The following paragraph, courtesy of Amazon, reviews the book Death of the Dollar by William Rickenbacker.

Death of the Dollar by William F. Rickenbacker is a critical examination of the economic policies and monetary mismanagement that the author argues are eroding the value of the U.S. dollar and threatening financial stability. Rickenbacker contends that the actions of money managers, including excessive government spending, inflationary policies, and the detachment of the dollar from the gold standard, are systematically devaluing the currency. The book warns of an impending monetary disaster, highlighting how these policies disproportionately harm everyday citizens who rely on the dollar’s stability for savings and investments. Through a blend of economic analysis and historical context, Rickenbacker underscores the dangers of unchecked financial intervention and the potential for a collapse of the dollar’s purchasing power.

Plenty of books, articles, and social media posts herald the same grim forecast as Rickenbacker. For the most part, they rely on similar reasoning. Essentially, lax monetary policy and gross fiscal spending, both deemed to be inflationary, will result in dollar devaluation and ultimately the death of the dollar.

The difference between Rickenbacker’s book and other dollar demise forecasts is that Death of the Dollar was written in 1968! Fifty-seven years later, despite, or possibly because of Rickenbacker’s justifications, the dollar is still the world's reserve currency, and no other sovereign currency, cryptocurrency, or precious metal will replace it anytime soon.

Given the topic's importance and the gross misinformation spread about the dollar’s imminent demise, we review Rickenbacker’s thesis to highlight that today’s warnings have been around for decades and why the odds of them coming to fruition this time are very low, as they were decades ago.

Removal Of The Gold Standard

Rickenbacker’s book was published in 1968, three years before President Nixon closed the gold window, essentially making the dollar a fiat currency. While his book accurately predicted that ground-shaking event, it did not correctly anticipate its impact.

He reasoned that without gold regulating the supply of dollars, unchecked monetary policy would result in reckless “money printing.”

He was correct that the Fed would have more flexibility in managing the money supply. Furthermore, with this added power, we have seen reckless behavior, as he theorized. However, Rickenbacker erred on the money printing allegation.

The Fed doesn’t print money. All money is lent into creation by banks. The Fed prints bank reserves, which allow banks to make loans, i.e., print money, if they choose. More importantly, even if the money supply increases due to Fed incentives to lend, it's unclear whether such activity is good or bad for the economy and how it impacts inflation and ultimately the dollar’s value. That is a function of the productivity of debt.

Simply, productive debt drives economic growth, increases the nation's prosperity, and reduces deficits as a percentage of economic activity. Unproductive debt detracts from economic growth and prosperity and worsens deficits. Weaker growth from unproductive debt tends to be disinflationary.

As judged by an increasing debt-to-GDP ratio, aggregate debt has been unproductive, leading to lower inflation growth rates. Thus, if the concern is that “money printing” would lead to inflation, it may lead to disinflation.

Fed Flexibility

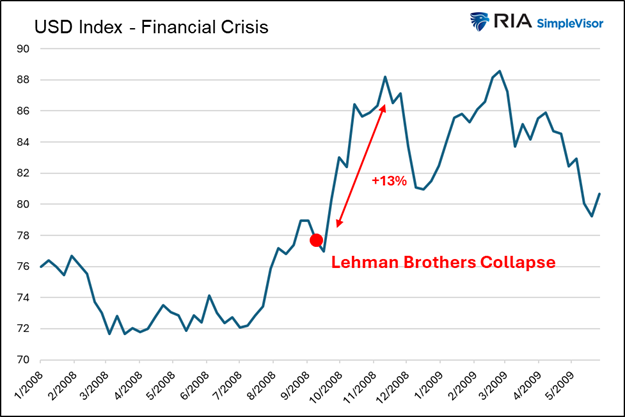

In one respect, Rickenbacker correctly said that giving the Fed more flexibility was a curse. Easy money policy has led to periods of gross speculation and crises, such as in 2008.

However, without the gold shackles, the Fed has incredible power to manage economic crises and avoid a currency collapse. In fact, despite the 2008 crisis having roots in the US mortgage market and the prospect of the collapse of the US banking system, the world flocked to dollars during the crisis, as shown below.

Most crises have been accompanied by a stronger dollar, proving that the dollar is the port in the storm foreign investors seek when economic confidence is lacking, and liquidity is paramount.

Excessive Government Spending

The book criticizes massive federal expenditures, particularly on social programs and military efforts, which create budget deficits, drive up inflation, and ultimately devalue the dollar. The book was written while Lyndon Johnson spent heavily on the Vietnam War and domestic programs. Again, Rickenbacker was correct in worrying about inflation, a big problem throughout the 1970s.

Despite ever-increasing government spending and an increasing debt-to-GDP ratio, the globalization of trade has expanded rapidly since his book was published. With it, foreigners' demand for dollars has been growing, and in mirror fashion, so is their need to invest the dollars, which helps us fund our deficits.

Even today, with “runaway” deficits making headlines daily, the dollar remains in the upper range of the last 35 years.

Dollar Devaluation In Context

Rickenbacker believed that easy money Federal Reserve policies, such as low interest rates and expanding the money supply, would fuel inflation that would erode the dollar’s purchasing power. He was right, as evidenced by comparing what a dollar buys today versus yesteryear. However, the argument provides little context.

For instance, in the 1950s, a hamburger (15 cents), fries (10 cents), and a Coke (10 cents) at McDonald's cost less than 50 cents. Today, the same meal could run nearly $10.

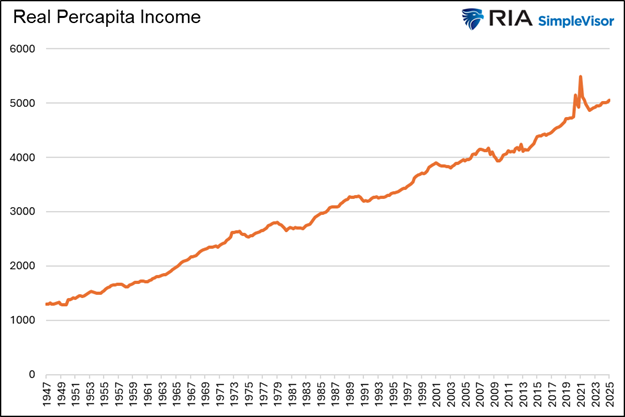

Although decades of inflation have drastically eroded the dollar's value, our standard of living has risen appreciably. To wit, the purchasing power of one dollar in 1947 has eroded to 7 cents. However, as shown below, inflation-adjusted incomes have risen fivefold since 1947. The dollar buys less, but our incomes buy more!

Trade and Balance of Payments Deficits

Rickenbacker points to persistent U.S. trade deficits and dollar outflows abroad, which weaken the currency’s global standing. He is correct that trade deficits have steadily increased, resulting in more dollars flowing abroad. However, more dollar outflows are a result of more demand for dollars. Furthermore, those dollars ultimately return to the US through investments and loans to the government and corporations. The larger the global economy, the greater the need for dollars, and the more dollars that need to be invested in the US economy.

Rickenbacker Was Right

The author’s concerns are valid and, in many cases, have proven true. However, the victim has not been the dollar. The victims are larger deficits, lower productivity growth, hollowing out of manufacturing, and a growing wealth divide, to name a few.

While these are big problems, they do not necessarily threaten the dollar's status. As we wrote in Four Reasons The Dollar Is Here To Stay:

The pundits will be right someday. The dollar’s death as the reserve currency will come, and some other nation’s currency, cryptocurrency, gold, shells, or something else will take its place. However, that day is not coming anytime soon. The four reasons we describe in the article leave the world with no alternative.

While China is rapidly growing its economy and global trade footprint, it lacks the rule of law and liquid capital markets to sustain a global currency. It’s difficult to see how a communist country can overcome those challenges.

The Euro is the most viable competitor. They have the rule of law, but their capital markets are not nearly liquid enough to facilitate global trade. They also lack the military might to force the usage of the Euro. Let us also remember its finances are in equally bad or even worse shape than the U.S. There is no reason to suspect the euro could overtake the dollar.

Bitcoin? Forget about it! The government will never relinquish its control over the currency because, with that, they lose control of the nation.

Summary

Had Rickenbacker’s Death of the Dollar book solely focused on monetary and fiscal imprudence and its negative implications for the country, he would have been proven a seer. Unfortunately, he was wrong to insist that the dollar would lose its status as the world’s reserve currency.

The graph below, courtesy of the Federal Reserve, shows how the dollar's usage in global transactions has been stable for the last two decades. The index calculation, as detailed at the bottom of the graphic, is based on the primary uses of currencies.

The post Death Of The Dollar: An Eternal Tale appeared first on RIA.

Illustration by The Epoch Times, Shutterstock

Illustration by The Epoch Times, Shutterstock An attendee inspects the new iPhone 16 Pro Max during event at the Apple headquarters in Cupertino, Calif., on Sept. 9, 2024. Experts warn of a rise in zero-click attacks—cyberattacks that compromise devices without any user interaction. Justin Sullivan/Getty Images

An attendee inspects the new iPhone 16 Pro Max during event at the Apple headquarters in Cupertino, Calif., on Sept. 9, 2024. Experts warn of a rise in zero-click attacks—cyberattacks that compromise devices without any user interaction. Justin Sullivan/Getty Images A woman checks the website of Israel-made Pegasus spyware at an office in Nicosia, Cyprus, on July 21, 2021. Pegasus has been tied to several high-profile international zero-click attacks in recent years. Mario Goldman/AFP via Getty Images

A woman checks the website of Israel-made Pegasus spyware at an office in Nicosia, Cyprus, on July 21, 2021. Pegasus has been tied to several high-profile international zero-click attacks in recent years. Mario Goldman/AFP via Getty Images