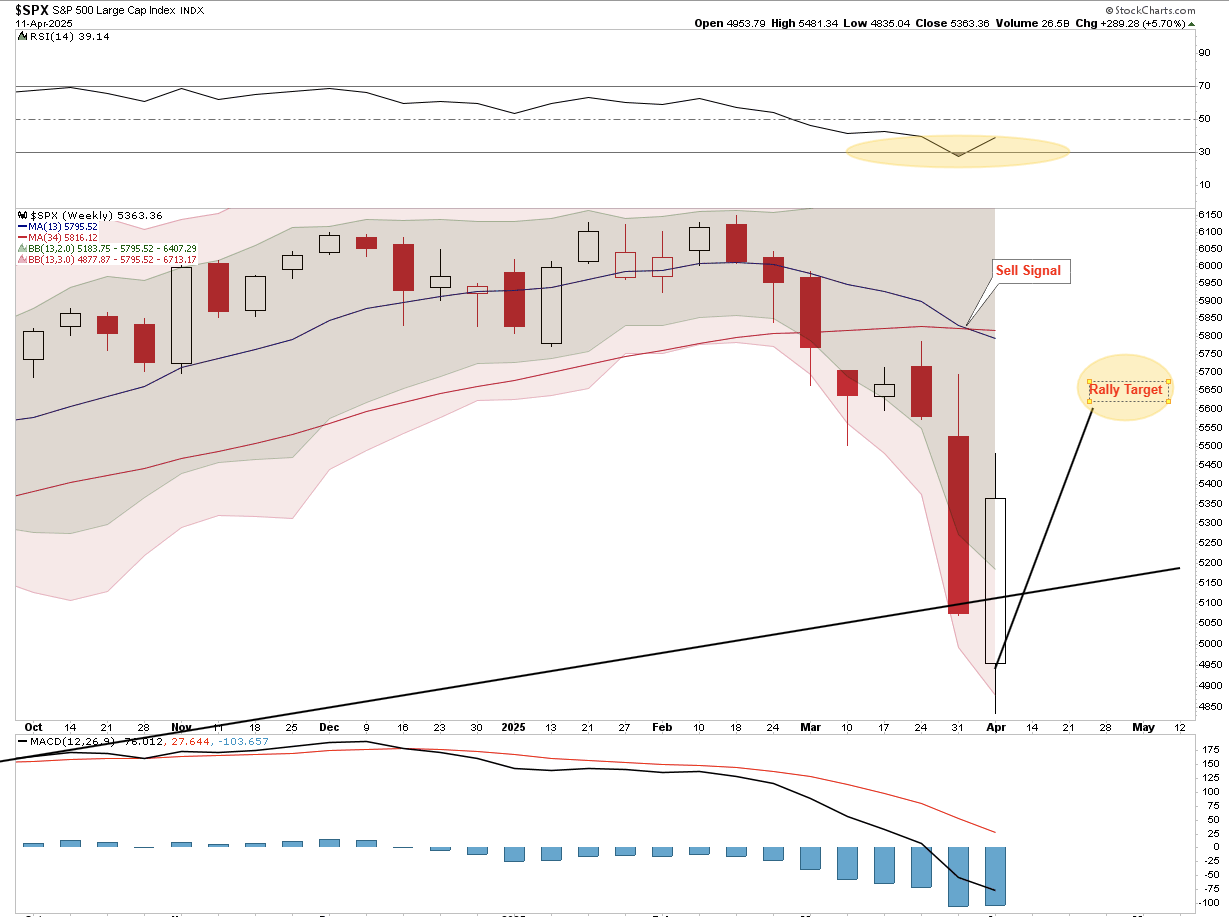

Last Tuesday, I posted "Failure At The 200-DMA" which discussed the importance of the weekly "risk management" signal.

The chart below is a long-term weekly chart of RSI and MACD indicators. I have denoted when the indicators are trading in bullish and bearish trends. The primary signal is the crossover of the weekly moving averages, as noted by the vertical lines. While the MACD and RSI indicators provided early warning signals, the moving average crossover confirmed a market correction or consolidation. These indicators will not necessarily cause a risk reduction precisely at the top. However, they generally provide sufficient indications to reduce risk ahead of more significant market corrections and consolidations.

I have updated the chart for this week's market close. The massive rally on Wednesday completed the 50% retracement from the low, which allowed us to reduce portfolio risk in portfolios. Most likely, the correction process that started with the break of the 200-DMA is likely not yet complete. We will discuss those actions in the "How We Are Trading It" section below.

The market tells us that the risk of a more significant correction or consolidation process is increasing, particularly as economic growth slows and valuations are repriced for reduced earnings growth expectations. As we noted in that article two weeks ago:

"While such does not preclude a significant counter-trend rally in the short term, the longer-term risks seem to be growing."

So far, the current corrective cycle, including the massive reflexive rally this week, remains very reminiscent of the 2022 correction. If we enter another corrective period like 2022, given some of the same technical similarities, there is a decent “playbook” to follow despite substantial differences. In 2022, the Fed was hiking rates, inflation was surging, and economists were convinced a recession was on the horizon. As noted above, earnings estimates were revised lower, causing the markets to reprice valuations. Today, the Fed is cutting rates, and inflation is declining; however, due to Trump's trade policies, the risk of recession is rising, and earnings estimates likely remain overly optimistic. We must realize that the analysis can change as time passes.

However, let's review the 2022 correction process. In March 2022, the market triggered the weekly “sell signal” as it declined. Notably, the market rallied sharply after the “sell signal” was initially triggered. Much to the same degree as we saw on Wednesday. Such a rally is unsurprising, as when markets trigger “sell signals,” they are often profoundly oversold in the short term. However, that rally was an opportunity to “reduce risk,” as the failure of that rally brought sellers back into the market. The “decline, rally, decline” process repeated until the market bottomed in October. One of the defining things we will be looking to identify where the current market will bottom is the positive divergence of momentum and relative strength. Even though markets continued to struggle in the summer or 2022, the positive divergences suggested that market lows were near.

In that article two weeks ago, we stated:

"With the market approaching decently oversold levels, I expect a rally to start as soon as this week or next."

That rally occurred, and we are starting to track the initial "sell signal" process as of 2022. Such suggests we could see a further rally over the next week.

We used the rally this week to reduce portfolio risk and raise cash levels, and we will continue that process on a further rally. While no two corrections are the same, it is essential to understand that corrections do not occur in a straight line. With the weekly sell signal in place, investors should expect that we will likely see further declines, which will likely be punctuated by short-term rallies that allow investors to rebalance portfolio allocations and reduce risk as needed.

With that understanding, this is what we did this past week.

How We Are Trading It

Last week, we stated:

"As noted, we expect a sizable rally soon. While such a rally will undoubtedly make investors more bullish on the markets, we will use that rally to reduce portfolio volatility until a more durable market bottom is identified. Furthermore, we are triggering an important weekly sell signal. Still, the markets are simultaneously three standard deviations below their longer-term moving average, challenging the rising trend line from the October 2022 lows. Such oversold conditions typically precede short-term rallies, allowing us to reduce exposure to equities between 5500 and 5700. While the rally could be more significant, we will use those levels to begin risk reductions."

We followed our instructions from last week, which stated that we would:

- Reduce current positions by 1/4 to 1/2 of their current target weights.

- Increase cash levels

- Raise stop loss levels on long-term positions.

- Sell positions that have technically violated previous support levels or exceeded risk tolerances.

- Add to positions that are positioned to benefit from further market stress.

All the trades are listed at the bottom of this week's newsletter.

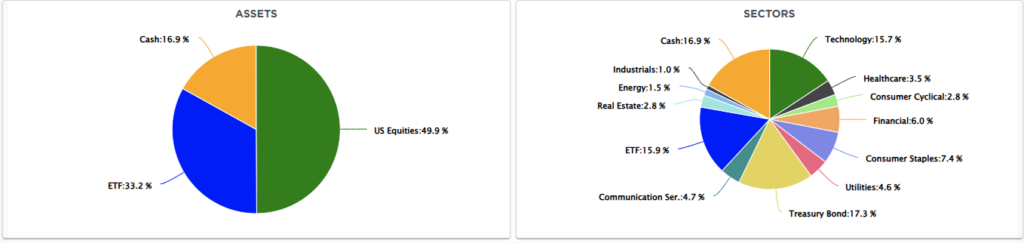

Those actions reduced equity exposure to 50% and increased cash to 17%. However, the portfolio has a 2.5% short-S&P 500 position, which brings the actual equity allocation to 47.5%.

Note: We expect the market to rally more from current levels over the next week or so and could challenge the 200-DMA. However, that is likely the point where sellers will re-enter the market. Markets rarely bottom without retracing toward the previous lows or setting new lows. Given the technical damage to the market, we suspect we will see a pullback before this correction process is over.

We will continue to monitor and adjust the portfolio accordingly. At some point, the valuation reversion will be complete, allowing us to reconfigure portfolio allocations for a more bullish environment. When that event occurs, we will reduce fixed income, shift income allocations to corporate bonds rather than government bonds, and overweight equity allocations in portfolios.

However, that is a conversation we will have in more detail in the future. For now, market conditions remain uncertain. Preparing and adjusting strategies can help investors navigate volatility confidently. As technical indicators flash warning signs, a well-structured risk management approach will protect capital and preserve long-term gains.

I hope this helps.

Feel free to reach out if you want to navigate these uncertain waters with expert guidance. Our team specializes in helping clients make informed decisions in today’s volatile markets.

Have a great week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

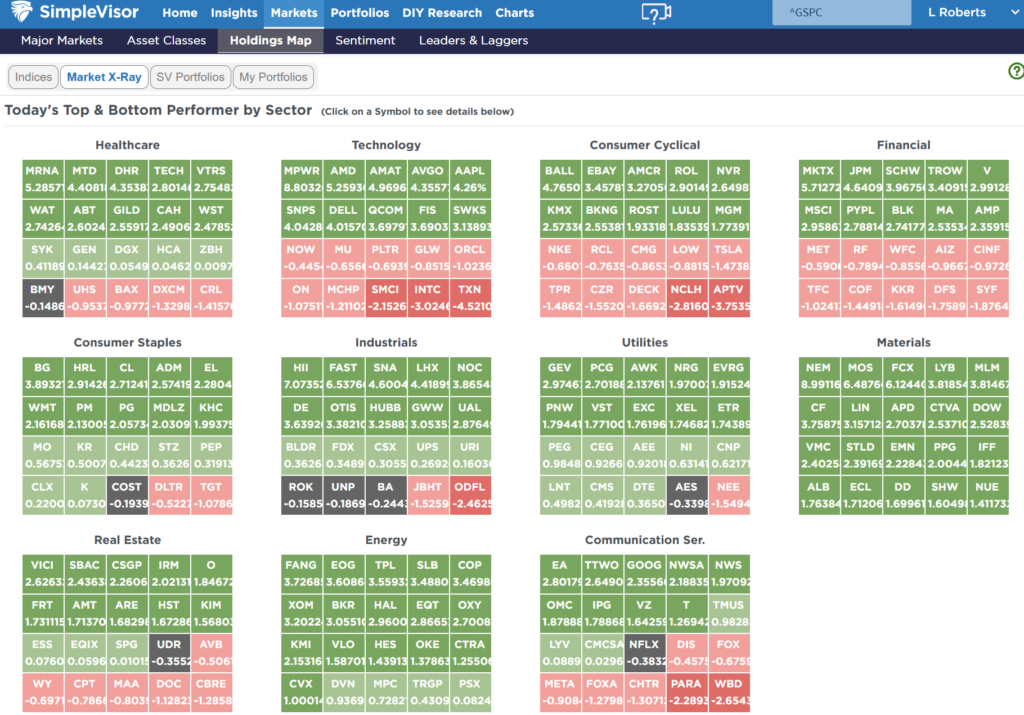

SimpleVisor Top & Bottom Performers By Sector

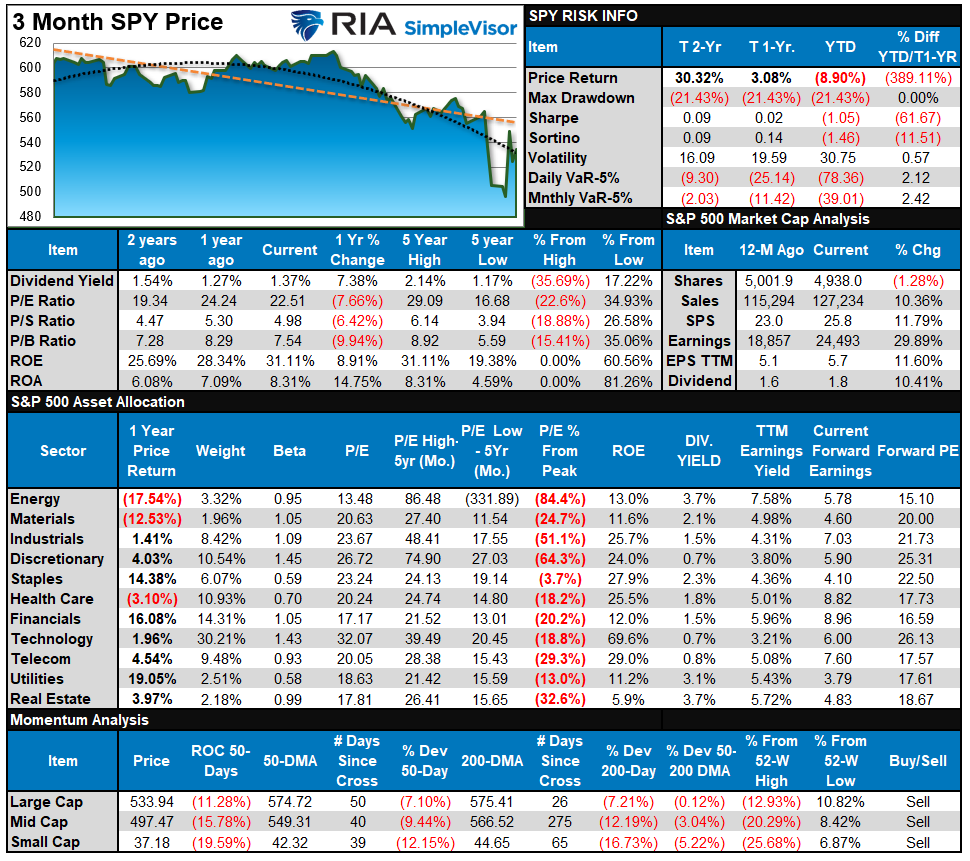

S&P 500 Weekly Tear Sheet

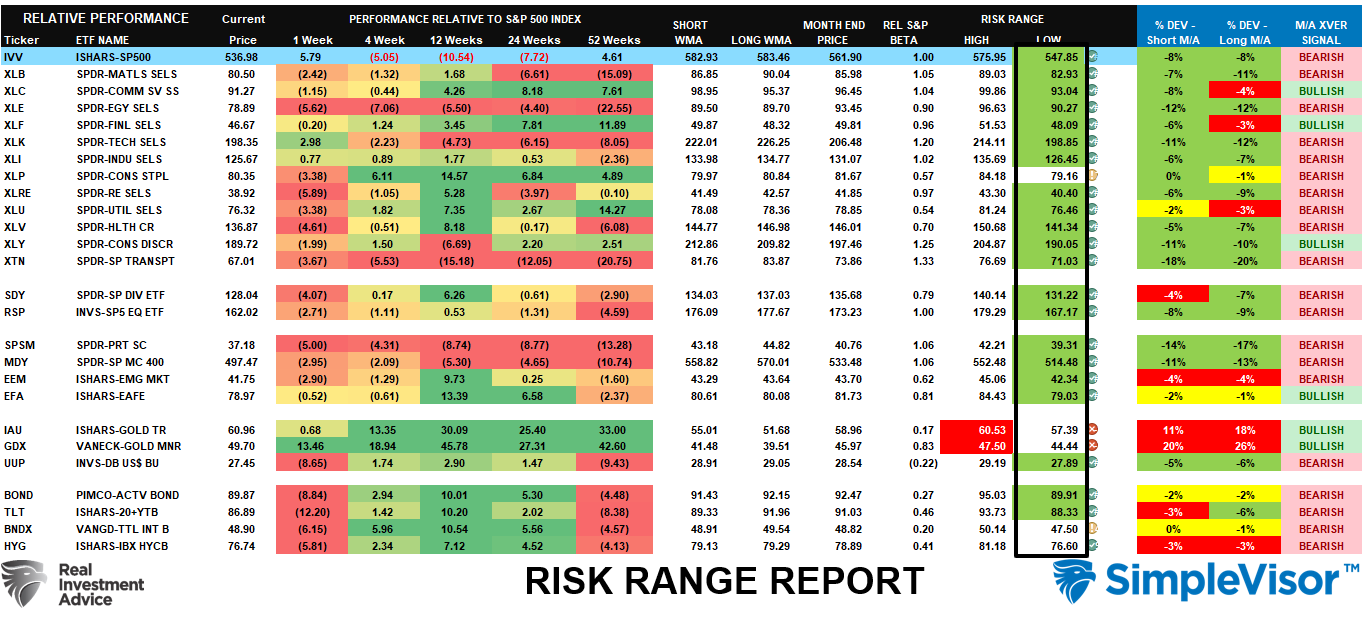

Relative Performance Analysis

Stocks had another very volatile week, with the bond market getting crushed as forced selling erupted over the "basis trade." Such was quite the reversal from last week when bonds were the shining star of the markets. Nonetheless, as we stated last week:

"Given the extremely deep oversold of every sector and market, I would expect a tradeable rally early next week, barring any more antics from the White House. As you will note in our Risk/Reward ranges below, while markets and sectors are well outside of normal tolerances, suggesting a rally is likely, the number of bearish divergences will keep markets contained for quite some time. Use rallies to reduce risk and rebalance exposures as needed."

That remains the case this week. More upside is likely as the markets are not overbought yet, but we will want to continue to rebalance and reduce equity risk on that rally as needed.

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 27.88 out of a possible 100.

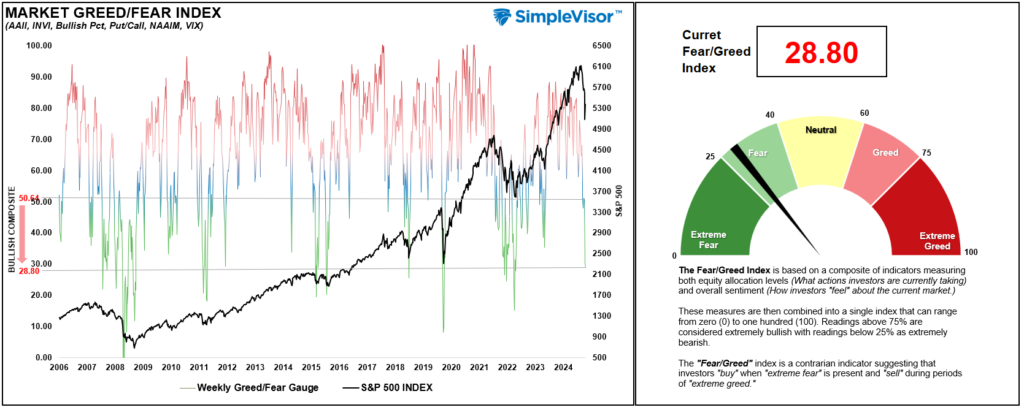

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90.

The current reading is 28.80 out of a possible 100.

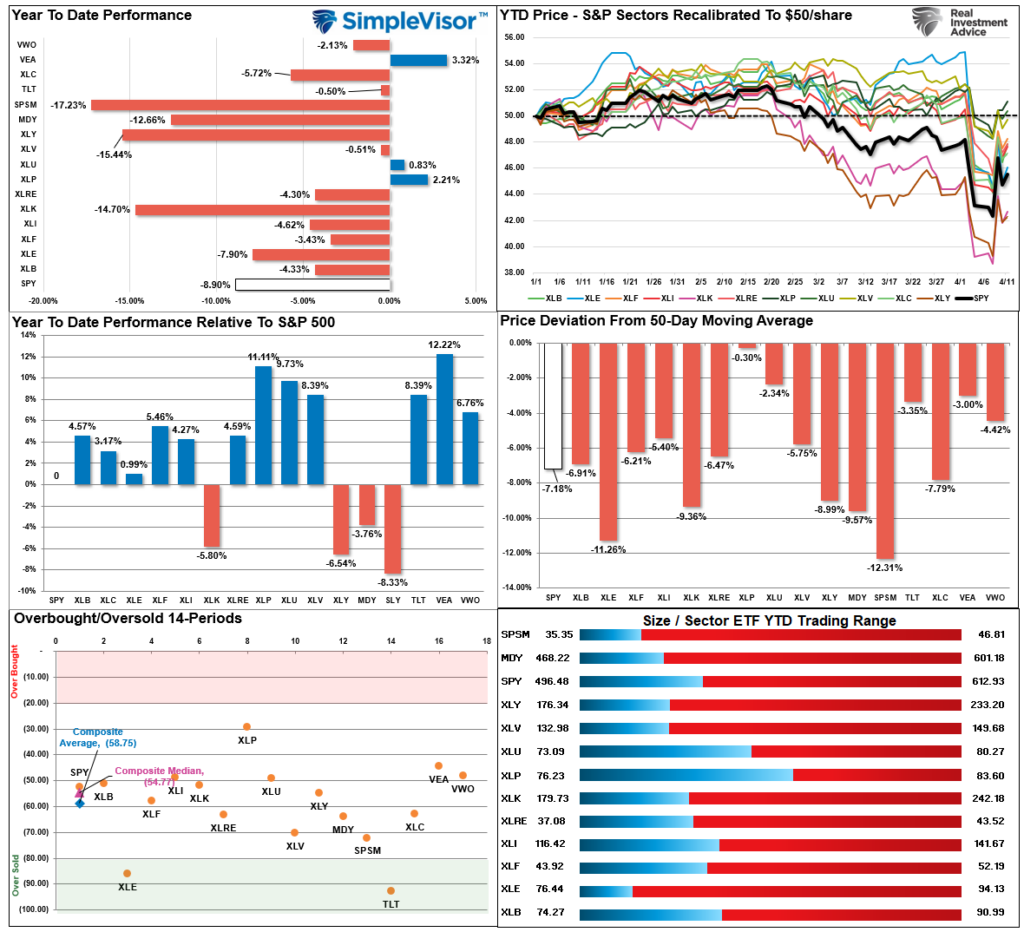

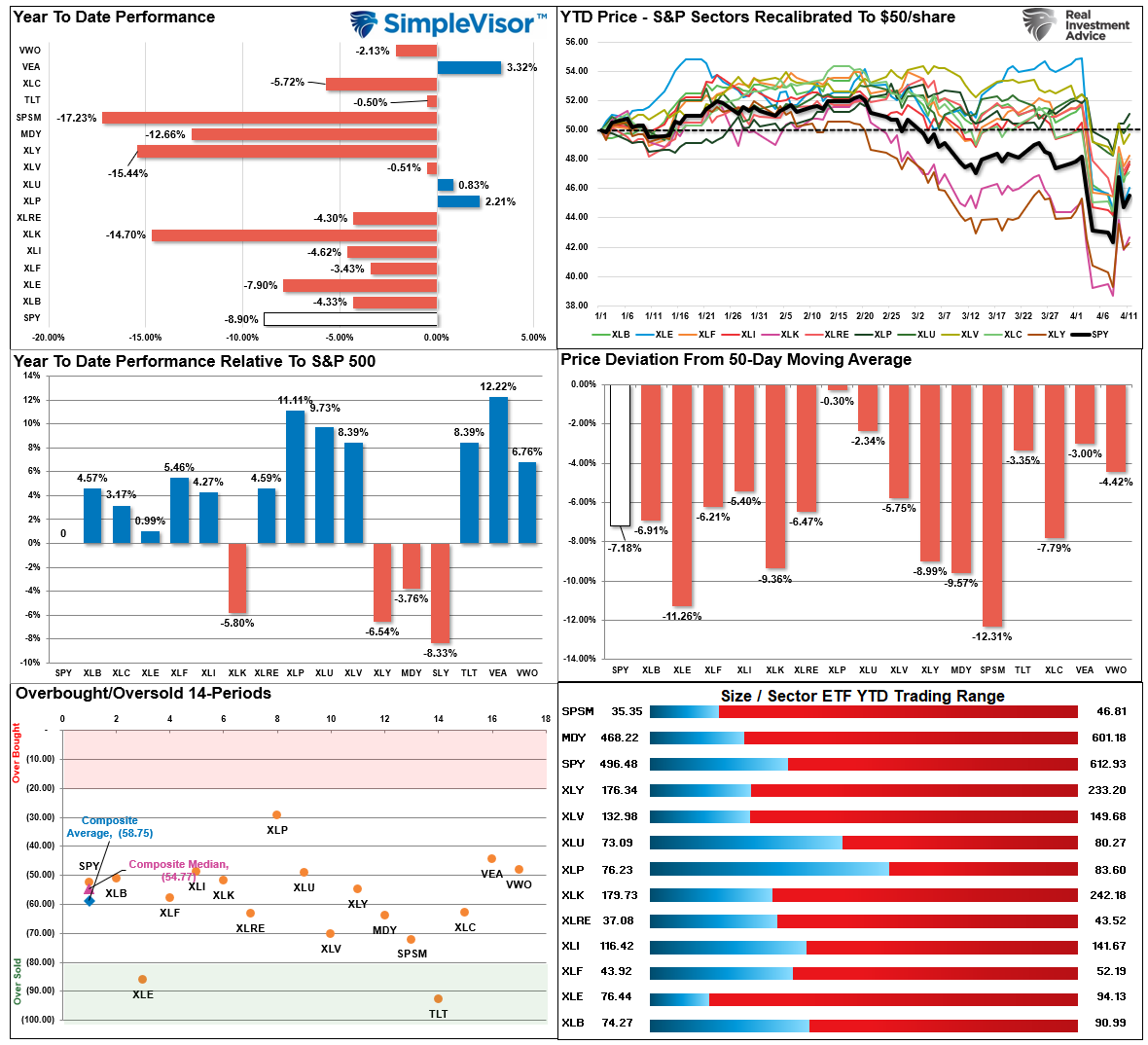

Relative Sector Analysis

Most Oversold Sector Analysis

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

As noted last week:

"The crash this past week sent every market and sector below normal monthly risk ranges. The only other time I have seen something like this was during the 2020 pandemic shutdown of the economy. Notably, these deviations provide opportunistic entry points for investors in the short term. More opportunities to add exposure now reside in Financials, Technology, Discretionary, and Communications. Take profits in Bonds after their recent run higher."

That advice worked, as bonds crashed and stocks made a decent move higher off their lows. The situation is reversing, with bonds very oversold and equities moving higher. Use the rally to reduce equity risk as needed, and watch the bond market for signs the "basis trade" is rectifying itself. There is a very good opportunity to add long-duration bonds to the portfolio coming soon.

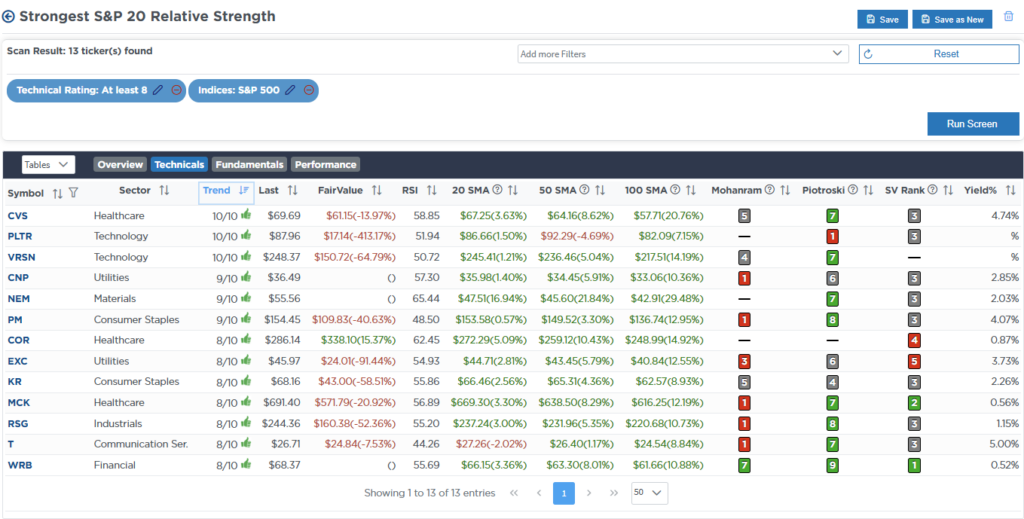

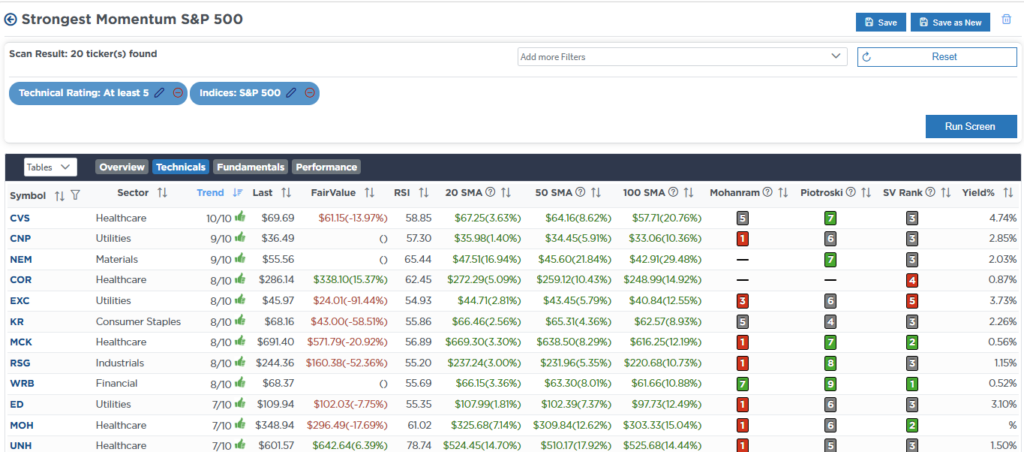

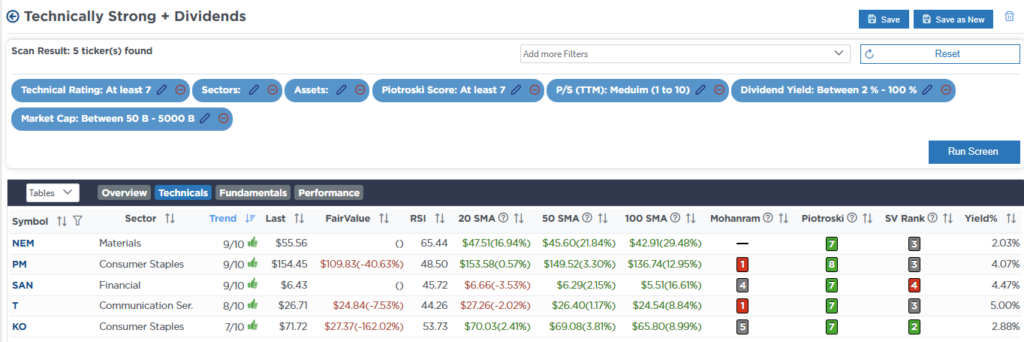

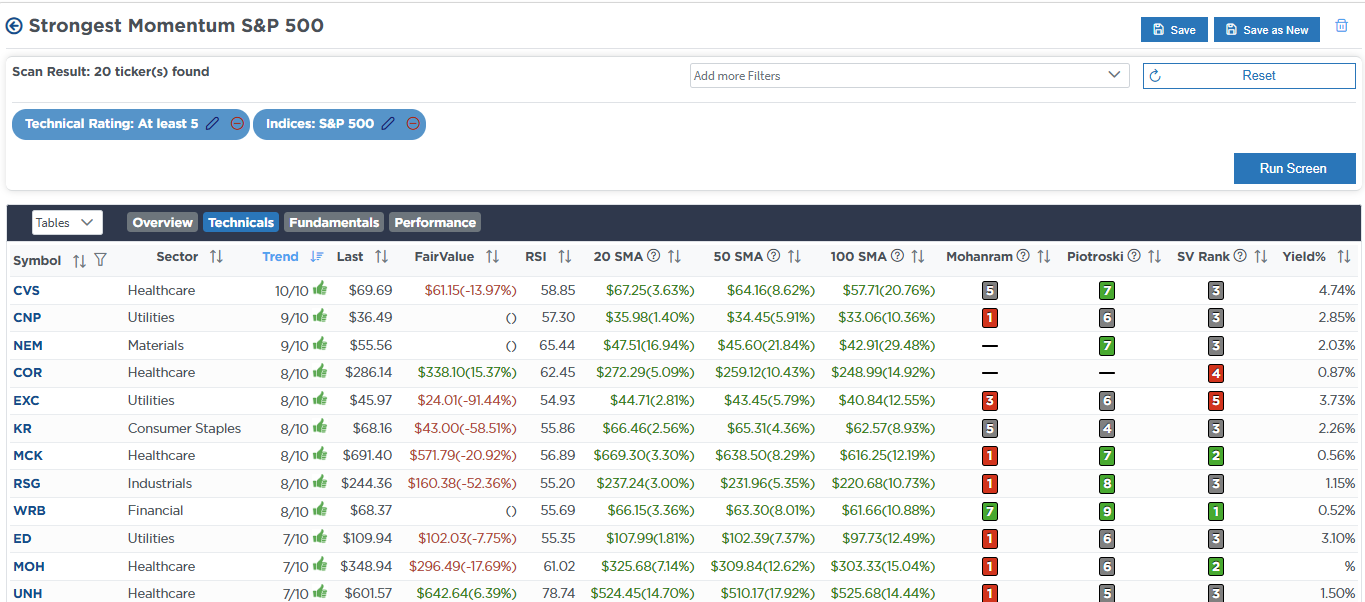

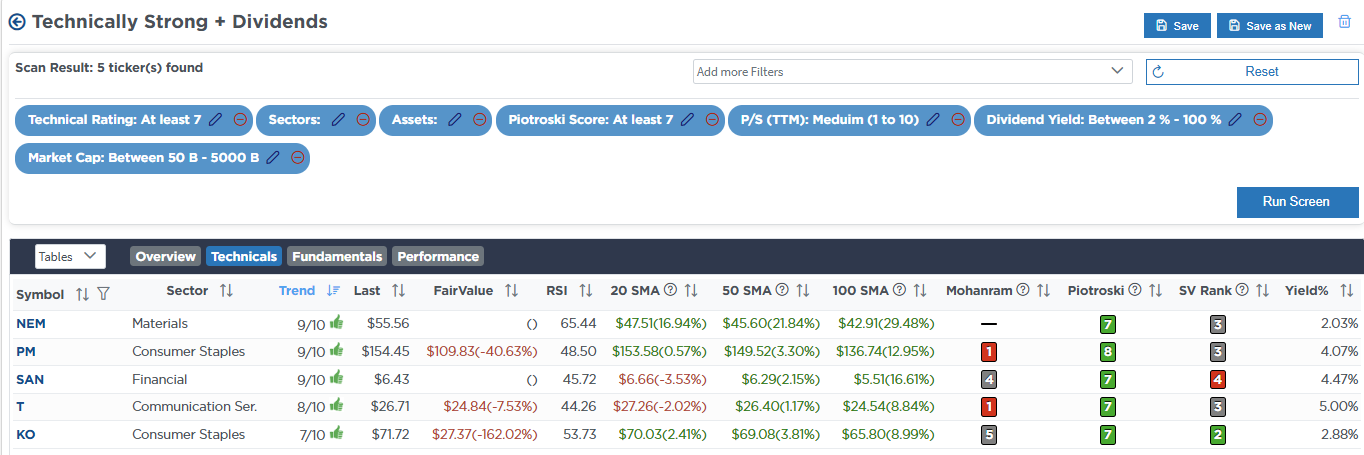

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week, we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technical Strength W/ Dividends

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technically Strong With Dividends

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

Apr 9th

"This week’s sell-off triggered our weekly sell signals, historically suggesting a much larger potential corrective cycle is in place. However, when this signal is triggered, markets tend to be very oversold and set up for a near-term rally where we can reduce risk at a better level. At the same time, a more critical liquidity event is brewing in the bond market.

The recent spike in bond yields starting Monday is a forced liquidation event in the bond market. It suggests rising credit risk, particularly in hedge funds’ highly leveraged arbitrage trades. In 2019 and 2020, we saw similar events where the Federal Reserve was forced to step in and become a “buyer of last resort.” While that hasn’t happened yet, if rates keep rising as sharply as they have been, the Fed will be forced to maintain financial stability in the credit markets. As such, we are shortening our bond duration sharply until this crisis passes and shifting exposure from stocks most impacted by credit risk increases.

Once this crisis is over, we will rebalance portfolios and increase duration to take advantage of slower economic growth and a potential recession."

Equity Model

- Reduce ABBV to 2% of the portfolio.

- Reduce LLY and JPM to 1.5% of the portfolio.

- Increase BRK.B, NVDA, and PLTR to 3% of the portfolio

- Increase PANW to 2.5% of the portfolio

- Add to GOOG to bring it up to weight at 4.5% of the portfolio

- Reduce EDV to 5% of the portfolio and increase IEI to 13.5%.

ETF Model

- Reduce XLV to 6% of the portfolio.

- Reduce XLF to 4% of the portfolio.

- Increase MGK to 5% of the portfolio.

- Reduce EDV to 5% of the portfolio and increase IEI to 13.5%.

Dividend Equity Model

- Sell 1/2 of TFC, FRT, SPG, MDT, O, JPM, and GS

Apr 10th

"As we have discussed over the last two weeks, the deep oversold condition of the market would lead to a sharp reflexive rally that should be sold into to reduce risk and rebalance portfolios. That rally came yesterday, and we are reducing risk across all models this morning. The first step is to reduce exposure to positions, reduce target weights, and increase cash levels. The next step, if needed, will be to add a short position in portfolios. Today is step one."

Equity Model

We are reducing the following stocks to new portfolio target weights:

- COST – 3.5%

- AAPL – 3.25%

- PLTR – 3.0%

- PG – 3.0%

- AMZN – 2.75%

- NVDA – 2.5%

- PANW – 2.5%

- WMT – 1%

- ABBV – 2%

- RTX – 1%

ETF Model

We are adjusting the following ETF holdings to new portfolio target weights.

- XLK – 10.0%

- XLC – 6.5%

- MGK – 6%

- XLP – 6%

- XLI – 1.5%

- XLY – 2.0%

- XLU – 5% (Increase)

- REM – 1%

- XLRE – 1%

Dividend Growth Model

- Reduce META, AAPL, GOOG, AMZN, NVDA, and MSFT to 4% of the portfolio each.

- Reduce MMM, KO, MO, DUK, KMI, AEP, NLY, AMLP, VZ, IBM, ABBV, XOM, and KMB to 2.5% of the portfolio each.

Apr 11th

"With the bond market in turmoil and volatility running at elevated levels, we are reducing equity exposure today in both models by adding 2.5% of an S&P 500 Short Position (SH). This temporary risk reduction measure will be removed once the bond market crisis passes. We will likely increase this position to 5% of the portfolio if the market musters a near-term rally to overhead resistance."

Equity Model

- Add 2.5% of the S&P 500 Short ETF (SH)

ETF Model

- Add 2.5% of the S&P 500 Short ETF (SH)

Lance Roberts, C.I.O., RIA Advisors

The post Basis Trade Sent Yields Soaring – Is It A Warning? appeared first on RIA.

-

Site: The Orthosphere

Promoted (as slightly edited) from a comment on a previous post.

Apologists for atheism often argue that theism is intellectually costly; that, i.e., atheism postulates less, and is therefore less vulnerable to Ockham’s Razor. Isn’t it simpler, they ask, to suppose that there is nothing but the cosmos, than to suppose that there is the cosmos and its creator and sustainer?

But theism is far more parsimonious – categorically more parsimonious – than atheism.

Theism supposes that the ultimate basis or source or reason or cause or explanation (these terms all coterminate) of things is an Ultimate Being who, as ultimate, is, by definition of “ultimate,” himself ultimate along all dimensions of virtue or excellence, and is therefore necessary, actual, eternal (and what is more, also temporal if he feels like it, indeed angelic or even animal, like us, should that be apt to his purposes) omniscient, infinite, boundless, the bound and limit of all things, Prime Mover, Being as such, the Good itself, Beauty as such, Justice as such, Mercy as such, himself the whole Truth, Rationality as such, creative, One, Many, almighty, Love o’erflowing, personal, suprapersonal, changeless, by his very being enabling and encompassing and furnishing all change, ubiquitous, everywhere and everywhen immanent, the source and logic of each particular being and of all beings together, and superlimely transcendent to each and all particular being.

We need not try to understand how a single being could be all those things. Indeed, on the definition of “ultimacy,” there is no way our less than ultimate minds could possibly succeed thereat (which is why we find among Xian theologians a unanimous cataphatic insistence on apophatic theology (that agrees perfectly with the mystics of every tradition: neti, neti; not this, not that). Indeed, the Ultimate must be perfect along many dimensions of perfection that we do not or even cannot know about at all (we cannot understand what greatness is like to a bat, but we can feel sure that whatever it is, the Ultimate manifests it maximally). And on the definition of “ultimacy,” all these perfections must logically coterminate in a One (for, one who lacked any of them would be subultimate).

Theism then proposes that the ultimate basis of things is an Ultimate Thing, who as ultimate is thingness as such, and the condition thereof.

Atheism on the other hand supposes that the ultimate basis, source, reason, cause or explanation of things is … nothing. And this is to suppose that, in the final analysis, there just is no such thing as a basis, source, reason, cause or explanation of things; of, NB, anything.

Theism says that the reason of things is God, who is necessarily, and who is what he is (logical, good, rational, beautiful, and so forth) necessarily (there are solid modal proofs of these propositions). It says that there is indeed a reason of things.

Atheism says that there is no reason of things.

That is a massive leap, a categorically greater leap; it is a leap into the zero of categories, so of any meaningful terms, then of discourse, thus of understanding. It is the biggest possible – and least warranted – intellectual leap. It is a leap into nothing; into mental vacuum; into a fathomless abyss; into utmost ignorance; into the Outer Darkness.

And, lo, into an obligatory philosophical reticence (never observed by public apologists for atheism, NB) that verges upon total silence; upon just the sort of humility before what to finite minds such as ours must incorrigibly appear mysterious: neti, neti.

A consistent and thoroughgoing atheism then tends to the same final – let’s call it ‘ultimate’ – epistemological terminus ad quem as a consistent and thoroughgoing theism. The remnant question, then, is this: what makes more sense, the everythingness, plurality and richness of theism, or the nothingness, emptiness and desolation of atheism?

Ineluctably worldly beings such as we are naturally more attracted to the former, which explains the dismal popularity of atheism through the millennia. But, at last, even these terms – nothingness and everythingness – eventually coterminate upon something (call him a thing, despite the nothingness) that transcends our terms – that, as thus transcendent, must remain to us ultimately (that term again) mysterious (not unlike our own being, after all) – and incorporates and reconciles them, all.

It would be odd – it would be nonsense – to suppose that the Ultimate, properly considered, might fail at such a reconciliation of all things.

There simply *must be* a reconciliation of all things. Otherwise, this is all just chaos, and all our works are stupid nonsense. The problem with that latter conclusion is that *every human feeling whatever* – including all the propositional feelings of intellectual life – argues otherwise.

You can’t be an atheist, or a determinist, except by engaging in activities that presuppose the falsity of atheism and determinism.

-

Site: Mises InstituteFar from being a true measure of economic health, GDP is a misleading economic statistic that implies consumer and government spending grow the economy. When government spends, GDP increases.

-

Site: Ron Paul Institute for Peace And Prosperity

It is an improvement that President Donald Trump has made himself many times more available for media questions than did Trump’s predecessor Joe Biden and Trump’s November election opponent Kamala Harris who notoriously made great effort to avoid reporters’ questions. Still, it would be nice if Trump told his White House employees to knock off their use of petty rules limiting media access.

Since February 13, Associated Press (AP) reporters have been barred from White House media access because the AP continued to use the term “Gulf of Mexico” after Trump declared in an executive order that the body of water should henceforth be called the “Gulf of America.” Get over it already. That’s how language works. People don’t always call things by the same name, and politicians don’t have absolute power to settle the matter. Even today, 16 decades later, battles of the Civil War are regularly called by two alternative names — one originating from use by the United States side and the other from use by the Confederate States side. Indeed, even the war itself does not have a settled name. The War Between the Sates and the War of Northern Aggression are two alternative names people use, among others. And I wonder if some reporters take a highway en route to press conferences while others take a parkway. Might White House employees consider taking a turnpike to be intolerable?

This week comes the revelation that White House employees are refusing to answer emailed questions from reporters whose emails include mention of the pronouns the writers prefer people use when referring to them. Are the White House employees so fragile that they can’t handle seeing someone noting his “preferred pronouns” are “they/them” or whatever? If so, it seems these employees are in the wrong line of work. Either that or maybe the executive branch needs to set up a safe room with teddy bears for them so they can deal with the trauma.

Then again, I may have been too caught up in recent trends in assessing this latest policy that results in evading questions. It could just be the doing of a jerk or a ploy to prevent the production of undesired reporting. Either way, it should end.

Why has Donald Trump put up with these thin-skinned policies preventing the answering of questions from people who use “wrong” or “hurtful” words that ordinary Americans deal with routinely? This evasion of reporters’ queries is ridiculous, and it stands in the way of having an open and accountable government.

-

Site: Mises InstituteJörg Guido Hülsmann explores humanity’s timeless drive to get something for nothing—and how free markets encourage true generosity while central banking and the welfare state undermine it.

-

Site: Mises InstituteChapter 12 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 9 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 6 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 3 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteThe Introduction to Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 11 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 8 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 5 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 2 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteThe Preface to Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteThe Conclusion to Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 10 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 7 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 4 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Mises InstituteChapter 1 of Abundance, Generosity, and the State: An Inquiry into Economic Principles audiobook.

-

Site: Rorate CaeliThe Pope's HealthArchbishop Héctor AgüerEmeritus of La Plata, ArgentinaBuenos Aires, April 8, 2025Francis was hospitalized for 38 days at the Gemelli Hospital in Rome for treatment of a double pneumonia. Thanks be to God, he got better and returned to the Vatican, to his usual place in Casa Santa Marta.I have prayed a lot for the Pope, for the health of his body and soul. In the present New Catholichttp://www.blogger.com/profile/04118576661605931910noreply@blogger.com

-

Site: Mises InstituteRecent moves make clear the tax agency plans to grow, not fade away.

-

Site: PaulCraigRoberts.org

Putin’s Pursuit of a New Yalta

Paul Craig Roberts

Kiev breaks energy ceasefire five times in 24 hours.

And these violations of the agreement are on top of previous violations.

So why is Russia complying with a non-existent ceasefire?

If Kiev will not comply with a partial ceasefire, why would Kiev comply with a full ceasefire?

How can Trump expect Putin to agree to a full ceasefire when Ukraine? Washington? NATO? Will not comply with a partial ceasefire? Why is Trump destroying Putin’s confidence in the negotiations with threats of more punishments for Russia?

Sometimes Trump sounds like Hitler, who trying to keep German war morale alive boasted of “super weapons.” Trump is claiming American super weapons “unlike anything the world knows.” Is there a neoconservative mole in the Trump administration encouraging Trump’s use of threats to prevent a peace agreement?

Moreover, who is not complying? Kiev or US/NATO? According to the CIA confession published in the NY Times, it is Washington’s war with Russia, not Kiev’s war. Washington calls the shots, not Zelensky.

In my opinion, Putin is complying with a broken agreement because he is trying to use the conflict to arrive at a Great Power Understanding like Yalta, an unrealistic hope that prevents a Russian victory.

https://www.rt.com/russia/615601-energy-ceasefire-ukraine-attacks/

-

Site: PaulCraigRoberts.org

The Tariff Issue Again

Paul Craig Roberts

The whore media is doing its best to misrepresent the tariff issue and to cause hysteria that causes stock market volatility and fears of world recession. One of the anti-Trump propaganda ministries that poses as financial media went so far as to claim that Trump has caused a “regime shift whereby US Treasuries are no longer the global fixed-income safe haven.”

Once upon a time the New York Times, the Financial Times, the Economist, the BBC, the US TV networks were semi-reliable. Today they are nothing but propaganda ministries.

Trump has “paused” the threatened tariffs. Why? Because as I have reported in columns and interviews they are a negotiating tool with which to reach agreements. Trump paused the tariffs, because the tool worked. Seventy-five countries have agreed to negotiate a solution to Trump’s concerns.

How did the excrement that pretends to be a media report Trump’s success? “The most significant retreat by Trump in his term so far.” “Faced with a world recession, sharp selloff of equities and bonds and plunge in oil prices, Trump abandoned his crackpot tariffs.”

The Western media, especially the one in the US, has never served the West well. The US media covered up the assassinations of President John Kennedy and his brother Robert Kennedy. The media first encouraged, then misrepresented, the Vietnam War. The media used the CIA-orchestrated “Watergate” to hound President Nixon out of office. The media tried, but failed, to destroy President Reagan as a somnolent Grade-B movie actor who slept through cabinet meetings. The media covered up 9/11. The media supported obvious lies, such as “Saddam Hussein’s weapons of mass destruction,” “Assad’s use of chemical weapons against his own people,” accused Gaddafi of ” being an authoritarian administration that systematically violated human rights and financed global terrorism in the region and abroad” (Wikipedia, the worst liar on earth). The media makes excuses, or does not cover, Israel’s extermination of Palestine and the Palestinian people. The media lies through their teeth about “the Russian invasion of Ukraine,” about alleged evils of Iran and China.

When people in the Western world are confronted by nothing but lies and propaganda serving as news, what understanding can they have?

Consider the Iranian issue. Iran has not threatened the US in any way, yet labors under Washington’s sanctions and war plans to attack Iran. For many years the Israel Lobby has been trying to get Americans to attack Iran for Israel. Trump, who appears to be an Israeli puppet instead of a strong American president, is threatening Iran with devastating attack. But does he mean it, or is it, like the tariff threat, just another negotiating instrument?

If I were Trump, I would not want any wars, because wars are all-consuming, and the domestic agenda would be put on the back burner. I think that Trump wants to avoid all wars so that he can deal with America’s real enemy: the American Establishment.

It will be interesting to see who is strongest, Trump or the war establishment.

-

Site: PaulCraigRoberts.org

US to screen migrants for anti-Semitic posts

Trump cannot deport illegals for being illegal or criminal, only “migrants” (notice the euphemism for illegals) for exercising free speech and posting criticism of Israel on social media. According to the Israel Lobby any criticism of Israel or Jews is anti-semitic.

-

Site: PaulCraigRoberts.org

A land of mass graves and mercenaries – Can this genocide be stopped?

https://www.rt.com/africa/615384-prospects-establishing-parallel-government-sudan/

Finally, Russian media responding to Israel’s genocide of Palestine?

No, the story is about Sudan.

It seems the Kremlin and Russian media are under the same Israeli control as Trump and the American media.

Recently, I wrote that Trump and Putin were the two people who counted, but it seems both are nothing but Israeli puppets. Putin even sold out Syria to Netanyahu.

-

Site: LES FEMMES - THE TRUTH

-

Site: The Orthosphere

Patriactionary has posted an amusing collection of postmodern Christian action figures. I’ve copied one below as a teaser, but you should go to Patriactionary to see the whole set. Be warned, more than one ox is gored.

-

Site: Mises InstituteWithin a libertarian society, people are free to act as long as they follow a principle of non-aggression. But can a libertarian society adopt an idea of the common good? In his Friday Philosophy, David Gordon tackles that question.

-

Site: Real Investment Advice

The S&P 500 surged 8.5% off its lows on Wednesday as the administration announced a 90-day tariff pause for all countries except China. Sound familiar? In Tuesday's Commentary, we wrote:

For those of you with bearish nightmares, we share one important takeaway from Monday’s market roller coaster. While there is a good chance the market may explore new lows over the coming months, we must appreciate that there is plenty of fuel for a sizeable bounce. The one piece of important evidence supporting this thesis was a Tweet claiming that Trump is considering a 90-day pause in all tariffs except those on China.

After the official announcement of the 90-day pause, the "fuel" propelled the market to its third-largest percentage gain in history. The two instances ahead of it both occurred in October 2008. The takeaway is that news about retalitory tariffs, pausing the tariffs, and any tariff agreements will continue to drive markets with extreme volatility. If Trump can turn the 90-day pause period into a series of constructive agreements with our largest trade partners, there is more bullish fuel in the tank. Negotiations with China will be most important. Retaliatory tariffs from China and then America have weighed on markets. The longer negotiations take, especially with China, the more negative consumer and investor sentiment will negatively impact the economy and markets.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we discussed the market reaction to the 90-day pause in tariffs, which sent the stocks surging in the third-largest single-day rally since WWII. As we stated yesterday:

"With the weekly “sell signal” in place, we will very likely see the market either stall at those levels (best case scenario) or retrace to test recent lows (most likely case.). Let’s see if we can get some follow-through on today’s trading.

Unfortunately, the market did not get a follow-through to yesterday's buying, and it was a classic bear market rally. As discussed on SimpleVisor yesterday morning, we took action and used the rally to rebalance portfolio and reduce exposure to equity risk.

"As we have discussed over the last two weeks, the deep oversold condition of the market would lead to a sharp reflexive rally that should be sold into to reduce risk and rebalance portfolios. That rally came yesterday, and we are reducing risk across all models this morning. The first step is to reduce exposure to positions, reduce target weights, and increase cash levels. The next step, if needed, will be to add a short position in portfolios. Today is step one."

We increased cash levels to nearly 20% in the 60/40 portfolio and dropped equity exposure to 49%. With the weekly sell signal in place, we will look to reduce equity risk by another 4-5% by adding a short position to the portfolio on the next rally.

Despite inflation dropping sharply and the 10 and 30-year bond auctions going well, the risk in the bond market is spreading through the equity markets. For more information on the "basis trade" and why it is such a risk, here is an excerpt from the Real Investment Show on Wednesday.

The market remains oversold in the near term, which should provide some opportunity for reflexive bounces to reduce risk and rebalance as needed. I suspect that the larger corrective process remains well intact, and an eventual retest of lows, if not new lows, is likely before this process is complete.

Trade accordingly.

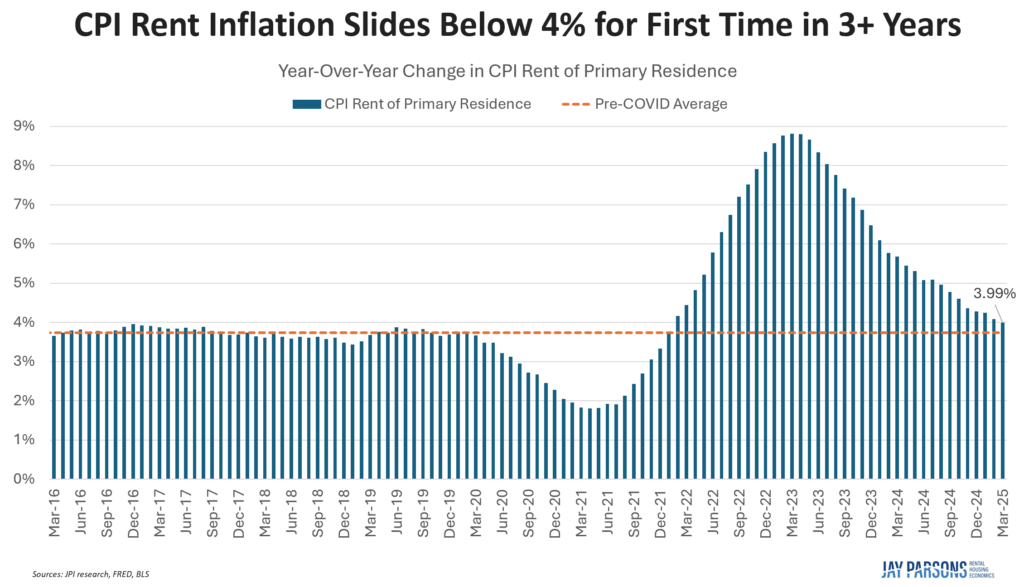

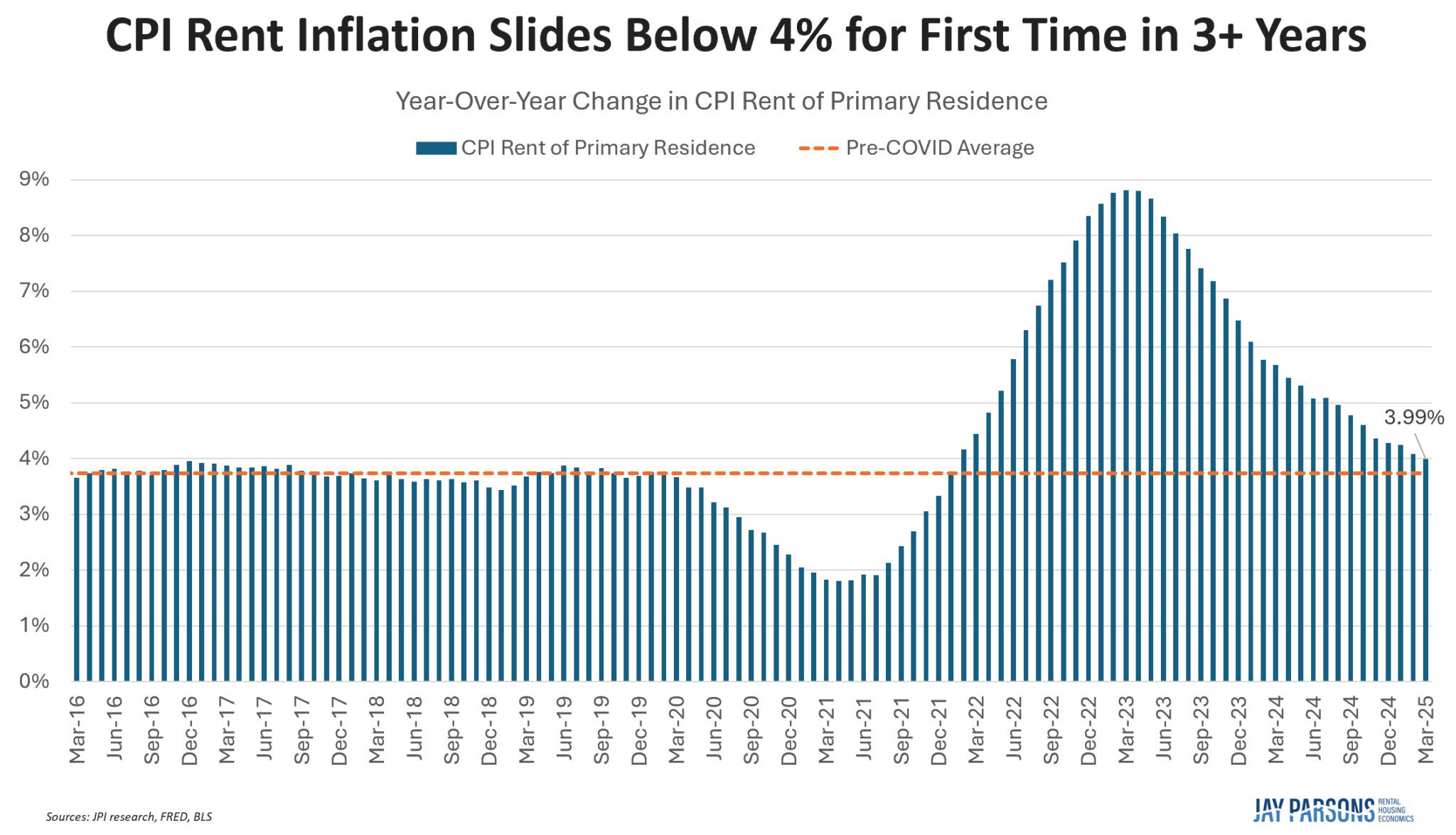

CPI Surprises To The Downside

The CPI (-.1%) and Core CPI (+.1%) came in 0.2% below expectations. Year over year Core CPI (+2.8%), the Fed's preferred inflation measure, is below 3% for the first time since March 2021. Also important, the so-called super core CPI fell by 0.24%, the lowest reading since May 2020. Supercore is the core calculation but also excludes housing.

CPI rent inflation, as shown below, continues to decline steadily. It now sits a hair below 4%. More disinflation in rents and shelter prices will continue, but the pace may slow from here.

While the data is very good, the initial impact of tariffs has yet to be felt. Inflation data could become volatile in the coming months as the tariffs' inflationary and deflationary effects ripple through the economy.

How To Use Tax Harvesting

For investors looking to reduce tax liability while keeping their portfolios optimized for growth, a tax-loss harvesting strategy can be a valuable tool. By strategically selling underperforming investments to offset capital gains, investors can minimize their tax burden and improve their after-tax returns.

Understanding how tax-loss harvesting works, when to apply it, and how it fits within a broader tax-efficient investing strategy can help investors make smarter decisions and maximize their wealth over time.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post The Pause Heard Around The World appeared first on RIA.

-

Site: Real Investment Advice

The recent implementation of tariffs has the media buzzing about increased recession odds as the consumer faces potentially higher costs. While recent economic reports, like the latest employment report, still show robust growth, those data points run with a lag that hasn't yet caught up with reality.

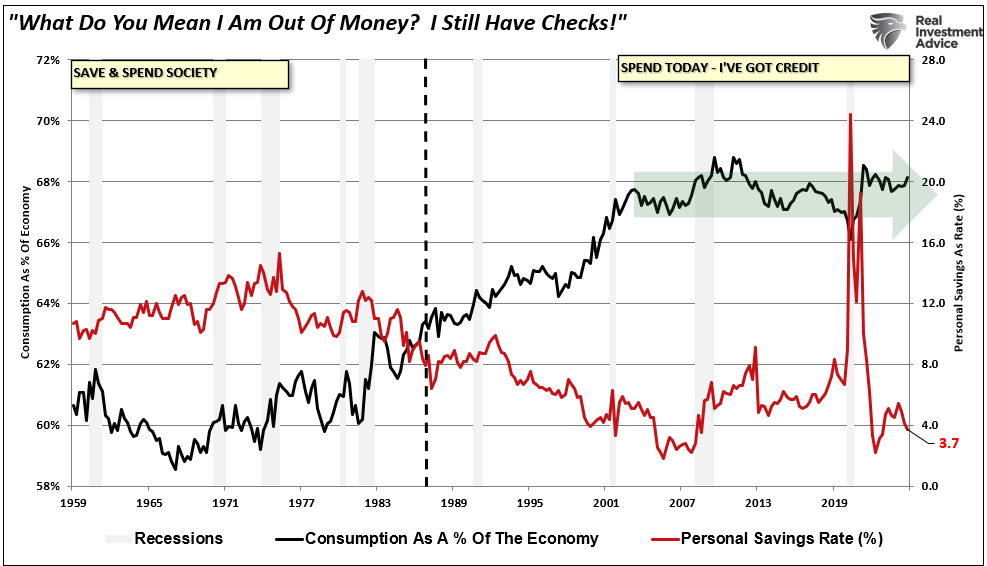

As we have discussed, the American consumer is the backbone of the U.S. economy and comprises nearly 70% of the GDP calculation. While GDP surged following the economic shutdown due to the massive flood of stimulus that fueled a savings surge, consumption as a percent of the economy has remained flat since the turn of the century. The reason is that despite the surge in savings, the consumer was also faced with rising inflation, which left them struggling to make ends meet.

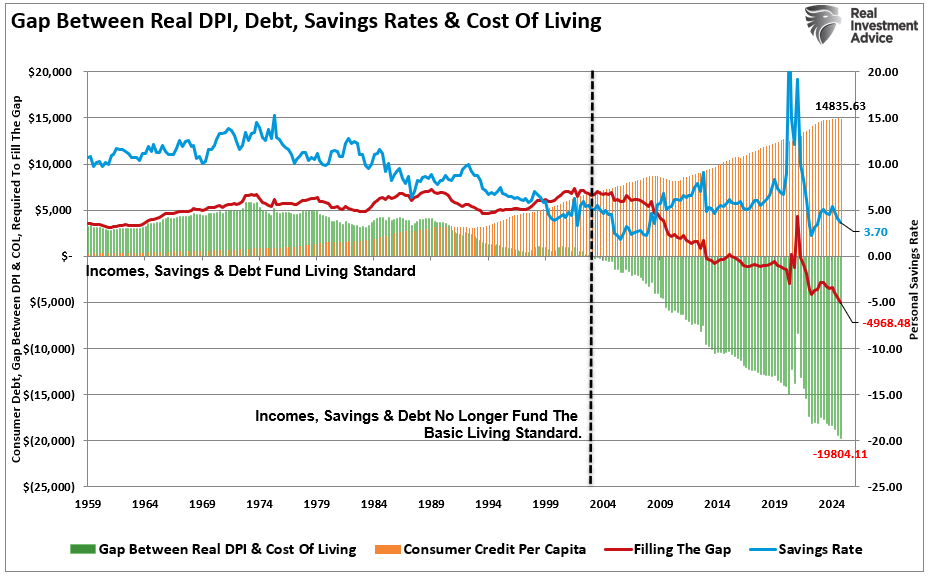

This dilemma is better illustrated by the chart below. The blue line is the personal savings rate, and the red line shows the debt needed annually to bridge the gap between the inflation-adjusted cost of living and savings and incomes. As shown, at the turn of the century, the consumer was no longer able to fund their living standard through just income and savings. The fact that consumers were forced to take on increasing debt levels to maintain their living standards explains why consumption as a percent of GDP has remained stagnant over the same period.

At the heart of the problem is the collapse of household balance sheets in the lower-income and middle-income brackets. These groups have depleted the excess savings accumulated during the pandemic and are turning to high-interest borrowing to bridge the gap. The Philadelphia Federal Reserve reported that the share of active credit card accounts making only minimum payments surged to 10.75% in Q3 2024—a record high. This statistic isn’t just a warning about credit health; it points to widespread cash flow stress.

In addition, more consumers are falling behind on their monthly card payments. The balance-based 30+ days past due rate increased 33 basis points year-over-year to 3.52% in the third quarter of 2024. This represents more than double the delinquency rate of 1.57 percent at the pandemic low in the second quarter of 2021.

More alarming is the growing use of Buy Now, Pay Later (BNPL) services. Notably, those services are not being used for large discretionary purchases but for food.

Recent surveys show that more consumers are increasingly relying on installment payment platforms like Klarna and Affirm to afford meals. Initially, the design of the BNPL model was for luxury or semi-durable goods. However, its expansion into groceries signals deep-rooted affordability issues. Debt is no longer just a tool for convenience; it's a necessity for millions' survival.

The problem with Trump's trade war now is that it comes when consumers are already showing clear signs of distress. According to recent data, both from the Federal Reserve and corporate earnings reports, the consumer's financial cushion that kept consumer spending alive in 2021 and 2022 is gone. What remains is a fragile consumer base increasingly reliant on credit and debt to afford necessities. While inflation has slowed, its damage is lingering. Now there is growing evidence suggesting that a recession and deflation are more immediate risks.

Consumer Confidence Declining

Consumer stress isn’t limited to anecdotal indicators—it’s now showing up in corporate earnings and executive commentary. During the company's earnings call, Doug McMillon, CEO of Walmart, stated that many customers are under “budget pressure.” They are also exhibiting “stressed behaviors,” including spending reductions across general merchandise. Specifically, he warned that “For many customers, the money runs out before the month does.”

Similarly, Dollar General CEO Todd Vasos painted an equally concerning picture. He described his customers as “struggling more than ever before.” Todd added that some are now forgoing non-discretionary items, like medication or hygiene products, to afford groceries and fuel. He said, “These customers are making trade-offs we haven’t seen in years.” Concurring with that warning was Jane Fraser, CEO of Citigroup. She observed that consumers are “becoming more cautious” and focusing spending on smaller, lower-cost purchases. While this signals a growing defensive posture, often associated with recessionary conditions, they are also deflationary. When consumer behavior shifts en masse from aspirational to survival-based, the ripple effects are inevitable.

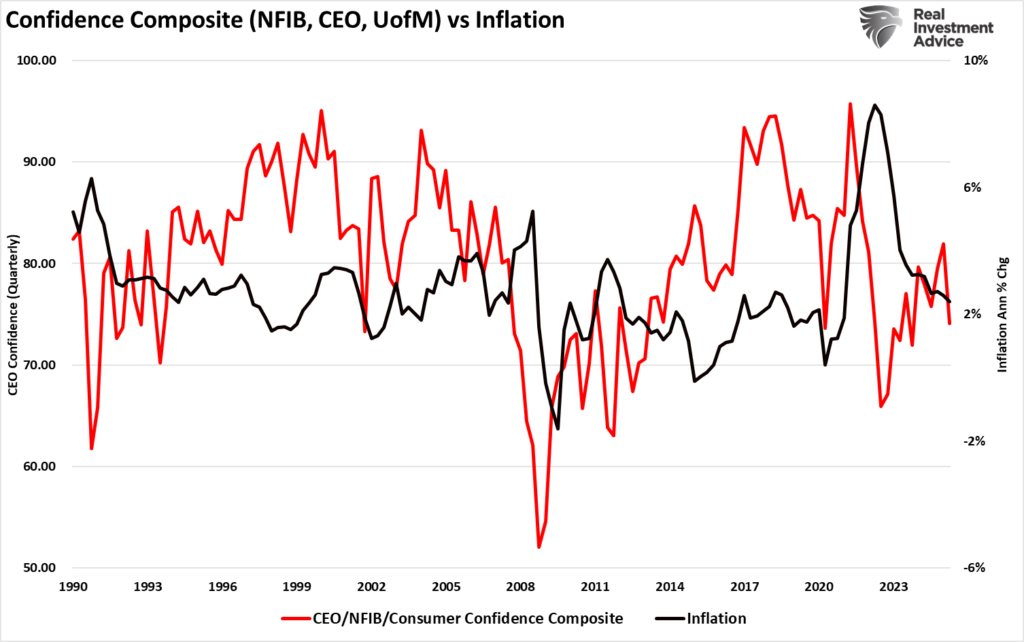

When we combine all the various measures of confidence into a single index, the correlation to GDP is unsurprising.

Furthermore, that decline in confidence leads to changes in the rate of inflation. This should be unsurprising since prices reflect supply and demand. As demand declines, prices fall to levels where demand for those products, goods, or services exists.

The data supports this narrative. Real personal consumption expenditures, the most significant component of GDP, are weakening. Once optimistic, the Atlanta Fed’s GDPNow model has revised estimates lower. Such was due to the decline in spending on goods and services. High interest rates, implemented by the Federal Reserve to curb inflation, now exert a secondary effect. Those rates are strangling credit access and making existing debt more expensive.

Housing data also reflects economic strain. Residential building permits and starts have declined markedly over the past six months, and homebuilder confidence has also deteriorated. First-time homebuyers—often a leading indicator of broader consumer strength—have retreated sharply due to affordability concerns.

When combined with increased pressures from higher taxes (read tariffs), the data is sending a warning.

The Risk Of Recession (and Deflation) Have Increased Markedly

The current data point toward a recessionary risk. Deflation is highly correlated to economic growth rates, wages, and rates. Unsurprisingly, recessions reduce inflation as demand for goods and services collapses. While inflation may be "sticky," the recent decline in bond yields and wages suggests consumer demand will decline this year.

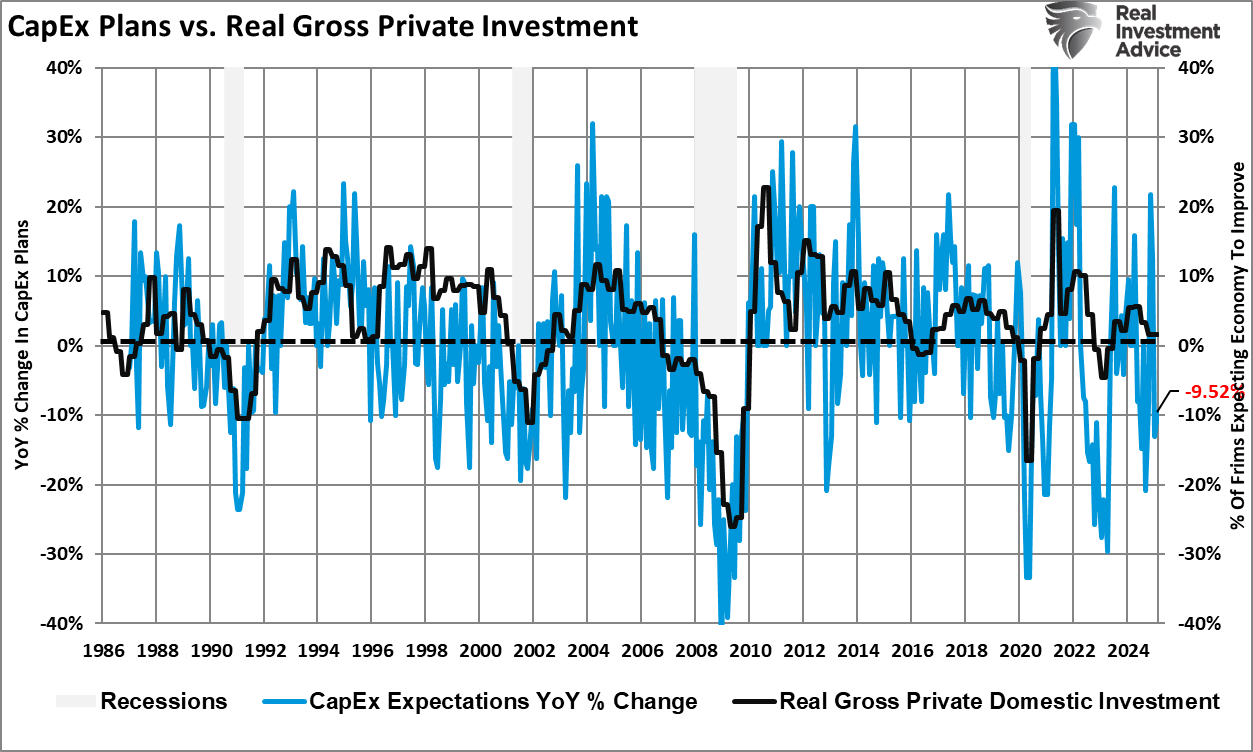

When tariffs, an additional tax on consumers, increase the cost burden, the reaction historically is not expansionary. As consumers contract spending, employers reduce business investment (demand) and cut employment (supply of wages). As shown, while volatile, plans to expend capital for investment purposes correlate with real private investment (which feeds into GDP.) While this data does not currently reflect the tariff impact, it was already suggesting much weaker growth. We suspect the outlook for CapEx has declined markedly in recent weeks.

We are seeing "demand destruction" caused by rising input costs due to tariffs against an already weak consumer backdrop. That combination of inputs will likely lead to higher unemployment, slower growth, and deflationary pressures in the economy unless there is a supply shock due to some unforeseen event like another "oil embargo." Outside of such an event, in an environment where consumer demand is falling due to the inability to afford what’s available, suppliers will have to cut prices to find buyers.

Furthermore, credit conditions also reinforce the recession risk. Banks have tightened lending standards across consumer and commercial lines as credit card delinquencies have ticked up sharply, particularly among borrowers aged 18–39. The Federal Reserve's Senior Loan Officer Opinion Survey shows a continued reduction in credit availability—making it even harder for stretched consumers to borrow their way through.

This reflects a critical turning point: the U.S. consumer is no longer a driver of economic growth but a potential drag on it. When nearly 70% of GDP depends on consumption, a weakening consumer poses systemic risks. A policy pivot may be necessary, and the calls for further Fed rate cuts this year are rising, with markets expecting four rate cuts this year. However, for now, with inflation still above target and the labor market gradually cooling, policymakers lack the room to cut rates aggressively without potentially reigniting price pressures. However, as the impact of tariffs causes a marked reduction in demand, those fears will likely give way to concerns about economic disruption.

In short, the American consumer is tapped out. The savings buffer is gone, wage growth is declining, and credit costs are rising. Corporate America is already adjusting to this new reality, with companies issuing cautious guidance for 2025. Even the tech sector—previously resilient—is showing signs of demand compression in consumer-facing verticals.

Unless wage growth accelerates or interest rates decline meaningfully, the pressure on households will continue to mount. That means recession and, ultimately, deflation—the more immediate threat to the U.S. economy. While deflation may seem the "out of consensus" view - if demand destruction continues unchecked, the more pressing concern is a downturn in demand. Declining real incomes and credit exhaustion are already warning of that risk.

Investors and policymakers would do well to focus less on inflation in isolation and more on the consumer’s deteriorating balance sheet. That’s where the next economic shock is currently hiding.

For more in-depth analysis and actionable investment strategies, visit RealInvestmentAdvice.com. Stay ahead of the markets with expert insights tailored to help you achieve your financial goals.

The post The Consumer Is Tapping Out appeared first on RIA.

-

Site: Mises InstituteMises said, “The continued existence of society depends upon private property.” Private property is essential for exchange, economic calculation, and many more pillars of human civilization.

-

Site: Mises InstituteFrom Paul Ehrlich to Bill Gates, prominent Americans have forecast doom through “overpopulation.” Although the Great Population Disaster has never occurred, that does not discourage the usual suspects from crying wolf.

-

Site: Public Discourse

As Catholic philosophers and fellow disciples of St. Thomas Aquinas, I would guess that Ed Feser and I are on the same page about many things. Even in his recent take on Catholic teaching on immigration, there is one point on which we are wholly in agreement: namely, that in evaluating policy decisions about immigration and immigration enforcement, we must consider “the entirety of Church teaching” on the subject.

Taken in its entirety, however, the Church’s teaching does not weigh, as Feser suggests, in favor of the Trump administration’s “restrictive immigration policy.” That claim is made to seem plausible only because Feser presents critics of the administration’s policies as consisting exclusively of “advocates of virtually open borders.” In reality, the very Church documents that Feser cites illustrate how it is possible both to criticize specific immoral forms of regulation and enforcement and defend moral forms of regulation and enforcement. Indeed, the whole point of Church teaching on immigration is to enable Catholics to assess whether specific policies are moral or immoral.

Feser’s essay does not properly reflect how this assessment works, however, because it misunderstands the role of prudence in applying moral principles.

Feser’s Relativistic Portrayal of Prudence

There is a puzzling disconnect between the beginning and end of Feser’s essay. Titled “A Catholic Defense of Enforcing Immigration Laws,” it opens by taking the position that “the administration’s restrictive immigration policy” is “on much stronger ground” vis-à-vis Catholic social teaching than the alternative that he presents as “virtually open borders.” He then identifies relevant principles from Church documents for the administration’s defenders to embrace: First, that the government ought to regulate immigration; second, that in doing so, it should consider immigrants’ potential impact on the well-being of its citizens, including with respect to employment, overall development, and cultural heritage.

(I should pause to note that this second point does not quite align with what the cited documents actually say. The point of section 2241 of the Catechism of the Catholic Church, about respecting cultural heritage, is phrased in terms of the immigrant’s duties to the host, rather than as something governments should consider in admitting immigrants. The 1988 document Church and Racism introduces “[a country’s] possibilities for employment and perspectives for development” as criteria that justify more limited intake. As the reference to development illustrates, however, this passage is evidently meant to justify a proportionately more limited responsibility for poorer countries in the developing world. Moreover, it takes a more open-ended perspective on the good of society as including that of the potentially admitted refugees, rather than being a one-sided consideration of the “economic well-being of its own citizens” as Feser suggests. Feser takes this same text to justify considering “preserving cultural identity” as a reason for restriction. In reality, what the text actually says is that governments should avoid creating “serious social imbalances” that would impel the home population to reject newcomers due to the perception that their identity and culture are threatened. The Church’s concern, again, is for the good of the newcomers taken together with the preexisting population. I set these observations aside for the sake of argument, though, and simply address matters the way Feser presents them.)

Now none of this yet makes a case for the essay’s opening position—everything is still too abstract. In the concluding paragraph, however, Feser seems to think that the existence of these principles already settles the question in his favor:

It would be intellectually dishonest, and indeed contrary to justice and charity, to accuse Catholics who appeal to such considerations in defense of enforcing U.S. immigration laws of somehow dissenting from the Church’s teaching. The truth is that the entirety of that teaching—not only what it says about the obligation to welcome the stranger, but also what it says about the limitations on that obligation—must inform our judgments about how many migrants to allow in and under what conditions.

After presenting this position as objectively preferable in light of Catholic teaching, though, he veers into surprisingly relativistic territory:

And as Aquinas teaches, here “it is not possible to decide, by any general rule” but requires the exercise of the virtue of prudence. As to what prudence calls for, Catholics of good will can reasonably disagree. Those who demand mercy toward immigrants should afford the same courtesy to their fellow Catholics who simply express a legitimate difference of opinion about a matter of public policy.

Two moves occur in this paragraph. First, although Feser is right to emphasize the need for prudence, he relies on an essentially relativistic notion of prudence—one in which objective moral principles only get us so far, and the rest of the work is done by prudential judgment in a personal realm of mere “difference of opinion,” shielded from objective moral scrutiny. Indeed, the phrase “legitimate difference of opinion about a matter of public policy” places public policy outside the realm of things one can objectively morally evaluate—a view commonly found in company with relativistic notions of prudence, as I have argued elsewhere.

I am not sure why Feser makes this move. It seems at odds with his judgment that Catholic social teaching positively favors “the administration’s restrictive immigration policy.” What makes such a judgment “legitimate”? If it is because the judgment correctly reflects the action’s objective moral status, then Catholics cannot reasonably disagree. But if it is because one has the right to apply moral principles prudentially as one sees fit, then this can only be true if the action has no objective moral status or its true status is for some reason undiscoverable—and then one prudential judgment cannot be “more in line” with Church teaching than another.

Moral Considerations Are Not Moral Justifications

But there is a second problematic move as well. Feser is at his strongest when he reminds us that many considerations must inform moral analysis of immigration policy—considerations that his conclusion divides roughly into the good of the host society and the good of the immigrant. But the point is (or should be) that all those considerations should inform every moral judgment in this domain. Instead, the conclusion treats social good and welcoming the stranger as separable justifications for irreconcilably opposing moral judgments, one justifying “restrictive” policy and the other justifying “merciful” policy.

Why is this problematic? Here’s an analogy: In morally evaluating a medical treatment, many considerations are relevant, including expectation of success, the patient’s health and age, the procedure’s cost relative to family and community resources, the absolute wrongness of intentional killing or forgoing ordinary lifesaving means, etc. But the mere fact that age is a relevant factor does not mean that anyone can legitimately appeal to it to sufficiently justify a particular moral judgment. For instance, when my grandmother with Alzheimer’s starts refusing food, I cannot legitimately conclude, “She is old; therefore we can stop feeding her.” Or, if my task is to demolish old buildings, I must take possible outcomes into consideration: a vagrant who may be sleeping inside would be killed or seriously injured. But that does not mean that I am justified in refusing to demolish any buildings on the grounds that a vagrant might be inside. Obviously, instead I should look inside and see if there is a vagrant actually sleeping there or not.

In other words, an item’s being on a list of relevant factors does not automatically make it into a plausible moral justification in an actual case. Otherwise, I could simply pick the factors that give me the answer I want and ignore the others. Rather, through prudence, I need to identify which factor actually does morally determine the case—or, to use more Thomistic language, to identify which moral form “specifies” the particular act, making it right or wrong.

Consequently, different factors may morally determine different cases. But it is not true that different people may legitimately appeal to different factors to justify opposing judgments of the same case. The principle of noncontradiction applies just as much to moral judgments as to any others. And prudence is the light that illuminates an action’s moral status.

An Authentically Thomistic Account of Prudence

These two problems are symptoms of something gone awry in the underlying picture of moral reasoning in Feser’s essay, which I want to contrast with an authentically Thomistic view of prudence.

Consider: Feser cites Aquinas saying that “it is not possible to decide by any general rule” whether in a given situation I should aid a less needy family member versus a more needy stranger. Instead, one must decide by prudence. This can sound as though I must make my decision, not by considering a rule, but by something else: prudence.

But the English translation is misleading. What Aquinas actually says is that “a general rule cannot determine” which person I am obliged to aid in this situation, something that only prudence can do. The difference sounds innocent, but it is important.

What does Aquinas mean? Here are three important characteristics of Thomistic prudence.

First, Thomistic prudence is objective, not relativistic. For Aquinas, deliberately chosen actions are always objectively either good or evil. Prudence is the virtue for discerning that moral status. Disagreement is legitimate when prudence fails, not when prudence is operating normally. For instance, my options may be equally good and thus morally indistinguishable. Or poorly informed agents may reach different judgments where one or both are unwittingly wrong, but they disagree “legitimately” in the sense of both acting in good faith.

Second, prudence judges in accord with the moral law, not outside it. Prudential reasoning is supposed to identify the features defining a concrete action as good or evil, thus uncovering which moral law the action falls under. Aquinas’s point in the passage above is that there are many relevant rules that might govern aid: e.g., I should aid those nearer to me, and I should aid the needy, both as a general matter. But there is no overarching rule adjudicating between them—i.e., a rule that dictates “in cases of conflict, always prioritize proximity” or “always prioritize need.” Indeed, as Aquinas observes, need and proximity come in degrees, so one can’t know which will be morally defining without having a particular situation in mind.

Different situations, then, have different “features” that make them fall under different morally defining rules. By examining an action in its particular circumstances, then, the prudent person can discover which rule objectively morally specifies it. In one situation I should prioritize, say, buying a thoughtful gift for my sister to strengthen family ties. In another, I should prioritize, say, buying food to stock the kitchen of a newly arrived refugee to alleviate her hunger and loneliness. (Incidentally, that’s why Aquinas’s ordo amoris isn’t a priority rubric or moral triage principle for allocating aid. Rather, it is one moral principle among many others, and prudence’s task is to detect whether a given action falls under this principle or a different one.)

Third, Thomistic prudence relates principles to particular actions. The reason Feser can make the choice between “restrictive” versus “merciful” policy seem legitimately open is that it remains so abstract. No morally defining features have yet come into view. One cannot morally evaluate “health care procedures” any more than one can morally evaluate “immigration policy” or “enforcing laws” in the abstract. What can be analyzed is a specific law or policy or enforcement activity—e.g., the six-month waiting period for work permits for asylum seekers, or ending refugee admissions in the U.S. in 2025, or the policy of ceasing to consider humanitarian impact when determining whom to deport, or the specific actions that agents of the state take to enforce a law or policy. These are not morally neutral, and the virtue of prudence should enable us to detect their true moral status.

Thomistic Reasoning on Immigration

With this picture of Thomistic prudence in mind, let us now examine how one might exercise moral reasoning on questions pertaining to immigration policy and enforcement. Since there is no room here for full-fledged analysis of any of these actions, I will instead examine how the considerations Feser identifies intersect with the particular circumstances of America in 2025.