For many people today, practical atheism is the normal rule of life...If this attitude becomes a general existential position, then freedom no longer has any standards, then everyting is possible and permissible.

Distinction Matter - Subscribed Feeds

-

Site: Zero HedgeWill Nuclear Fusion Soon Be The "Norm?"Tyler Durden Fri, 05/16/2025 - 19:05

Authored by Duggan Flanakin via RealClearEnergy,

The dream of humanity to imitate the forces that created their habitat has been alive for at least as far back as the time when humans with a single language decided to build a city with a tower that reached the heavens. For such a people, “nothing they plan will be impossible to them,” it is recorded.

For at least the same time frame, humanity has sought comfort through technology. While primitive heat producers like coal and wood are still used today, the discovery that petroleum, natural gas, and even moving water could generate a newly discovered phenomenon known as “electricity” transformed the industrial revolution into the modern era.

Not until the 1930s did German scientists build on Enrico Fermi’s discovery that neutrons could split atoms to recognize that splitting atoms would release significant energy – energy that could be used for both bombs and electricity generation. By the 1950s, scientists began building nuclear fission-based power plants that today provide about a tenth of the world’s electricity.

Scientists and engineers also began to envision the potential of nuclear fusion -- the reaction of light atomic nuclei powers the sun and the stars. Since that time, they have worked feverishly, but with little success, to replicate this energy-rich reaction using deuterium and tritium.

One group of scientists and engineers decided to try an alternative approach.

Founded in 1998, California-based TAE Technologies has been developing a reactor that runs on proton-boron aneutronic fusion – that is, a fusion reaction that fuses a hydrogen nucleus with non-radioactive boron-11 instead of fusing hydrogen isotopes of deuterium and tritium. Their goal is to develop commercial fusion power with the cleanest-possible environmental profile.

All efforts at fusion require chambers that can withstand temperatures of millions of degrees Celsius and immense pressure that are needed to fuse two isotopes together. To accomplish this requires huge amounts of energy – and until recently, more energy than the fusion produced.

Most fusion researchers, including those building the ITER project being built in France, rely on a donut-shaped tokamak reactor chamber, in which a stream of plasma must be held away from its walls by electromagnets for any energy to be produced. The tokamak design uses a toroidal magnetic field to contain the hydrogen plasma and keep it hot enough to ignite fusion.

Sadly, as with ITER, project costs have soared and timeframes have fallen by the wayside despite occasional breakthroughs. Over decades, tokamak designs became gigantic, with huge superconducting magnetic coils to generate containment fields; they also had huge, complex electromagnetic heating systems.

Spurred by the failures of wind and solar to fully satisfy the desire for “clean energy,” governments and private investors began investing heavily into fission and fusion projects. Oak Ridge, Tennessee, has tapped into a $60 million state fund intended to bolster both fission and fusion energy in atomic energy’s American birthplace.

New research at the University of Texas, in conjunction with Los Alamos National Laboratory and Type One Energy Group, uses symmetry theory to help engineers design magnetic confinement systems to reduce plasma leakage from tokamak magnetic fields.

The old method used for a stellarator reactor relied on perturbation theory. The new method, which relies on symmetry theory, is a game changer. It can also be used to identify holes in the tokamak magnetic field through which runaway electrons push through their surrounding walls and greatly reduce energy output.

The TAE Technology reactor is entirely different than any of the tokamak or stellarator fusion chambers. In 2017, the company introduced its fifth-generation reactor, named Norman, which was designed to keep plasma stable at 30 million C. Five years later the machine had proven capable of sustaining stable plasma at more than 75 million C.

That success enabled TAE to secure sufficient funding for its sixth-generation Copernicus reactor and to envision the birth of its commercial-ready Da Vinci reactor. But in between, TAE developed Norm.

Norm uses a different type of fusion reaction and a new reactor design that exclusively produces plasma using neutral beam injections. The TAE design dumps the toroidal field in favor of a linear magnetic field that is based on the “field-reversed configuration” (FRC) principle, a simpler, more efficient way to build a commercial reactor.

Instead of massive magnetic coils, FRC makes the plasma produce its own magnetic containment field. The process involves accelerating high-energy hydrogen ions and giving them a neutral charge, then injecting them as a beam into the plasma. That causes the beams to be re-ionized as the collision energy heats the plasma to set up internal toroidal currents.

Norm’s neutral beam injection system has cut the size, complexity, and cost, compared to that of Norman, by up to 50%. But not only is an FRC reactor smaller and less expensive to manufacture and operate, says TAE, it can also produce up to 100 times more fusion power output than a tokamak -- based on the same magnetic field strength and plasma volume.

The FRC reactor also can run on proton-boron aneutronic fusion, which, instead of producing a neutron it produces three alpha particles plus a lot of energy. The fewer neutrons also do less damage to the reactor; the energy being released as charged particles is easier to harness. Less shielding is required, and, perhaps best of all, boron-11 is relatively abundant and not radioactive.

So, while “Norm” may not be the final step in developing commercial fusion energy, TAE’s hope is that fusion energy will the “norm” as early as the mid-1930s. FRC technology has materially de-risked Copernicus, according to TAE CEO Michi Binderbauer.

If Norm is as advertised, it will accelerate the pathway to commercial hydrogen-boron fusion – a safe, clean, and virtually limitless energy source.

But is humanity ready for free energy to be the “norm?”

Duggan Flanakin is a senior policy analyst at the Committee For A Constructive Tomorrow who writes on a wide variety of public policy issues.

-

Site: Zero HedgeTrump Fumes After Supreme Court Rules Venezuelan Illegals Can't Be Deported (For Now)Tyler Durden Fri, 05/16/2025 - 18:51

Update (1715ET): President Trump took to TruthSocial to issue his brief but terse statement:

"THE SUPREME COURT WON’T ALLOW US TO GET CRIMINALS OUT OF OUR COUNTRY!"

* * *

The Supreme Court ruled this afternoon to keep in place its block on President Trump's deportations of (alleged) Venezuelan gang members under a 1798 law historically used only in wartime after their ACLU lawyers said the government was set to remove the men without judicial review in violation of a prior order by the justices.

The Supreme Court has previously issued two orders stemming from those cases.

Justices agreed that the president could rely on the centuries-old wartime law to remove immigrants from the country - provided they first have an opportunity to challenge those claims in court - and then temporarily blocked the government from deporting another group of Venezuelans in Texas while their lawyers scrambled to challenge the allegations against them.

In his proclamation invoking the Alien Enemies Act, Trump stated that “all Venezuelan citizens 14 years of age or older who are members of [Tren de Aragua], are within the United States, and are not actually naturalized or lawful permanent residents of the United States are liable to be apprehended, restrained, secured, and removed as Alien Enemies.”

The 7-2 decision clarified an unusual order issued by the justices in the early hours of April 19 that hit pause on any government plans to deport people held in northern Texas.

The Supreme Court delivered a blow to the Trump Administration in blocking deportations under the Alien Enemies Act. However, the Court only did so based on the lack of notice (24 hours) afforded by the Administration. It did not rule on the legality of the use of the AEA...

— Jonathan Turley (@JonathanTurley) May 16, 2025Over the dissents of conservative Justices Clarence Thomas and Samuel Alito, the justices in the latest unsigned decision slammed the Trump admin for only giving the detainees 24 hours to launch legal challenges.

“Notice roughly 24 hours before removal, devoid of information about how to exercise due process rights to contest that removal, surely does not pass muster,” the court wrote in its unsigned opinion.

“But it is not optimal for this Court, far removed from the circumstances on the ground, to determine in the first instance the precise process necessary to satisfy the Constitution in this case. We remand the case to the Fifth Circuit for that purpose,” the opinion continued.

However, as The Hill reports, the justices declined the ACLU’s additional request to leapfrog the lower courts to immediately take up the issue of whether President Trump can invoke the rarely used law outside of wartime.

Instead, the case will return to the lower courts alongside a handful of other challenges being brought by the civil rights group around the country.

So it’s legal for a president to ship millions of illegal aliens into our country but it’s illegal to send them home?

— Rep. Mike Collins (@RepMikeCollins) May 16, 2025

The system is broken. The Supreme Court failed us.

Whose country is this anymore?The issue could ultimately return to the justices, who directed the lower courts to act “expeditiously.”

Now, we all anxiously await President Trump's response to this decision...

-

Site: Zero HedgeBees Are Behind Our Food And Natural Medicines - And They're DisappearingTyler Durden Fri, 05/16/2025 - 18:40

Authored by Emma Suttie via The Epoch Times (emphasis ours),

Bees are dying—and at an alarming rate.

Between 2023 and 2024, US beekeepers lost an estimated 55.1 percent of their colonies—the worst loss in more than a decade and nearly 15 percent higher than the previous 13-year average.

Lisa Schaetzle/Getty Images

Lisa Schaetzle/Getty Images

Bees pollinate three-quarters of the fruits, vegetables, and nuts we eat, and many of us rely on bee products for their nutrition and health-promoting gifts. If bees vanish, it’s scary to think of all we stand to lose. And some say that if the bees go, we go too.

Jeff Pettis, president of Apimondia—The International Federation of Beekeepers’ Associations—sums up the health benefits that bees offer humans in one word: huge.

Although two-thirds of our diet comes from carbohydrates—crops like rice, wheat, and corn—which are pollinated by wind rather than insects, many other important foods require bees.

“So we’re not going to starve if we don’t have bees. But literally, everything you can think of that’s nutritious—fruits, nuts, and vegetables—all of those are, we'll call it, animal-pollinated. The vast majority of those are pollinated by honey bees or other wild bees,” he told The Epoch Times.

Bees Pollinate

Ryan Burris is a third-generation beekeeper and the president of the California State Beekeepers Association. He points out that many people don’t realize how many fruits and vegetables we eat depend on bees for pollination.

“The biggest one, obviously, for beekeepers, is almonds. And then you have things like blueberries, watermelons, and stuff you don’t think about, like onions and carrots—all require pollination. There’s an estimated 100 crops that require pollination,” he told the Epoch Times.

Twenty thousand species of bees grace our planet, and 4000 species are native to the United States. Bees are some of our most well-known and beloved pollinators. One in every three bites of food you eat depends on pollinators to produce, and bees pollinate one in every four bites.

Beyond their critical role as pollinators, bees also gift us powerful products like honey, bee pollen, propolis, and royal jelly—each packed with nutritional and medicinal benefits.

Honey

The Ancient Egyptians may have been the world’s first beekeepers. They crafted clay hives and transported them on rafts along the Nile, allowing bees to pollinate whatever flowers were in season. Bees were deeply revered, and honey was considered sacred.

Throughout history, honey has played many roles—it was used in religious rituals, medicine, currency, and offerings to the gods. When archaeologists uncovered King Tutankhamun’s tomb, they found a sealed jar of honey more than 2,000 years old. Because honey doesn’t spoil, it was still safe to eat.

Honey offers a treasure trove of healing properties. It soothes a cough, benefits digestion and oral health, treats constipation and diarrhea, protects the heart, and has anticancer properties—in addition to being antibacterial, anti-inflammatory, antifungal, and a powerful antioxidant.

Jana Schmidt is a board-certified naturopathic doctor and master herbalist who keeps bees. She says not all honey is created equal, and knowing where your honey comes from is crucial, as many store-bought varieties are synthetically made or artificial. If you want the good stuff, go for raw, local honey—ideally straight from a beekeeper.

“Darker varieties have higher antioxidants than the lighter varieties,” she noted, saying bees make the darker types in the winter months when it’s cold, and they need more nutrition—which is passed to us when we eat it.

She says that honey added to tea before bed can help you sleep—something she did for her children when they were little.

“It helps regulate your sleep, but it also protects the teeth from the bacteria that causes cavities, which seems crazy because it’s sweet. You think, oh, that’s going to cause cavities, but actually, it protects the teeth,” she told The Epoch Times.

Studies have found that honey’s antibacterial properties fight harmful bacteria, such as Salmonella and E. coli. In addition, honey has been studied for its potential benefits against cancer—including breast, liver, and colorectal cancers, where it has shown cytotoxic effects on cancer cells, the ability to inhibit cancer cell growth, and prevent the formation of new blood vessels that tumors need to grow.

Raw honey is a potential source of Clostridium botulinum spores, which can cause botulism—especially in babies. Therefore, it’s generally recommended that infants under one year of age should not be fed raw honey.

Bees are prolific producers of a diverse array of products with numerous potential health benefits, according to experts.

Bee Pollen

Honeybees collect pollen from flowers and mix it with their saliva, which contains special enzymes. They then store it in comb cells inside their hives. Once the pollen is stored and processed in the hive, it is called beebread, or ambrosia—a vital food for the bees—containing proteins, fats, vitamins, and minerals they need. When beebread is stored, it undergoes a natural fermentation process, which preserves it and makes its nutrients easier to absorb.

Bee pollen. hanif66/Shutterstock

Bee pollen. hanif66/Shutterstock

“To me, it’s God’s perfect multivitamin because it has every vitamin and mineral known for human nutrition. It has approximately 96 different nutrients and bioavailable energy. It’s antibacterial, antifungal, antiviral, and the most digestible protein per ounce than anything else out there,” Schmidt said.

Bee pollen offers a source of sustained energy throughout the day and not a spike like you might get from sugar or caffeine, she said.

“I don’t drink coffee or anything like that. I just take my bee pollen in the morning, and I’m good to go,” she beamed.

There is growing scientific interest in bee pollen, particularly because of its antimicrobial properties, which can fight a wide variety of pathogens, including bacteria and fungi. This ability is notable because some bacteria are becoming resistant to antibiotics. Bee pollen (beebread) seems able to fight microbes without creating resistance, which some scientists believe is because it contains several different natural compounds that work synergistically. Bee pollen also supports the body’s good bacteria, benefiting healthy gut microbes—behaving like a prebiotic.

Schmidt adds that as a natural fertility specialist, bee pollen is her number one fertility supplement.

“If you think about it, it’s the fertility for the plants. Why wouldn’t it be fertility for us, too? So sometimes that’s all it takes. The couple start taking bee pollen, and bam, they’re fertile. So that’s been pretty fun to be a part of.”

Studies have found that bee pollen has other wide-ranging medicinal benefits to humans, including:

- Benefiting metabolic syndrome disorders

- Preventing obesity

- Combating liver disorders

- Cardioprotective effects

- Lowering uric acid

- Detoxifying (based on animal studies)

- Regulating ovarian functions

- Alleviating allergic reactions

- Improving digestion and absorption

- Stimulating the immune system

- Improving cognitive dysfunction

“It takes bees working eight hours a day, two to four weeks, to gather one teaspoon of pollen, Schmidt said. They work so hard. They visit over 2 million flowers to get one teaspoon of pollen. It’s pretty amazing.”

Propolis

Propolis, also known as “bee glue,” is a resinous substance bees gather from different types of plants. Bees use it as a type of construction material for the hive. It seals holes and cracks, improves structural integrity, smooths the inner surface of the hive, maintains a constant internal temperature of 95 degrees Fahrenheit, and protects the hive from the elements, predators, and pathogens. Once hardened, it helps create an antiseptic internal environment.

Bee propolis. Ihor Hvozdetskyi/Shutterstock

Bee propolis. Ihor Hvozdetskyi/Shutterstock

Schmidt offers a long list of propolis’s benefits, particularly to the brain. These include reducing inflammation in the brain and oxidative stress, helping reduce the toxic effects of methylmercury—a highly toxic form of mercury—and aluminum in the brain, increasing synaptic efficiency, and protecting against neurodegeneration and cognitive impairment.

She adds that it is a great prebiotic and excellent for gut health.

“Anytime there’s an infection, and you’re not quite sure what it is, I usually go to propolis—it just boosts your immune system like nothing else I’ve ever used,” she said.

Studies have revealed that this amazing substance has many applications for human health and has the following medicinal properties:

- Antioxidant

- Anti-inflammatory

- Antiulcer

- Anticancer

- Immunomodulatory

- Neuroprotective

- Anti-allergic

- Cardioprotective

- Antidiabetic

Studies in humans and animals have shown propolis to possess powerful healing properties beneficial in multiple acute and chronic diseases—from autoimmune diseases like Type 2 diabetes and rheumatoid arthritis to cardiovascular disease, cancer, and COVID-19.

In a 2021 randomized, controlled clinical trial, 124 hospitalized patients with COVID-19 were split into three groups. Two groups received Brazilian green propolis—400 or 800 milligrams daily—in addition to regular treatment—while the third group did not receive propolis.

The researchers found that patients who received propolis were released from the hospital five to six days sooner, and those who received 800 mg of daily propolis had less kidney damage associated with COVID-19. Thus, the study authors concluded that propolis is a safe and effective adjunct treatment for patients with COVID-19.

Royal Jelly

Humans have used royal jelly as a powerful medicine for millennia. It is extremely popular and highly regarded in Chinese medicine—in ancient times and today. Royal jelly is an overall tonic that promotes the robust development of bones, teeth, and the brain. It also helps boost fertility for women and soothe the symptoms of menopause.

Royal jelly. Bin Zhu/Shutterstock

Royal jelly. Bin Zhu/Shutterstock

Royal jelly is a white milky substance secreted by worker bees to feed the queen bee larvae. Worker bee larvae get a different type—called worker jelly that contains fewer nutrients. According to one study, the higher quality royal jelly fed to the queen allows her to live a long life (up to five years) and lay 2,500 eggs daily. In comparison, worker bees only live about 45 days and, although female, do not reproduce.

Rich in proteins, carbohydrates, fats, vitamins, and minerals, royal jelly is a vital food source for bees. Today, humans use it as a dietary supplement, medicine, and ingredient in cosmetic and skincare products.

Studies have shown royal jelly to have the following medicinal properties:

- Antioxidant

- Anti-lipidemic

- Antiproliferative

- Antimicrobial

- Neuroprotective

- Anti-inflammatory

- Immunomodulatory

- Antiaging

- Estrogenic activities

Despite its medicinal benefits, Schmidt says that she does not recommend royal jelly because of how it is harvested, as it hurts the bees and the hive only to collect a tiny amount.

“I just don’t like the practice overall ... I feel like it takes it a step beyond what we should be doing to live well with the bees,” she said.

A 2023 study investigated the effect of royal jelly on liver enzymes and glycemic indices. The researchers found that royal jelly did not significantly affect adults’ glycemic profile or liver function. However, in trials with a longer duration of 8 or more weeks, and those conducted in “non-healthy” populations, there was a significant reduction in serum fasting blood glucose —a measurement of glucose in the blood after fasting. Higher fasting blood glucose levels are a characteristic sign of both prediabetes and Type 2 diabetes.

Why Bees Are Dying

We have all heard about the alarming decline in bee numbers in recent years.

Pettis says the reasons that bees are dying is such huge numbers are multifaceted and complex.

The first, he says, is that bees are losing their natural habitat. A significant reason for this is the rise of monoculture—when farmers plant only one kind of crop in their fields. This lack of diversity limits the flowers available for bees, making it harder for them to get all the nutrients they need to stay healthy and thrive.

“Roundup Ready crops, like corn, soybeans, all these—they create very sterile fields so there are no weeds—and a lot of those weeds are really good for bees,” he said.

Pettis says the second reason is pesticide exposure and the third is pests and diseases affecting bees. He says they all combine in different ways to affect bees and reduce their numbers, making beekeeping more challenging.

“We’ve had a number of exotic things come into the U.S.—two parasitic mites, and then the beetle from Africa, and now we have some invasive hornets coming in from Asia. It’s just one thing after another,” he said.

“It’s really hard to survive when you have all these stressors lining up, one right behind the other.”

Some readers may be wondering about colony collapse disorder.

“I was actually very involved in colony collapse disorder, which is now 20 years old, and we never came up with a single definitive thing. It was just a combination of things that were killing managed honeybees,” Pettis said.

Mites, particularly the varroa mite—which is aptly named Varroa destructor—have become an enormous challenge for beekeepers.

“The varroa mite—Varroa destructor—is the main killer of honey bees because they feed on the bee as it’s growing,” Burris said.

These tiny parasitic mites feed on bee fat and blood, which bees need for energy and a healthy immune system. They also spread viruses, particularly the deformed wing virus, which causes bees to be born with shriveled wings that will never fly.

Burris adds that federal and state regulators do not want honeybees on public lands as they fear they may hurt native pollinators, though he notes they don’t have evidence to support those concerns.

He says they’re arguing about food supply and demand problems without considering that native pollinators and honey bees have different feeding habits.

“They’re not taking into account the size of the honeybee, the size of a native pollinator, the size of their tongues, and how they extract nectar—how they obtain pollen,” he said.

Pesticides, which include insecticides and herbicides, are also detrimental to bees.

“Roundup and other weed killers that contain glyphosate are incredibly harmful to our bodies, but also the bees,” Schmidt said.

A relatively recent class of insecticides called neonicotinoids, or neonics, are the world’s most widely used insecticides and possibly one of the most deadly. They work by making every part of the treated plant toxic while poisoning the soil, surrounding water, and wildlife. They affect the bees’ nervous system, interfering with their ability to learn, remember, and navigate, meaning many exposed bees can’t find their way back to the hive and eventually die.

Since their introduction in the last two decades, neonicotinoids’ widespread use has made U.S. agriculture increasingly destructive to insect life. Neonicotinoids are responsible for 92 percent of this increase in danger to insects.

These deadly insecticides don’t just kill bees. Neonics are linked to losses of birds and fish and birth defects in white-tailed deer. Increasing evidence has also shown that neonics affect human health, especially children. One study found neonics in the urine of half of children 3 to 5 years old, and a 2020 Swiss study found neonics in every sample of plasma and spinal fluid of children receiving treatment for leukemia and non-Hodgkin lymphoma.

How We Can Help Bees

Thankfully, there are things we can all do to help bees and support these essential pollinators.

- Plant native flowers and trees, especially ones that bloom through summer, as bees need food from spring through fall.

- Buy local honey, and honey made 100 percent in the United States to support U.S. beekeepers.

- Avoid using insecticides or pesticides around your yard and use natural methods instead. Schmidt says using vinegar and water with a bit of salt kills weeds without harming anything else.

- Allow an area of your yard or garden to be overgrown or less cut back to provide food and nesting habitats for bees.

- Plant a bee garden with native flowers to attract bees and other pollinators.

- Create a bee watering station with filtered water using a deep plate with pebbles or marbles near flowering plants to give bees a safe place to drink.

- Create a bee house you can hang in your yard to give bees a place to live.

- Keep hives away from sources of wifi radiation and EMFs, which adversely affect bees.

- If you notice a swarm of bees on your property, contact a local beekeeping association, university agriculture department, or local beekeeper to collect them, not an exterminator.

- Encourage state legislators to support laws that support and protect bees.

- Spread awareness about bees and how we can support them.

Schmidt reveres the tiny pollinators that provide us with so much.

“You know, we use the term beekeeping, but I really feel like they keep us—like they know what to do, we just need to provide a nice habitat for them, and they do all the work—they just give and give.”

-

Site: RT - News

The offensive, dubbed Gideon’s Chariots, reportedly aims to “conquer” the entire Palestinian enclave

The Israel Defense Forces (IDF) has announced a new bombing campaign in Gaza aimed at defeating Hamas. The offensive comes after a ceasefire brokered by the US, Egypt, and Qatar expired in March.

“Over the past day, the IDF launched extensive attacks and mobilized forces to seize strategic areas in the Gaza Strip, as part of the opening moves of Operation Gideon’s Chariots and the expansion of the campaign in Gaza,” the military said in a statement on Friday evening.

The IDF reiterated its goals of securing the release of the remaining hostages and achieving “the defeat of Hamas.”

“IDF troops in the Southern Command will continue to operate to protect Israeli citizens and realize the goals of the war,” the Israeli army added.

According to the Times of Israel, the IDF aims to “conquer” Gaza, relocate the Palestinian population to the southern part of the enclave, and prevent “terror groups” from seizing humanitarian aid.

Al Jazeera reports that at least 115 Palestinians have been killed since dawn on Friday.

במהלך היממה האחרונה צה"ל החל בתקיפות נרחבות והניע כוחות לתפיסת שטחים שולטים בשטח רצועת עזה, זאת כחלק ממהלכי הפתיחה למבצע "מרכבות גדעון" והרחבת המערכה בעזה, להשגת כל מטרות המלחמה בעזה, לרבות שחרור החטופים והכרעת החמאס.

— צבא ההגנה לישראל (@idfonline) May 16, 2025

כוחות צה"ל בפיקוד הדרום ימשיכו לפעול בכדי להגן על אזרחי ישראל… pic.twitter.com/WtK8Iy6XyGThe ceasefire between Israel and Hamas broke down in March after the sides failed to agree on implementing the second phase of the truce.

Israel declared war on Hamas following a surprise attack by Palestinian militants on October 7, 2023, which killed around 1,200 people and resulted in over 200 hostages being taken. More than 53,000 Palestinians have been killed since the conflict began, and human rights organizations have accused Israel of genocide.

-

Site: LifeNews

Pro-Life Americans were sorely disappointed today when a House committee voted down the reconciliation bill that has language to defund the Planned Parenthood abortion business.

But House Majority Leader Steve Scalise says he thinks the fiscal policy issues that prompted a handful of pro-life Republican lawmakers to defeat the bill will be resolved and the House will pass the bill next week.

Scalise explained how this one big, beautiful bill will go to the Budget Committee on Sunday night before heading to the Rules Committee, and then the House Floor.

“So Sunday night, the Budget Committee will go back in,” he said in an interview with Fox News. “They’re going to meet.”

SUPPORT LIFENEWS! If you want to help fight abortion, please donate to LifeNews.com!

“Look, we’re talking to those members who voted no today. We’re going to work through it. There were some questions they had for the Trump Administration. We were working on getting them some of those questions answered,” Scalise explained.

“We’re going to get the bill passed. Then, ultimately, by next week, Tuesday, Wednesday, Thursday, on the House Floor, that bill will pass,” he added.” One big, beautiful bill will pass the House, and then it goes to the Senate, and they get to start their process. Although we’ve been keeping Senator Thune, Senator Crapo, all the other members of their leadership informed every step of the way, so they know what’s in this bill. Hopefully, they won’t have to start over from scratch.”

“[It could pass the Budget Committee by] Sunday night. It goes to Rules [Committee], goes to the floor – Tuesday, Wednesday, Thursday, somewhere in there. As fast as we can get it done. Let’s get it done,” the pro-life congressman added.

The bill failed in this morning’s vote in a 16-21 vote, with Reps. Ralph Norman (R-SC), Chip Roy (R-TX), Josh Brecheen (R-OK), Andrew Clyde (R-GA), and Lloyd Smucker (R-PA) joining all Democrats in voting down the bill.

The House Energy and Commerce Committee signed off on the bill earlier this week.

The good news for pro-life Americans is that the measure includes language to defund Planned Parenthood and Big Abortion. The abortion giant just announced that it killed over 420,000 babies in aboritons in its most recent year and mamade over $2 billion.

There were several amendments by pro-abortion Demcorats to take out the pro-life language in that committee. They all failed.

Nearly all committee Republicans voted against an amendment brought by pro-abortion Democrat Rep. Lizzie Fletcher to strike the language that would prohibit Planned Parenthood from receiving federal funds, even through Medicaid payments. Republican Reps. Mariannette Miller-Meeks and Gabe Evans did not vote on the amendment.

Susan B. Anthony Pro-Life America, a leading pro-life group, celebrated that vote.

“We congratulate Energy and Commerce Committee Chairman Brett Guthrie and House GOP allies for their hard work on a budget that serves moms, babies and taxpayers alike. SBA will proudly score in favor of this ‘one big beautiful bill’ that includes the vital priority of stopping forced funding of the abortion industry. To no one’s surprise, pro-abortion Democrats peddled lies and ran cover for abortion businesses like Planned Parenthood,” the group told LifeNews.

“Their taxpayer funding increased almost $100 million in one year, hitting $792.2 million in 2023, as health care like pap smears and breast exams plummeted – all while ending a record 402,230 babies’ lives,” it added. “We applaud pro-life congresswomen Harshbarger, Houchin, Fedorchak and Lee for speaking out during the debate to set the record straight and defeat a Democrat amendment that would have kept funneling money to Big Abortion. The Big Abortion industry is focused on profits, politics and lawfare, not providing quality services for low-income women in a safe environment. Patients are far better off going to community health centers that outnumber Planned Parenthood 15:1, where Medicaid recipients among others can get much more comprehensive care.”

Last week, a few Republicans in the House and Senate expressed their reservations about defunding Planned Parenthood within the budget bill. Asked about that, President Donald Trump expressed confidence that Republicans will resolve internal disagreements to advance legislation defunding Planned Parenthood.

“I don’t know yet. I have to see because you’re just telling me that for the first time, we’ll work something out,” Trump said in response.

The reconciliation process, which allows legislation to pass the Senate with a simple majority, offers Republicans a rare opportunity to strip federal funding from Planned Parenthood, the nation’s largest abortion business. Pro-life groups argue that taxpayer dollars, even if not directly funding abortions, indirectly subsidize Planned Parenthood’s operations, which include killing over 390,000 babies every year.

Pro-life advocates emphasize that community health centers, which outnumber Planned Parenthood clinics and provide comprehensive care without abortions, can absorb patients if funding is redirected.

House Speaker Mike Johnson, a staunch pro-life advocate, has signaled that defunding “big abortion” is a priority in the reconciliation bill, which also addresses Trump’s agenda on taxes, border security, and energy.

The Hyde Amendment already prohibits federal funds from directly paying for abortions, except in cases of rape, incest, or to save the mother’s life. However, Planned Parenthood receives approximately $700 million annually through Medicaid reimbursements and Title X grants. Pro-life leaders argue this funding frees up resources for Planned Parenthood’s abortion operations.

The reconciliation bill, which allows legislation to pass with a simple majority in both chambers, is seen as a critical opportunity to strip federal funding from Planned Parenthood, the nation’s largest abortion business. The abortion company received nearly $700 million in taxpayer funds in its 2022-2023 fiscal year, killing 392,715 babies in abortions, according to its annual report.

Meanwhile, Representative Mary Miller (R-Ill.) is waging a fierce campaign among her Republican colleagues to make defunding Planned Parenthood a non-negotiable piece of the final proposal.

Miller sent a passionate letter to Rep. Brett Guthrie (R-Ky.), chairman of the House Committee on Energy and Commerce, obtained by Breitbart News. In it, she urged Guthrie to “use every legislative option available to cease all federal funds going to Planned Parenthood,” exposing the organization’s deep entanglement in abortion and transgender treatments. “Abortions and transgender treatments have exploded in clinics across the country,” she wrote.

Citing the Charlotte Lozier Institute, Miller highlighted that “abortions made up 97.1% of Planned Parenthood’s pregnancy services from 2021-2022, performing nearly 400,000 abortions.” She also underscored the crisis in her home state, noting, “In 2023, my home state of Illinois performed 72,143 abortions, the most in our history since the state started reporting abortion totals in 1973.” Miller laid bare Planned Parenthood’s financial empire, stating, “Due to a lack of decisive Congressional action, Planned Parenthood has become a federally funded health network with private assets valued at $2.5 billion. Recent numbers show that Planned Parenthood received nearly $700 million in taxpayer revenue from 2022-2023.”

Her letter concluded with a call to action: “It is essential that we protect taxpayer dollars and stop funding this organization. President Trump has already issued an Executive Order that implements such a plan. Therefore, I urge you to do everything possible to ensure Planned Parenthood never receives another penny of taxpayer dollars.”

Speaking to Breitbart, Miller doubled down, declaring, “Planned Parenthood is a multi-billion-dollar abortion business that continues to receive millions in federal funding.” She praised Trump’s leadership, stating, “President Trump had it right when he issued an Executive Order to cut off taxpayer dollars from abortion providers like Planned Parenthood,” and insisted, “it’s time for Congress to make that policy permanent. I urge the Energy and Commerce Committee to ensure that not another dime of American tax dollars goes to this murder-for-profit organization.”

The post Steve Scalise: House Will Pass Bill to Defund Planned Parenthood Next Week appeared first on LifeNews.com.

-

Site: Real Jew News

Episode 80: White Culture And The Church

May 16 2025___________________________________

More Vids!

+BN Vids Archive! HERE!

___________________________________

Support The Brother Nathanael Foundation!

Br Nathanael Fnd Is Tax Exempt/EIN 27-2983459

Or Send Your Contribution To:

The Brother Nathanael Foundation, POB 547, Priest River, ID 83856

E-mail: brothernathanaelfoundation([at])yahoo[dot]com

Scroll Down For Comments

-

Site: non veni pacem

Have you noticed the “Republicans” can’t seem to cut a single dollar from the budget? The whole DOGE thing was smoke and mirrors. The current budget proposal would add another $10T to the debt over the next four years. Quite the Big Beautiful Bill, isn’t it? Good for Moody’s. Drop the bomb and see if it shakes any sense into them. -nvp

Moody’s downgrades United States credit rating, citing growth in government debt

Moody’s Ratings cut the United States’ sovereign credit rating down one notch to Aa1 from Aaa, the highest possible, citing the growing burden of financing the federal government’s budget deficit and the rising cost of rolling over existing debt amid high interest rates.

“This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns,” the rating agency said in a statement.

The decision to lower the United States credit profile would be expected, at the margin, to lift the yield that investors demand in order to buy U.S. Treasury debt to reflect more risk, and could dampen sentiment toward owning U.S. assets, including stocks. That said, all the major credit rating agencies continue to give the United States their second-highest available rating.

The yield on the benchmark 10-year Treasury note climbed 3 basis points in after-hours trading, trading at 4.48%. The iShares 20+ Year Treasury Bond ETF — a proxy for longer term debt prices — fell about 1% in after hours trading, while the SPDR S&P 500 ETF Trust that tracks the benchmark index for U.S. stocks dropped 0.4%.

Moody’s had been a holdout in keeping U.S. sovereign debt at the highest credit rating possible, and brings the 116-year-old agency into line with its rivals. Standard & Poor’s downgraded the U.S. to AA+ from AAA in August 2011, and Fitch Ratings also cut the U.S. rating to AA+ from AAA, in August 2023.

“Successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs,” Moody’s analysts said in a statement. “We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.”

-

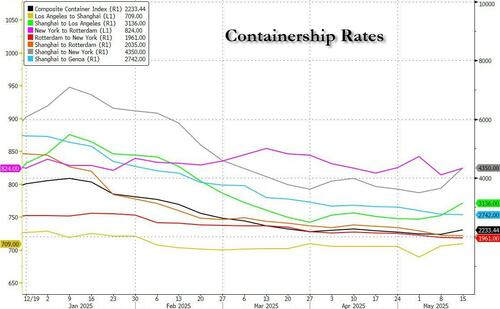

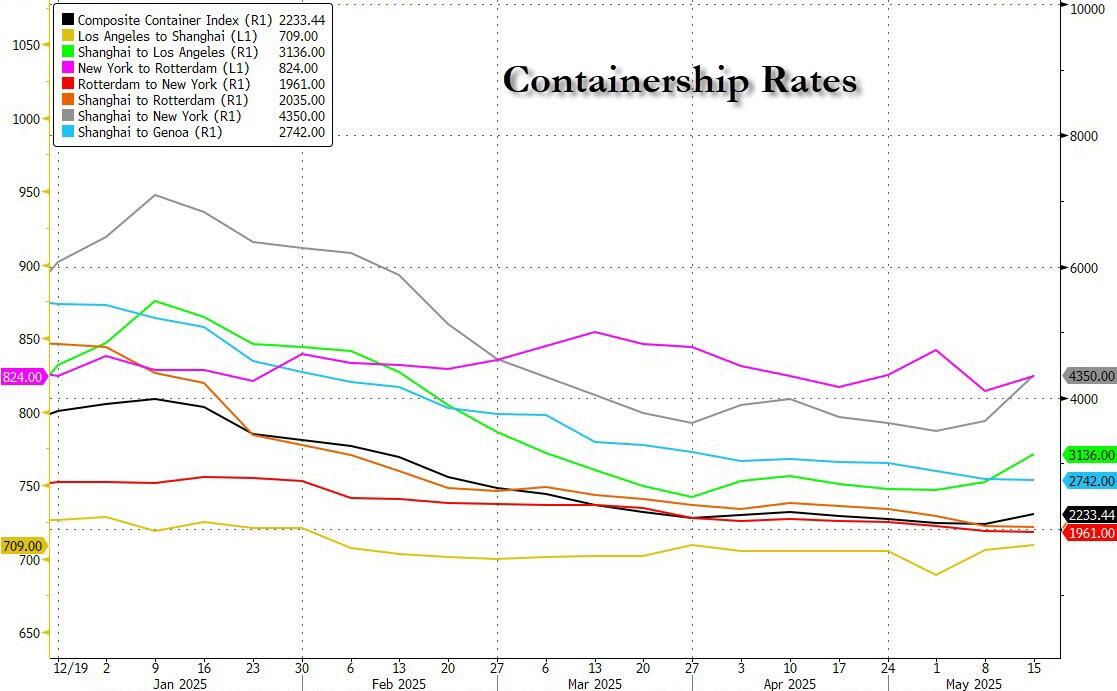

Site: Zero HedgeHapag-Lloyd Sees 50% Surge In Container Bookings From China To The USTyler Durden Fri, 05/16/2025 - 18:15

Bt Stuart Chirls of Freightwaves

Hapag-Lloyd saw container bookings from China to the United States jump by 50% following the break in the tariff battle between the trading partners.

In comments during an earnings call, Chief Executive Rolf Habben Jansen explained that while recent bookings were down 20%-30%, there has been “a surge of over 50% in recent days,” though he noted the difficulty in predicting exact growth patterns.

“We expect capacity to return fairly swiftly. We have deployed smaller ships instead of doing blanks [canceled sailings], and we will reverse that soon. Within the next couple of weeks, we will deploy bigger ships again, and others may also increase capacity as the quarter progresses.”

The CEO also confirmed that upsizing vessels can be accomplished without significant disruption due to the simplified Gemini network with Maersk, and that it “won’t materially change overall costs,” with no current issues regarding mispositioning of containers.

Profit increased 45% to $469 million on revenue that was up 15% year over year to $5.3 billion in the first quarter, driven by a 9% increase in liner shipping volumes, marking the highest year-on-year growth in several years.

Liner shipping saw revenues of $5.2 billion on volume of 3.3 million twenty-foot equivalent units and an average freight rate of $1,480 per TEU, both of which were 9% higher y/y on strong demand. Earnings before interest, taxes, depreciation and amortization rose by 18%, to $1.1 billion, and earnings before interest and taxes were up by 25%, to $472 million.

The successful launch of the Gemini network saw schedule reliability of 90%, a remarkable figure in an industry that is usually around 65%.

The carrier faced operational challenges during the quarter, including ongoing rerouting of ships away from the Red Sea and around the Cape of Good Hope, as well as disruptions at various ports. These challenges increased operational costs and impacted efficiency but were effectively managed to minimize adverse effects on overall performance.

-

Site: Zero HedgeAmerica's Next Top Migrant: White House Denies Noem Backing DHS Citizenship Game ShowTyler Durden Fri, 05/16/2025 - 17:50

The White House has denied a report that DHS Secretary Kristi Noem is backing a proposal for a reality TV series that pits immigrants against each other for the grand prize: a fast-track to U.S. citizenship.

According to a 35-page pitch obtained by DailyMail.com, the Department of Homeland Security has been in contact with reality TV producer Rob Worsoff - known for Duck Dynasty and Millionaire Matchmaker - on a show called The American. The show would take a dozen pre-vetted immigrants on a cross-country journey aboard a train, competing in “cultural” challenges like assembling a Model T Ford in Detroit, rolling logs in Wisconsin, and digging clams in Maine.

Contestants would be greeted in New York City at Ellis Island by “a famous, naturalized American who was also born in another country,” the pitch reads, with names like Sofia Vergara, Ryan Reynolds, and Mila Kunis floated as possible hosts. Each contestant would receive a personalized baseball glove before hitting the rails aboard “The Citizen Ship.”

"Along the way, we will be reminded what it means to be American – through the eyes of the people who want it most," Worsoff’s pitch says.

There’d be elimination rounds, dramatic town halls, and viewer voting tallied by U.S. Citizenship and Immigration Services staff - yes, actual DHS employees, according to the proposal. The live finale would see the train stop in Washington, D.C., with the winner sworn in on Capitol Hill as Thunderbird jets roar overhead. "There won't be a dry eye within 10 miles!" the pitch promises.

Game show prizes? Think red-white-and-blue Americana: 1 million American Airlines points, a $10,000 Starbucks gift card, or a lifetime supply of 76 gasoline.

Tricia McLaughlin, DHS’s top spokesperson, confirmed the department had a call with Worsoff last week. "I think it's a good idea," she said. Though she claimed Noem “is yet to be briefed,” DailyMail.com reports Noem supports the show and wants to move forward.

DHS Distances

That said, DHS on Friday confirmed that it had received the pitch - but a spokesperson denied the Mail's report that Noem was involved. In a statement to the Epoch Times, DHS Assistan Secretary Tricia McLaughlin called the Mail's reporting "completely false," and denied claims that Noem had either "backed" or "reviewed" the plan.

"The Department of Homeland Security receives hundreds of television show pitches a year, ranging from documentaries surrounding ICE and CBP border operation to white collar investigations by HSI," she said, referring to Immigration and Customs Enforcement, Customs and Border Protection, and Homeland Security Investigations.

TV show proposals undergo “a thorough vetting process prior to denial or approval,” McLaughlin said, adding that the reality TV “show in question is in the very beginning stages of that vetting process and has not received approval or denial by staff.”

Separately, McLaughlin told news outlets that she had spoken with the producer of the proposed reality show. -Epoch Times

Worsoff, a Canadian-born producer, said, “I’m not affiliated with any political ideology. As an immigrant myself, I am merely trying to make a show that celebrates the immigration process.”

The proposal also includes themed challenges like mining for gold in San Francisco, launching rockets in Cape Canaveral, and rafting down the Arkansas River. “We'll join in the laughter, tears, frustration, and joy – hearing their backstories – as we are reminded how amazing it is to be American,” the pitch reads.

Even the losers would have “a leg-up” in the naturalization process, the proposal notes.

For a secretary already accused of turning immigration enforcement into a branding exercise, The American is on-brand. Whether the public buys into her vision — or sees it as one more cringe photo op — remains to be seen.

Side note - the book 'Running Man' takes place in 2025...

-

Site: Zero HedgeUS Drug Overdose Deaths Fall Nearly 27 Percent To Lowest Level In 5 YearsTyler Durden Fri, 05/16/2025 - 17:25

Authored by Tom Ozimek via The Epoch Times (emphasis ours),

Drug overdose deaths in the United States dropped sharply in 2024, falling to their lowest level since before the pandemic, according to provisional data released on May 14 by the Centers for Disease Control and Prevention (CDC).

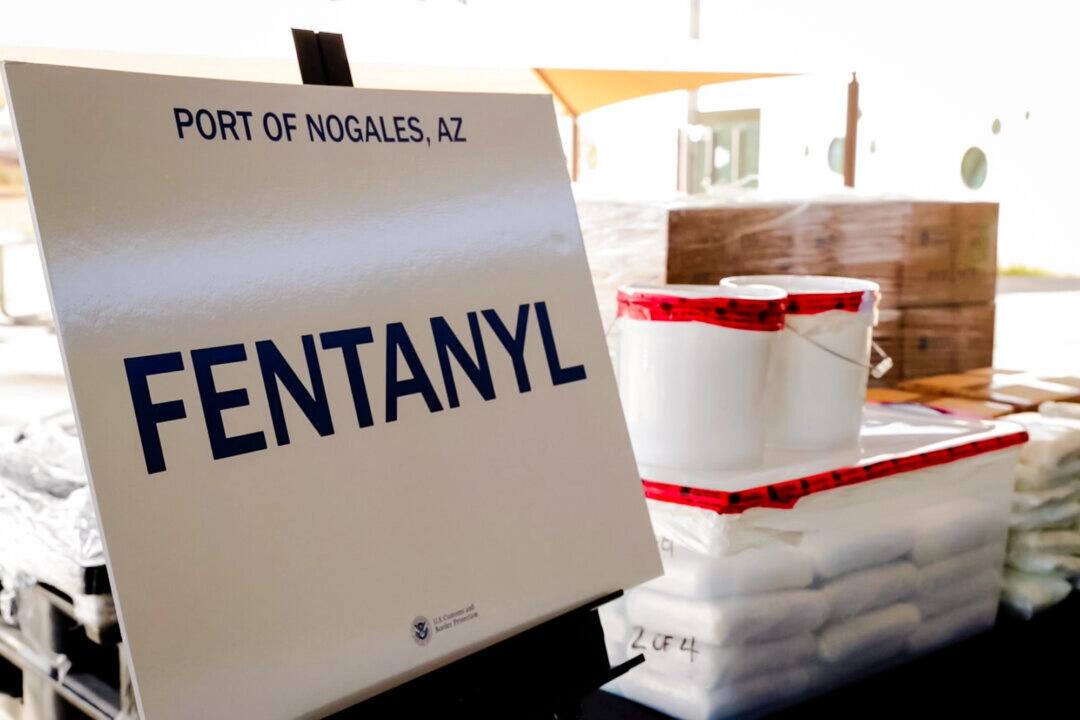

Packets of fentanyl and methamphetamine seized from a truck crossing into Arizona from Mexico are displayed during a news conference at the Port of Nogales, Ariz., on Jan. 31, 2019. U.S. Customs and Border Protection/Reuters

Packets of fentanyl and methamphetamine seized from a truck crossing into Arizona from Mexico are displayed during a news conference at the Port of Nogales, Ariz., on Jan. 31, 2019. U.S. Customs and Border Protection/Reuters

The report estimates that 80,391 people died of a drug overdose in 2024—a 26.9 percent decline from 110,037 in 2023, marking the largest one-year drop since the agency began collecting comparable data more than four decades ago.

It’s the second consecutive annual decrease after overdose deaths surged during and after the COVID-19 pandemic. Social isolation, disruptions to treatment, and other factors helped push fatalities to a peak of nearly 115,000 in 2023.

All but two states—Nevada and South Dakota—recorded declines last year, with especially steep drops in hard-hit areas such as West Virginia, which reported a 43.5 percent decrease. While the final figures may shift slightly as data are finalized, the CDC data indicate an unmistakable downward trend.

The decline was driven almost entirely by a reduction in fentanyl-related deaths. The synthetic opioid—at least 50 times more potent than heroin—was linked to more than 76,000 deaths in 2023, but that number dropped to just over 48,000 in 2024.

Experts have cited several possible reasons for the downturn, including expanded access to the overdose reversal drug naloxone—sold as Narcan—which became available over the counter in 2023. It is now carried by most first responders. Increased use of addiction treatment medications and changes in drug supply patterns may also be factors.

Despite the improvement, the new data revealed troubling increases in deaths tied to stimulants such as methamphetamine and cocaine.

Fatalities involving meth rose from 29,456 to 37,096, while cocaine-related deaths jumped by about 8,000, reaching 30,833. Since overdose statistics often overlap—many deaths involve multiple substances—it remains unclear how many of these fatalities involved stimulants alone.

The Trump administration has intensified efforts to choke off the international supply chain responsible for flooding the country with synthetic opioids.

While most fentanyl consumed in the United States is manufactured in Mexico, the raw chemicals used to make it overwhelmingly come from China. A Pulitzer Prize-winning investigation by Reuters last year exposed how Chinese chemical suppliers and Mexican cartels continue to enable the epidemic.

Reporters were able to legally purchase all the chemicals and equipment needed to produce $3 million worth of fentanyl for just $3,600—exploiting a since-closed customs loophole known as the “de minimis” rule. That exemption had allowed goods valued at or under $800 to be imported duty-free.

A recent report from the House Select Committee on the Chinese Communist Party (CCP) found that Beijing is not only failing to stop the export of fentanyl precursors but is actively encouraging it.

According to the report, the Chinese regime offers tax rebates and state subsidies to companies producing illegal synthetic opioid components, fueling what lawmakers call a deliberate assault on the United States.

“Through its actions, as our report has revealed, the Chinese Communist Party is telling us that it wants more fentanyl entering our country,” Select Committee Chair Mike Gallagher (R-Wis.) said during an April 16, 2024, hearing. “It wants the chaos and devastation that has resulted from this epidemic. And yes, that means more dead Americans.”

In response, the Trump administration in February announced a new round of targeted tariffs on China’s synthetic drug supply chain, aiming to disrupt the production and export of fentanyl precursors.

-

Site: Zero HedgeMoody's Downgrades USA Credit Rating From AaaTyler Durden Fri, 05/16/2025 - 17:05

Earlier this week, we noted that short-dated USA sovereign CDS were trading wider than China and Greece as trade policy uncertainty and the debt ceiling 'X-date' loomed...

...well, it appears Moody's Rating Agency noted it too... because they just downgraded the Government of United States of America's (US) long-term issuer and senior unsecured ratings to Aa1 from Aaa and changed the outlook to stable from negative.

The one-notch cut comes more than a year after Moody’s changed its outlook on the US rating to negative, with Moody's joining Fitch Ratings and S&P Global Ratings in grading the world’s biggest economy below the top, triple-A position.

This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns.

Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs.

We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.

Over the next decade, we expect larger deficits as entitlement spending rises while government revenue remains broadly flat.

In turn, persistent, large fiscal deficits will drive the government's debt and interest burden higher.

The US' fiscal performance is likely to deteriorate relative to its own past and compared to other highly-rated sovereigns.

The stable outlook reflects balanced risks at Aa1.

The US retains exceptional credit strengths such as the size, resilience and dynamism of its economy and the role of the US dollar as global reserve currency. In addition, while recent months have been characterized by a degree of policy uncertainty, we expect that the US will continue its long history of very effective monetary policy led by an independent Federal Reserve.

The stable outlook also takes into account institutional features, including the constitutional separation of powers among the three branches of government that contributes to policy effectiveness over time and is relatively insensitive to events over a short period.

While these institutional arrangements can be tested at times, we expect them to remain strong and resilient.

The US' long-term local- and foreign-currency country ceilings remain at Aaa.

The Aaa local-currency ceiling reflects a small government footprint in the economy and extremely low risk of currency and balance of payment crises.

The foreign-currency ceiling at Aaa reflects the country's strong policy effectiveness and an open capital account, reducing transfer and convertibility risks.

RATIONALE FOR THE RATINGS DOWNGRADE TO Aa1

Over more than a decade, US federal debt has risen sharply due to continuous fiscal deficits.

During that time, federal spending has increased while tax cuts have reduced government revenues.

As deficits and debt have grown, and interest rates have risen, interest payments on government debt have increased markedly.

Without adjustments to taxation and spending, we expect budget flexibility to remain limited, with mandatory spending, including interest expense, projected to rise to around 78% of total spending by 2035 from about 73% in 2024.

If the 2017 Tax Cuts and Jobs Act is extended, which is our base case, it will add around $4 trillion to the federal fiscal primary (excluding interest payments) deficit over the next decade.

As a result, we expect federal deficits to widen, reaching nearly 9% of GDP by 2035, up from 6.4% in 2024, driven mainly by increased interest payments on debt, rising entitlement spending, and relatively low revenue generation.

We anticipate that the federal debt burden will rise to about 134% of GDP by 2035, compared to 98% in 2024.

Despite high demand for US Treasury assets, higher Treasury yields since 2021 have contributed to a decline in debt affordability.

Federal interest payments are likely to absorb around 30% of revenue by 2035, up from about 18% in 2024 and 9% in 2021. The US general government interest burden, which takes into account federal, state and local debt, absorbed 12% of revenue in 2024, compared to 1.6% for Aaa-rated sovereigns.

While we recognize the US' significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics.

Moody's couldn't help but take a shot at Trump's tariffs:

The US economy is unique among the sovereigns we rate.

It combines very large scale, high average incomes, strong growth potential and a track-record of innovation that supports productivity and GDP growth.

While GDP growth is likely to slow in the short term as the economy adjusts to higher tariffs, we do not expect that the US' long-term growth will be significantly affected.

But they did say something positive...

Despite reserve diversification by central banks globally over the past twenty years, we expect the US dollar to remain the dominant global reserve currency for the foreseeable future.

...

Moreover, the resilience of the US sovereign rating to shocks is supported by strong monetary and macroeconomic policy institutions.

Although policy has been less predictable in recent months, relative to what has typically been the case in the US and other highly-rated sovereigns, we expect that monetary and macroeconomic policy effectiveness will remain very strong, preserving macroeconomic and financial stability through business cycles.

The timing is exceptional, as Republicans try to get Trump's 'big beautiful bill' out of committee... and as everyone knows, there's no such thing as a coincidence in Washington.

US equity markets are trading down after hours on the news:

Trump's gonna be pissed!!

-

Site: Zero HedgeTrump Tax Bill Fails To Advance As Conservative Holdouts Double Down On 'No'Tyler Durden Fri, 05/16/2025 - 17:00

Update (1210ET): The House Budget Committee has voted down the reconciliation bill by a vote of 16-21 - with GOP Reps. Clyde, Roy, Breechen, Norman and Smucker (who flipped his vote) all voting "no".

Speaker Mike Johnson (L), President Donald Trump, Rep. Chip Roy (R-TX)

Speaker Mike Johnson (L), President Donald Trump, Rep. Chip Roy (R-TX)

"This bill falls profoundly short. It does not do what we say it does with respect to deficits," said Rep. Chip Roy.

Rep. Andrew Clyde (R-GA) said "I am unable to support this package in its current form, but I look forward to strengthening this bill to ensure that it does pass, so that we full all of our America First promises to the American people."

Whilst Ralph Norman (R-SC) said "Sadly, I’m a hard no until we get this ironed out."

According to Punchbowl's Jake Sherman, Smucker likely flipped "no" to preserve the ability to reconsider the bill at a later time.

House Budget Committee Chairman Rep. Jody Arrington (R-TX) said after the vote "I do not anticipate us coming back today."

* * *

A fiery intra-party fight exploded on Capitol Hill Friday as House Republicans clashed over President Donald Trump's mammoth "One Big Beautiful Bill," with Trump himself jumping into the fray to torch conservative holdouts as attention-hungry "grandstanders."

As the House Budget Committee met to advance the 1,116-plus-page megabill - packed with Trump’s signature proposals on taxes, Medicaid, and immigration - chaos broke out behind the scenes, and in front of the cameras, as hardline conservatives threatened to blow up the entire process.

"Republicans MUST UNITE behind ‘THE ONE, BIG BEAUTIFUL BILL!’" Trump posted on Truth Social. "We don’t need ‘GRANDSTANDERS’ in the Republican Party. STOP TALKING, AND GET IT DONE!"

The scorched-earth post came as the House Budget Committee met down to mark up the massive reconciliation bill, which bundles together much of Trump’s second-term policy wishlist: tax cuts, welfare reform, immigration crackdowns, and the death of Biden’s green energy subsidies.

But what was supposed to be a legislative victory lap turned into a high-stakes hostage crisis, with Speaker Mike Johnson (R-LA) caught between warring GOP factions, each demanding major changes and threatening to sink the bill if they don’t get their way.

Conservatives on the committee - Reps. Chip Roy, Ralph Norman, Andrew Clyde, and Josh Brecheen - signaled they were ready to vote against the bill unless major changes were made. Their demands include a faster phase-in of Medicaid work requirements, a ban on undocumented immigrants receiving federal benefits, and immediate termination of Inflation Reduction Act clean energy provisions.

"If they don’t [change it], I’m gonna vote no. We’ll kill it," Norman warned Thursday. "I don’t want to. But I will."

The vote is ongoing, with Roy and Norman both using their time during committee to voice their opposition, CNN's Sarah Farris reports.

Ok we're now at TWO no votes: Roy and Norman both used their time during committee to say they're opposed

— Sarah Ferris (@sarahnferris) May 16, 2025

Both Brecheen and Clyde supposed to speak now but neither are there to speak. If either opposes, it's done for today. https://t.co/pDIwEaw6zTThe tension spilled into full view Friday morning when Norman, Roy, and Clyde abruptly left the committee room moments before the markup was scheduled to begin, prompting immediate speculation they were staging a walkout. All three returned shortly afterward, saying little, but still signaling deep frustration.

Norman told reporters the situation was “very disappointing," adding “I hope they recess.”

Rep. Roy: “I'm not going home this weekend. I'm staying here all weekend and we're going to get this damn thing done but the right way.

— Rep. Chip Roy Press Office (@RepChipRoy) May 16, 2025

I'm not going to vote for a bad bill. I didn't come here to raise debt. I didn't come here to increase deficits. I didn't come here to cement… pic.twitter.com/0jcqR9cgz3Johnson, for his part, is trying to keep the circus moving. He has pledged to make some concessions - such as speeding up work requirement timelines and possibly harmonizing those across both Medicaid and SNAP - but every adjustment risks triggering a backlash from the other side of the GOP spectrum.

"If you push too hard on one side, the other side bulges out," opines Punchbowl News. "That’s exactly what’s happening here."

Very SALTy

Moderates are already howling over cuts to safety net programs and demanding changes of their own. Blue-state Republicans want the SALT deduction cap raised above the $30,000 ceiling currently in the bill. Rep. Don Bacon (R-NE) wants to remove language that would block legal refugees from getting food aid. And Florida Republicans are furious over a provision that clamps down on provider taxes - a method states use to draw more federal Medicaid dollars.

The markup itself became a theater of dysfunction - with Rep. Blake Moore (R-UT) joking about the fact that he went viral earlier this week for falling asleep during a late-night hearing. “I also appreciate that you schedule the markup during daylight hours,” he said. Chair Jodey Arrington (R-TX) fired back: “Some of the staff decided to chip in and equip your chair with an electric shocking mechanism... I hope that is also a bipartisan proposal.”

Unbelievable. Rep. Blake Moore falls asleep during a committee meeting and had to be woken up. pic.twitter.com/xSKPKkP628

— Thomas Sowell Quotes (@ThomasSowell) May 14, 2025But behind the laughs, the reality is grim. With Rep. Brandon Gill (R-TX) absent for the birth of his child, Johnson can’t afford even a single Republican defection if he wants the bill to make it out of committee.

Majority Leader Steve Scalise (R-LA) tried to downplay the drama, telling reporters, “The goal is to get it out of the committee today... because failure is not an option.”

How did we get here? These speed bumps aren’t surprising. This is a gigantic legislative grab-bag with lots of disparate priorities. We get that. It reminds us a bit of Build Back Better – which failed and led to the IRA, for what it’s worth. -Punchbowl News

Indeed, Speaker Johnson has tried to do what many before him could not: push through a comprehensive, everything-at-once bill that pleases both fire-breathing conservatives and centrist pragmatists. But by skipping the usual slow walk through committee education and member negotiations, he may have created a legislative trap for himself.

And of course, after all of this - the bill still has to get through the Senate...

Stay tuned for updates...

-

Site: LifeNews

A post-abortion woman named “Leena” tells the following story:

I’m now 21 years old, and I had my abortion 2 months ago… I was about six weeks pregnant.

It was, and has been, the hardest thing I’ve ever gone through in my life. I didn’t want to do it… I just felt stuck, like I had no choice.

My boyfriend and I had been together for only about six months, and were living together. We were not having protected sex, so my pregnancy was bound to happen.

He knew, before I did, that I was pregnant. He told me for a couple of weeks, and I kept saying, “Nah, nah… my period isn’t due yet.” But I was wrong.

One Saturday, I went to the grocery store to pick up my pregnancy test, and secretly took it that day. When the pink line came up fast, I was completely shocked. I walked out of the bathroom, not being able to speak, and just motioned for my boyfriend to go look in the bathroom.

SUPPORT LIFENEWS! If you want to help fight abortion, please donate to LifeNews.com!

The first thing he said to me was, “His name is Alex.” I was in more shock than he was, almost crying. But in the back of my mind, I was so happy. I’d always wanted a baby. I’d always imagined myself pregnant. It was finally happening for me.

For the next few days, my boyfriend told me he’d support me in whatever decision I made, whether it was to keep it, or have an abortion. I always said I didn’t know, but I secretly knew I wanted the baby. I figured, we’re both adults, we both work, and I’m planning on going back to school. To top it off, we’re in love and planned on getting married. I could do this.

But suddenly, he put down the line. I had to abort the baby. We weren’t ready financially or emotionally, he said. I didn’t want to. I cried, and cried.

I couldn’t function during the day. I made an appointment at the abortion clinic. I cried, and cried. The night before my appointment, I cried, and begged him to let me keep it.

There was nothing more I wanted than to keep this baby. I wish I would have been stronger. But I wasn’t, and I went through with it. The morning of my appointment was dark and rainy. We drove, and I was numb.

Once we got inside, I was shocked at how many women/girls were there. I cried from the time that they called my name, to the time I went under anesthesia.

It was the scariest thing I’ve ever been through. And I would never go through it again.

To this day, I hate seeing pregnant women. It can ruin my day to see one. Babies, even.

It breaks my heart to know that in February, I would have had my own. The worst thing is that I feel like I don’t have anyone to talk to.

My boyfriend and I are still together, but it’s not the same. He doesn’t understand what it feels like. God love him, he does try. But a man will never know what an abortion feels like.

The moment you find out your pregnant, you have an instant bond… something that no one will never be able to understand until they experience it themselves.

Did I do the right thing? I still ask myself that everyday. If I took away the emotions, I would say, “Yes.” I’m only 21 years old, and I still have my entire life.

I’m trying to get through school, and work full time to get through it. My boyfriend and I are broke. We are scraping by, with rent every month. Financially, we could not support a baby right now.

But, with the emotions? Yes, I wish I did have that baby. That was my child and, even without any money at all, that would be the love of my life… So its hard to say. Its over now, and I have to get on with my life.

I will always love that little boy with all of my heart and, someday, I’ll have him again. Till then, I just have to learn to be strong.

LifeNews Note: Sarah Terzo covered the abortion issue for over 13 years as a professional journalist. In this capacity, she has written nearly a thousand articles about abortion and read over 850 books on the topic. She has been researching and writing about abortion since attending The College of New Jersey (class of 1997) where she minored in Women’s Studies. This article originally appeared on Sarah Terzo’s Substack. You can read more of her articles here.

The post I Wanted to Keep My Baby, But My Boyfriend Pressured Me Into Abortion appeared first on LifeNews.com.

-

Site: Catholic ConclaveCardinal Bishop of Algiers, modernists to the rescue?During the days before the Conclave, in the normal and predictable whirlwind of voices and interviews that these occasions arouse, we had missed the interview given to the daily newspaper of the CEI "Avvenire", on April 29, 2025 (here), by His Eminence Cardinal Jean Paul Vesco, O.P., Cardinal Archbishop of AlgiersThe interview, as you will Catholic Conclavehttp://www.blogger.com/profile/06227218883606585321noreply@blogger.com0

-

Site: Catholic ConclaveAs one of three Papal electors from Germany, Cardinal Reinhard Marx participated in the conclave. In an interview, he now reflected on his first meeting with Cardinal Prevost and commented on the Vatican's financial situation.From the perspective of Munich Cardinal Reinhard Marx, there was only "very isolated" criticism of Pope Francis in the pre-conclave. Trying to pretend nothing is going Catholic Conclavehttp://www.blogger.com/profile/06227218883606585321noreply@blogger.com0

-

Site: LifeNews

Craig Paton reported for the Independent on May 13, 2025 on the Not Dead Yet UK rally outside Holyrood (Scottish parliament) as the Liam McArthur assisted suicide bill was debated and voted on.

The rally opposing assisted suicide featured actress Liz Carr and Scottish Labour MSP Pam Duncan-Glancy.

Paton reported that Silent Witness star Liz Carr told campaigners outside the Scottish Parliament that:

“I am so fed up of having to answer strangers’ questions, even in this day and age, who think that being us must be the worst thing imaginable,” she said to campaigners, which included a number of disabled people.

Click here to sign up for pro-life news alerts from LifeNews.com

“That having pain, having difficulty with everyday activities, must mean that it would be better if we were dead – that is not the case.”

Paton reported that Liz Carr qualifies for assisted suicide under the bill.

“But it also has a definition that I would qualify under, I would define myself as a disabled person, but actually the definition of having a progressive condition, I would come under that.

“So the potential for this to include far more than just those with true terminal illnesses … those as well with degenerative conditions, is what concerns so many of us and so many of the people that are here today.”

Scottish Labour MSP Pam Duncan-Glancy, who strongly opposes assisted suicide, also spoke at the rally. Paton reported:

Addressing the dozens of campaigners outside Holyrood, Ms Duncan-Glancy said: “If any of my colleagues are in any doubt whatsoever, if in doubt: don’t.”

She added: “The risk is too high.

“And so I hope that my colleagues will listen carefully to that and will not support this legislation this afternoon.

“I know that I will, on behalf of all of you, go in there and fight for out lives.”

The bill passed at second reading by a vote of 70 to 56. The bill will now go to committee and a final vote is expected later this year.

LifeNews.com Note: Alex Schadenberg is the executive director of the Euthanasia Prevention Coalition and you can read his blog here.

The post Disabled People are Not “Better off Dead” appeared first on LifeNews.com.

-

Site: Fr. Z's BlogOn this Feast of St. John Nepomuceno the sun came into view at 5:47. We will lose sight of it again at 20:27. Our ears will not hear the un-run Ave Maria Bell at 20:45 in the Roman Curia, but … Read More →

-

Site: Catholic ConclaveIn the final year of his Pontificate, Pope Francis repeatedly pointed out the Vatican's dramatic deficit. While Cardinal Marx sees a clear need for action, he warns against panic-mongering – and explains what he believes is behind the headlineMunich Cardinal Reinhard Marx rejects reports of deep red figures in the Vatican. "I can't confirm that. The situation isn't as catastrophic as some claim,"Catholic Conclavehttp://www.blogger.com/profile/06227218883606585321noreply@blogger.com0

-

Site: RT - News

James Comey knew exactly what his recent cryptic social media post meant, the US president has claimed

US President Donald Trump has accused former FBI director James Comey of posting a since-deleted social media post calling for his “assassination.”

Comey posted a photograph of seashells spelling out the numbers ‘86 47’ in a now-deleted Instagram post on Thursday. He captioned the cryptic post with “cool shell formation on my beach walk.”

White House officials and Republicans quickly interpreted the post as a coded threat to the 47th US president, arguing that the number 86 is intended as slang for ‘get rid of’ or ‘kill’.

Comey subsequently deleted the image and explained in a separate post: “I posted a picture earlier of some shells I saw on a beach walk, which I assumed were a political message. I didn’t realize some folks associate those numbers with violence. It never occurred to me but I oppose violence of any kind so I took the post down.”

Trump isn’t convinced.

“He knew exactly what that meant. A child knows what that meant,” he told Fox News in an interview on Friday.

That meant assassination. And it says it loud and clear.

“If you’re the FBI director… and you don't know what that meant? Now, he wasn’t very competent, but he was competent enough to know what that meant,” the president added.

Donald Trump Jr. also saw Comey’s Instagram post as a call to murder his father.

Just James Comey causally calling for my dad to be murdered.

— Donald Trump Jr. (@DonaldJTrumpJr) May 15, 2025

This is who the Dem-Media worships. Demented!!!! pic.twitter.com/4LUK6crHATDirector of National Intelligence Tulsi Gabbard said Comey could face legal consequences for the incident.

Read more Ex-FBI director Comey under investigation for ‘call to assassinate Trump’

Ex-FBI director Comey under investigation for ‘call to assassinate Trump’

“The rule of law says people like him who issue direct threats against the president of the United States, essentially issuing a call to assassinate him, must be held accountable under the law,” she said in an interview with Fox News on Friday.

Comey and Trump have been at odds for years. The US president fired him as the FBI director in 2017, during his first term in the White House. Trump later accused him of spreading “false statements and lies” and of being a “dirty cop.”

During his 2024 reelection campaign, Trump survived an assassination attempt when a gunman took shots at him during a rally in Butler, Pennsylvania. The would-be assassin grazed Trump’s ear with a bullet, killed a spectator in the crowd behind him, and injured several others. In addition, at least one other plot to kill Trump was foiled in the lead-up to last year’s election.

-

Site: LifeNews

Despite the U.S. Supreme Court overturning Roe v. Wade and Planned Parenthood v. Casey on June 24, 2022, Planned Parenthood aborted more unborn children during the 2023-2024 fiscal year than the previous year and brought in a $100 million increase in taxpayer funding.

In the recently released 2023-2024 fiscal year annual report titled, “A Force for Hope,” Planned Parenthood performed 402,230 abortions during that time. That is an increase of nearly 10,000 abortions over the previous year (392,715).

The report also showed Planned Parenthood received about $792.2 million in “Government Health Services Reimbursements & Grants” versus $699.3 million from the previous year. U.S. taxpayers are

Click here to sign up for pro-life news alerts from LifeNews.com

Planned Parenthood’s largest financial contributor by supplying 39 percent of the organization’s $2 billion in revenue.

The nation’s largest abortion business, which commits over 1,100 abortions per day, presents killing unborn children and harming women as “inspiring hope.” The annual report begins, “Every time a patient walks through the doors of a Planned Parenthood health center, it is an act of hope — hope that they’ll get the care they need, that their decisions about their own bodies will be honored, that they’ll be truly seen. Every time a young person searches online for health information, their hope is that someone, somewhere has unbiased, real answers. Every time someone takes a birth control pill, or gets their IUD taken out, or goes with their partner for STI testing, they are filled with hope that the future they plan is possible.”

Twelve states now have banned elective abortions, and six states passed restrictions at or before 12 weeks of pregnancy. However, Planned Parenthood reports how it “helped” more than 100,000 women seeking abortions in the past year, particularly those who traveled from pro-life states elsewhere. More than 12,500 women received on average $275 to go toward travel costs. That’s more than $3.4 million in direct funding for abortion travel.

Chemical abortions now account for at least 63 percent of all U.S. abortions, an increase from 53 percent in 2020. Contributing to that is a new telehealth platform that Planned Parenthood provides in 42 states and Washington, D.C., for many services, including abortion pills to women who do not have to see a doctor in person to be screened for complications.