“What is perfection in love? Love your enemies in such a way that you would desire to make them your brothers … For so did He love, Who hanging on the Cross, said ‘Father, forgive them, for they know not what they do.’” (Luke 23:34)

Real Investment Advice

Is Buffett’s Cash Hoard A Market Warning?

Every year, investors anxiously await the release of Warren Buffett’s annual letter to see what the “Oracle of Omaha” says about the markets, the economy, and where he is placing his money.

“One of the longest-running traditions in modern finance is that every year, one Saturday morning in late February, the world’s financial class – from professionals to mere amateurs – sit down as they have for the past 65 or so years – for an hour and read the latest Berkshire annual letter written by Warren Buffett. In that letter, the man seen by many as the world’s greatest investor, wrote down his reflections, observations, aphorisms and other thoughts which are closely parsed and analyzed for insight into what he may do next, what he thinks of the current economy and market climate, or simply for insights into how to become a better investor.” – Tyler Durden

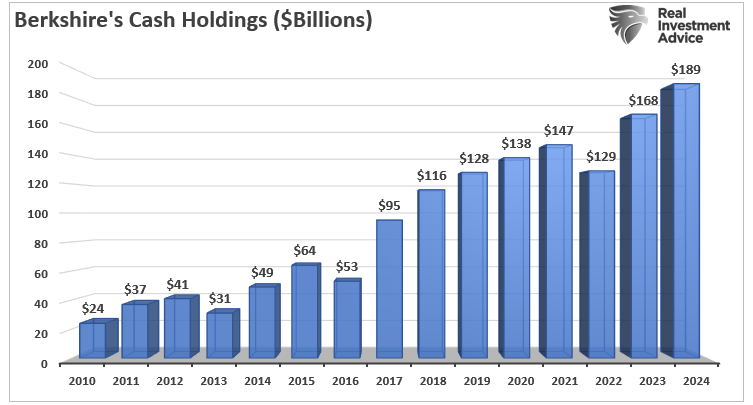

This year’s letter was no different, with various tidbits about the current market and investing environment for investors to digest. The one thing that got most of my attention was his comments about the recent surge in cash holdings. Buffett’s cash and short-term investments (read T-bills) exceed $189 billion as of Q1, 2024.

To put that into context, that $189 billion cash pile alone would make Berkshire the 58th-largest economy in the world, only slightly smaller than Hungary.

There are two critical messages regarding Buffett’s cash hoard. The first is that due to the size of Berkshire Hathaway, which is approaching a $1 Trillion market capitalization, acquisitions have to be of substantial size. As Warren previously noted:

“There remain only a handful of companies in this country capable of truly moving the needle at Berkshire, and they have been endlessly picked over by us and by others. Some we can value; some we can’t. And, if we can, they have to be attractively priced.”

Such was an essential statement. One of the most intelligent investors in history suggests that deploying Buffett’s cash hoard in meaningful size is difficult due to an inability to find reasonably priced acquisition targets. With a $189 war chest, there are plenty of companies that Berkshire could either acquire outright, use a stock/cash offering, or acquire a controlling stake in. However, given the rampant increase in stock prices and valuations over the last decade, they are not reasonably priced.

In other words:

“Price is what you pay, value is what you get.” – Warren Buffett

The Valuation Dilemma

The problem with the valuation dilemma is that historically, such has preceded market repricings.

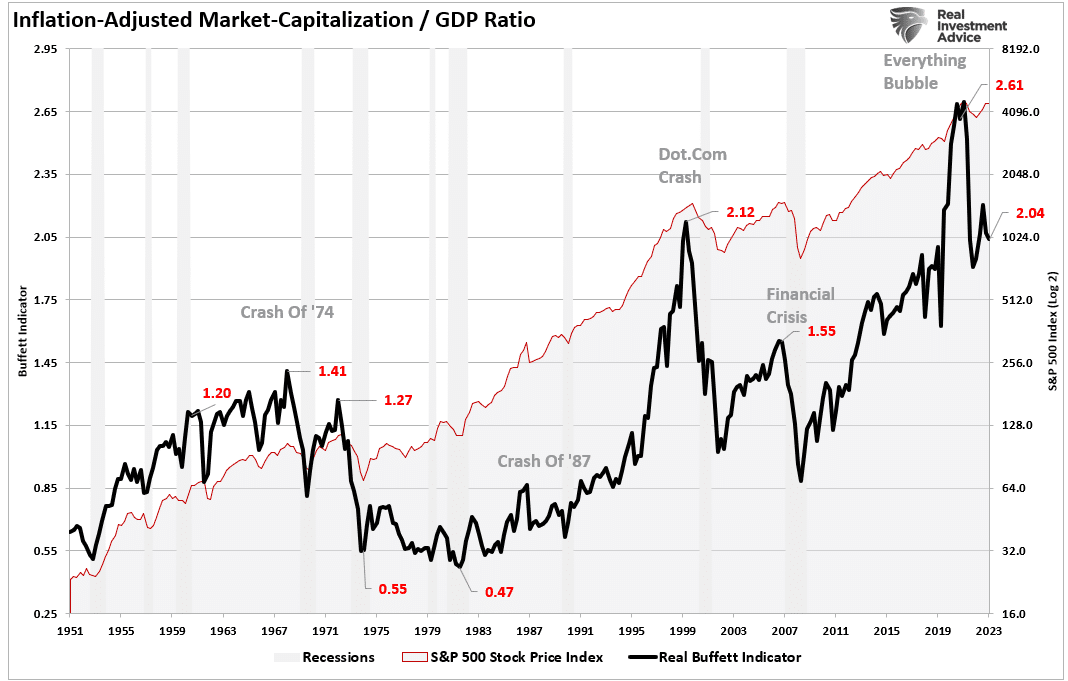

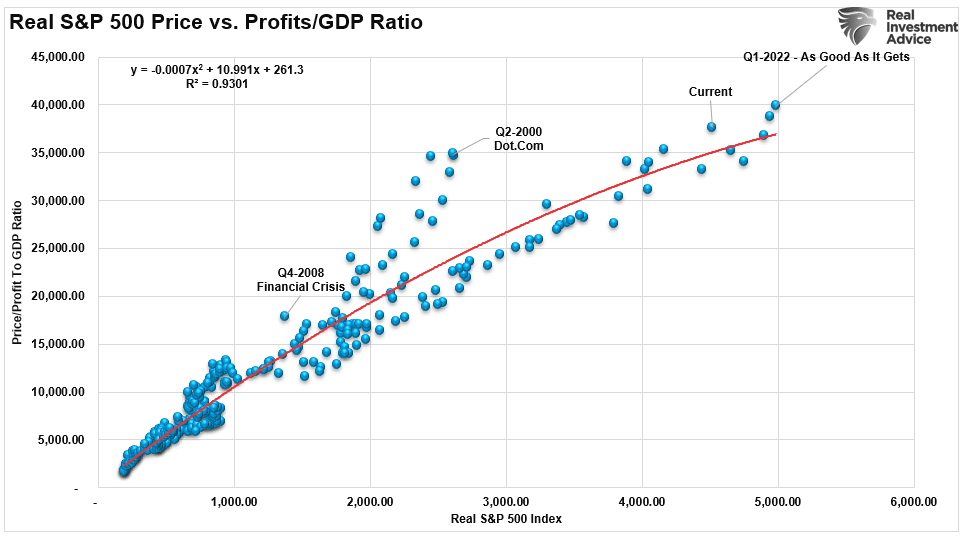

One of Warren Buffett’s favorite valuation measures is the market capitalization to GDP ratio. I have modified it slightly to use inflation-adjusted numbers. This measure is simple: stocks should not trade above the value of the economy. The reason is because economic activity provides revenues and earnings to businesses.

As discussed in “Stock Markets Are Detached From Everything,” the current environment is anything but opportunistic for a value investor like Warren Buffett. To wit:

“While stock prices can deviate from immediate activity, reversions to actual economic growth eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports. The market disconnect from underlying economic activity is due to psychology. Such is particularly the case over the last decade, as successive rounds of monetary interventions led investors to believe ‘this time is different.’”

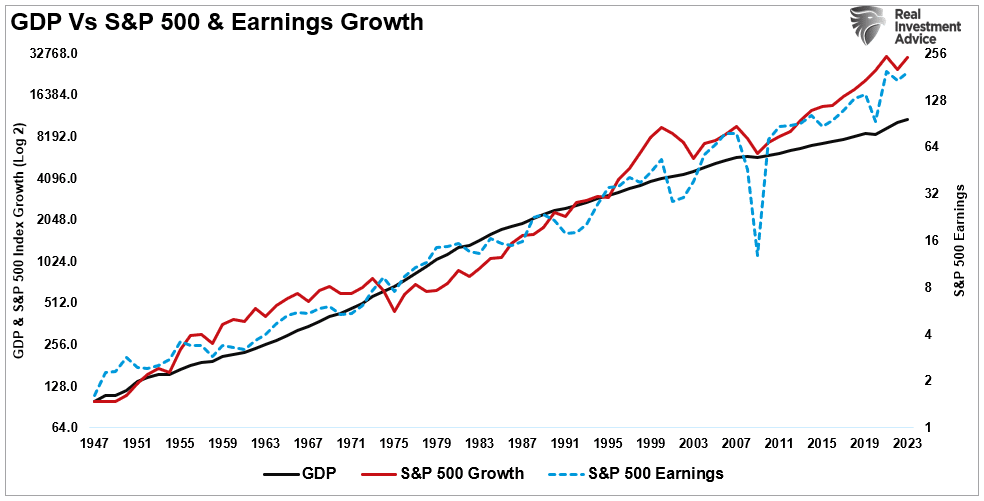

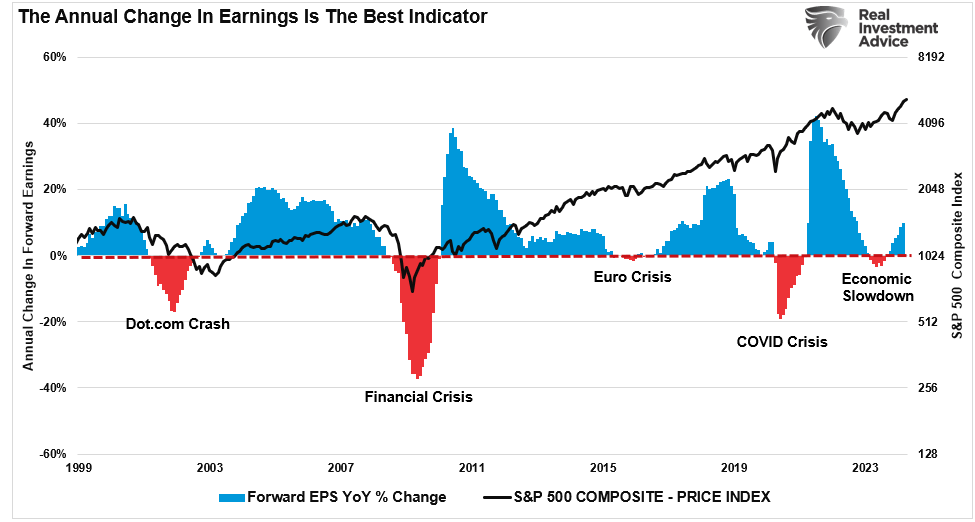

There is a correlation between economic activity and the rise and fall of equity prices. For example, in 2000 and again in 2008, corporate earnings contracted by 54% and 88%, respectively, as economic growth declined. Such was despite calls for never-ending earnings growth before both previous contractions.

As earnings disappointed, stock prices adjusted by nearly 50% to realign valuations with weaker-than-expected current earnings and slower future earnings growth. So, while stock markets are once again detached from reality, looking at past earnings contractions suggests such deviations are not sustainable.

With the current market capitalization to GDP ratio data outside the historical range as economic growth slows, you can understand Berkshire’s dilemma of deploying cash.

The risk of overpaying for assets comes down to sustaining current profitability.

Berkshire’s issue of finding “reasonably priced” acquisitions is not just one of being overly picky about opportunities. After more than a decade of monetary infusions and zero interest rates, most companies are priced well beyond what economic dynamics can support.

The second message from Buffett’s cash hoard was more of a warning.

Buffett’s Cash Looking For A Crash?

“Occasionally, markets and/or the economy will cause stocks and bonds of some large and fundamentally sound businesses to be strikingly mispriced. Indeed, markets can – and will – unpredictably seize up or vanish as they did for four months in 1914 and a few days in 2001. If you believe American investors are now more stable than in the past, think back to September 2008. Speed of communication and the wonders of technology facilitates instant worldwide paralysis, and we have come a long way since smoke signals. Such instant panics won’t happen often – but they will happen.

Berkshire’s ability to immediately respond to market seizures with both huge sums and certainty of performance may offer us an occasional large-scale opportunity. Though the stock market is massively larger than it was in our early years, today’s active participants are neither more emotionally stable nor better taught than when I was in school. For whatever reasons, markets now exhibit far more casino-like behavior than when I was young. The casino now resides in many homes and daily tempts the occupants.

One investment rule at Berkshire has not and will not change: Never risk permanent loss of capital. Thanks to the American tailwind and the power of compound interest, the arena in which we operate has been – and will be – rewarding if you make a couple of good decisions during a lifetime and avoid serious mistakes.” – Warren Buffett

In other words, he holds such high cash levels to take advantage of market dislocations. Such is what happened in 2008 when the prestigious “white shoe” investment firm of Goldman Sachs came begging with “hat in hand” for a bailout to avoid bankruptcy. Buffett was glad to oblige by providing a massive infusion of capital at lucrative terms. During a crisis, those who “have the gold make the rules.”

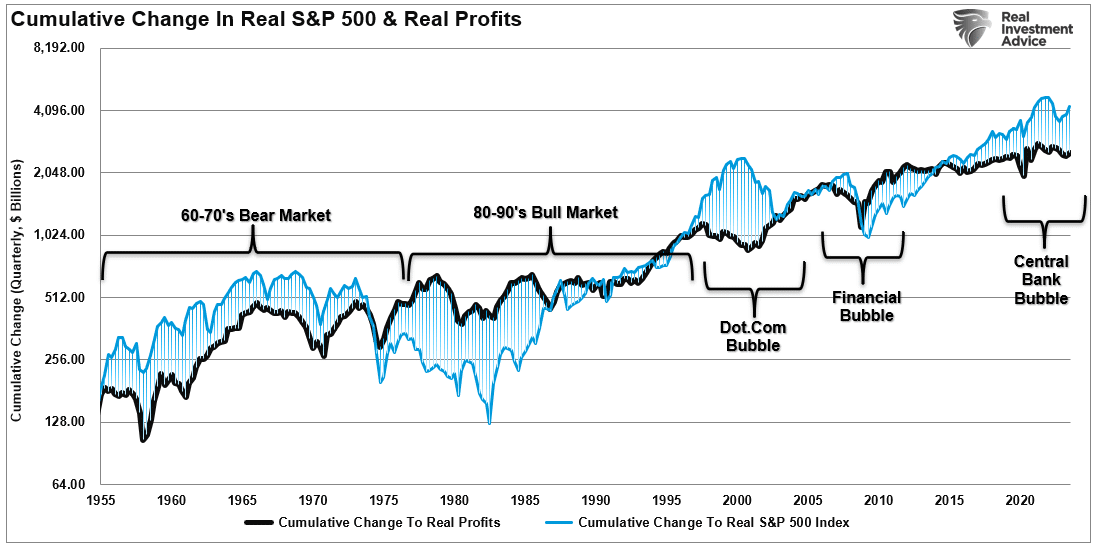

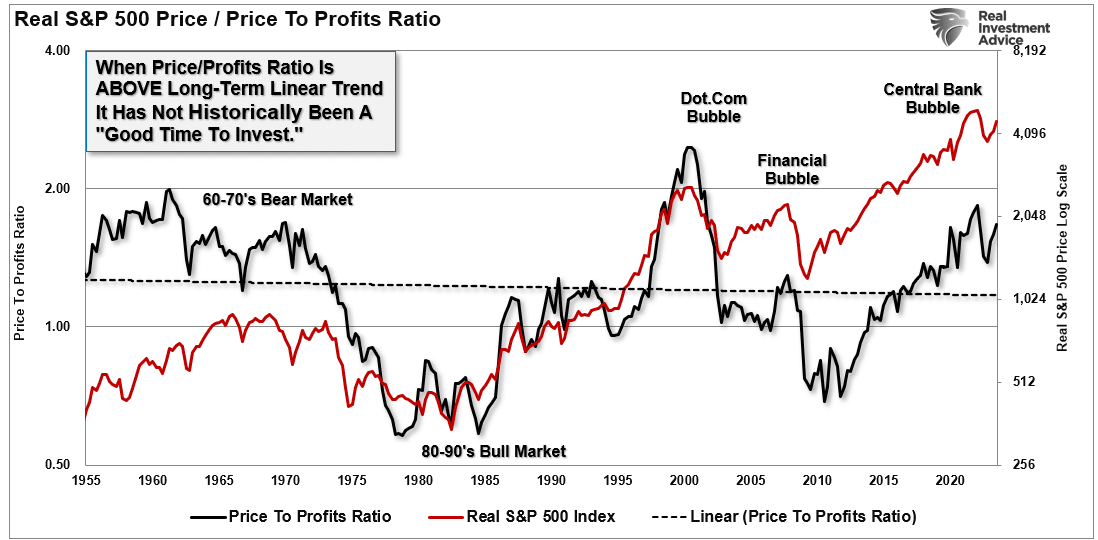

Is there such an opportunity coming in the future? The answer is most likely yes. If we examine corporate profits as they relate to economic growth, we find another measure of excess. The chart below measures the cumulative change in the S&P 500 index compared to corporate profits. Again, when investors pay more than $1 for $1 worth of profits, those excesses are eventually reversed. The current deviation of the market from underlying profitability suggests that eventual reversion will be pretty unkind to investors.

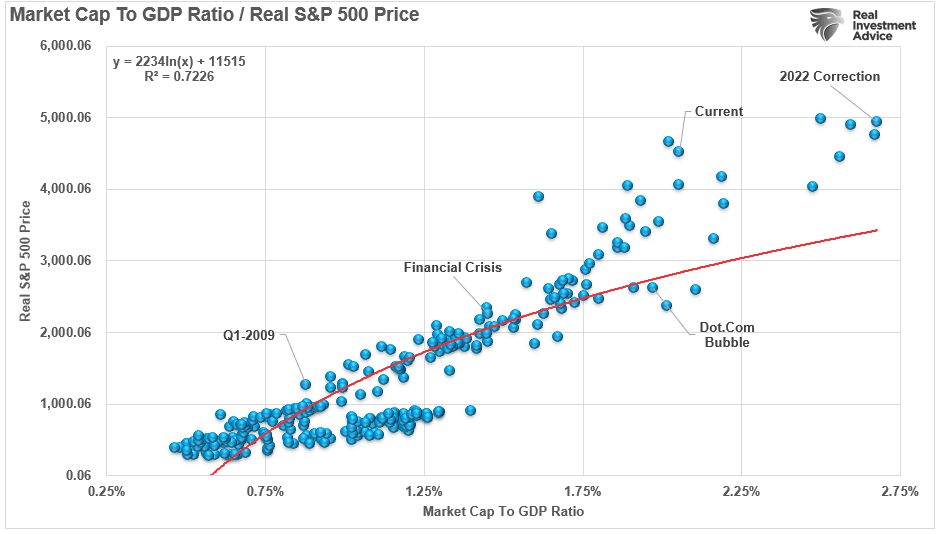

The correlation is more evident in the market versus the price-to-corporate profits ratio. Again, since corporate profits are ultimately a function of economic growth, the correlation is not unexpected. Hence, neither should the impending reversion in both series. Currently, that ratio is approaching levels that preceded more significant market reversions to realign the markets to profitability.

As noted, the high correlation is unsurprising. Investors should expect an eventual reversal with the market on the more extreme end of the valuation spectrum. However, those reversals can take much longer to occur than logic would assume.

Investors believe the deviation between fundamentals and fantasy doesn’t matter as long as the Fed supports asset prices. Such a point remains challenging to argue.

However, as is always the case, the reversion of excesses will occur. Buffett’s cash hoard suggests that he realizes that such a reversion is not unprecedented. More importantly, he wants to capitalize on it when it occurs.

The post Is Buffett’s Cash Hoard A Market Warning? appeared first on RIA.

Stimulus Today Costs Dearly Tomorrow

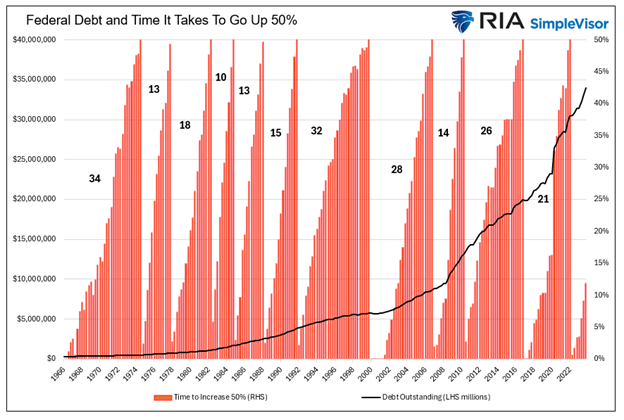

Since the pandemic-related bazooka of fiscal stimulus, the outstanding Federal debt has risen appreciably. In nominal dollar terms, the recent debt surge is mindboggling. However, the increase is on par with the government’s negligent ways over the last fifty years.

The red bars show the percentage increase in debt starting in 1966. The bars reset to zero every time they hit 50%. The numbers to the left of each series of bars correspond to the number of quarters it took for every 50% increase.

Over the last sixteen quarters, 2020 through 2023, the outstanding federal debt has risen by 46%. Of the 11 times the debt has increased by 50% since 1966, five occurred over 15 quarters or less.

That said, the repercussions of relying on stimulus for economic growth and growing debt faster than the ability to pay for it have significant economic consequences. The recent surge in debt will only further handicap our economy and prosperity in the future.

There are predominantly two ways our growing debt load negatively impacts economic growth, as we will share.

#1 Manipulated Interest Rates Cripple Capitalism

Growing debt faster than one’s income is a Ponzi scheme. No matter how politicians sugarcoat fiscal stimulus, there are no two ways around such a characterization. Individuals and corporations that run such a scheme ultimately end up bankrupt. The same holds for governments, but they tend to have much longer runways.

The Federal Reserve allows the government to perpetuate its Ponzi scheme. The Fed keeps borrowing costs lower than they should be through lower-than-market interest rates and asset purchases.

Not only is the growing ratio of debt to income problematic, but it is also a sure sign that the debt in aggregate is used for unproductive purposes. In other words, the debt costs more than the financial benefits it provides. If it were productive debt, income or GDP would rise more than the debt.

In the long run, unproductive debt reduces a nation’s productivity, aka economic potential.

Negative Real Rates And QE

A lender or investor should never accept a yield below the inflation rate. If they do, the loan or investment will reduce their purchasing power.

Regardless of what should happen in an economics classroom, the Fed has forced a negative real rate regime upon lenders and investors for the better part of the last 20+ years. The graph below shows the real Fed Funds rate (black). This is Fed Funds less CPI. The gray area shows the percentage of time over running five-year periods in which real Fed Funds were negative. Negative real Fed Funds have become the rule, not the exception.

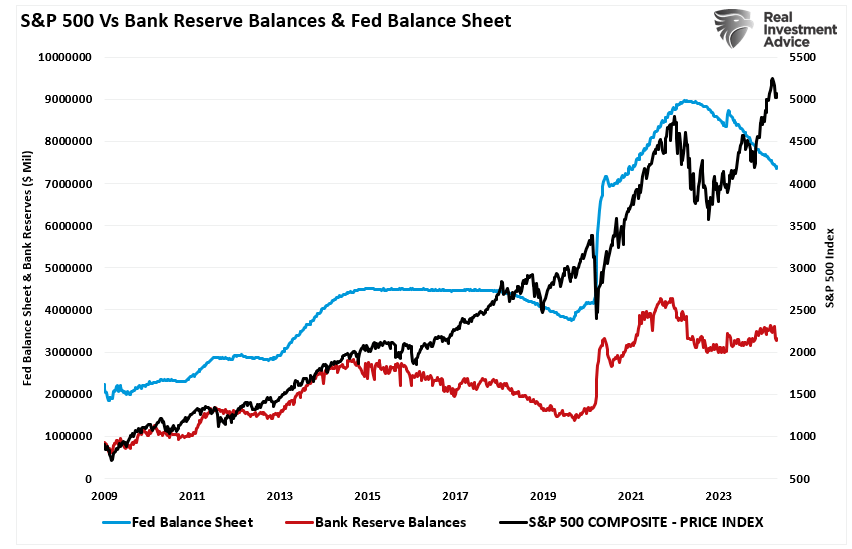

Starting in 2008, with QE, the Fed began using its balance sheet to manipulate interest rates further. Currently, the Fed holds $8 trillion in Treasury and mortgage-backed securities. Their Treasury holdings account for almost 25% of all Treasury securities outstanding to the public.

By reducing the supply of bonds on the market, they effectively lower interest rates below where the free market would price them. This makes fiscal stimulus more appetizing for politicians and, by default, encourages even greater federal debt loads.

Like the Fed’s negative real rate interest rate policy, QE also reduces interest rates, allowing for more unproductive federal and private sector debt.

#2 Negative Multiplier

As we note, debt increasing faster than economic growth proves that borrowing and spending are unproductive. Unproductive government debt or private sector debt also results in a negative economic multiplier. Essentially, the ultimate expense of the debt outstrips its benefits over the long run.

Economists define the multiplier effect as the change in income divided by the change in spending. Over an extended period, if the change in spending is more significant than the change in income, the effect of said spending is negative. Replace GDP for income and government debt for spending to compute the government’s spending multiplier.

Multiplier = Change Income / Change Spending

Government Multiplier = Change GDP / Change Debt Outstanding

To help appreciate the negative multiplier, let’s consider the two rounds of stimulus checks sent to the public during the pandemic. Consumers and businesses spent a large percentage of the funds on goods or services that no longer provide economic benefit. The initial result of the direct stimulus was a massive boost to economic activity. Three to four years later, the economic growth spurt is finished, and the debt and its annual interest costs remain. The interest on the debt is capital that will not be put to productive use.

Yesterday’s tailwind is slowly becoming tomorrow’s headwind.

There are other economic considerations as well.

Ricardian Equivalence

This economic theory states that when individuals anticipate tax increases to finance current and future government spending, they increase their savings to offset the expected tax burden. Therefore, any increase in government spending financed by debt may not stimulate consumption and investment, potentially resulting in a negative multiplier effect.

Crowding Out

High levels of government borrowing can lead to crowding out of private investment. This occurs when government borrowing forces higher interest rates, making it more expensive for businesses and individuals to borrow for investment. Further, as banks are asked to hold more government debt, they have less ability to lend to the private sector. Consequently, private investment, likely to be more productive than government spending, may decline.

Capitalism Is Eroding

The graph below shows why capitalism matters. It plots the Heritage Foundation’s Index of Economic Freedom, a measure of capitalism, versus the average family wealth for 137 countries. As shown, economic freedom and wealth have a strong positive correlation.

With that relationship in mind, government spending is a key component of the economic freedom index. Massive government stimulus spending reduces our index score. Further, while not a part of the score, manipulation of free market interest rates also detracts from the benefits of capitalism. As our index score falls, denoting the retreat from capitalism, so does our wealth.

Summary

Nothing is free, it’s just a question of how it’s paid for. While the government spends like there is no tomorrow and the Fed does everything in its power to help them, we must understand that the longer-term consequences of their actions are weaker economic growth and growing wealth disparity, as we discuss in Fed Policies Turn The Wealth Gap Into A Chasm. To wit:

QE may have served as an emergency way to add bank reserves to the system and boost confidence. However, its continued use, even during economic prosperity periods, only makes the wealth gap wider.

We should take the matter personally because, as we have shown, there is a strong link between government borrowing and our prosperity. While the cost of deficits may not be higher taxes, it does show up invisibly in lesser wages and wealth than we otherwise could attain. Any wonder why millennials are on track to be the first generation to fail to exceed their parents in income?

The post Stimulus Today Costs Dearly Tomorrow appeared first on RIA.

Moving Average Crossovers Suggest The Bull Is Back

While there is much debate over whether another bear market is imminent, weekly moving average crossovers suggest a different outcome for now. There are many current concerns, from geopolitical risk to still inverted yield curves, slowing economic growth, high interest rates, and inflation. Yet, despite those concerns, markets are flirting with all-time highs.

While 5% money market yields are certainly enticing, investors often need to step back from the “doomsday” dripping headlines. Given that one of our behavioral investing traits is “loss avoidance,” it is easy to talk ourselves into an overly cautionary position. The mistake is that while alleviating our short-term emotional concerns, it can lead to a significant wealth impairment in the long term.

Therefore, it is often worth digging ourselves out of the media headlines and focusing on what the market tells us. After all, the stock market has a long track record of leading the economy by 6-9 months. To explain this, start with the chart of the S&P 500 index below and notice those interesting blue dots.

What Did The Market Know?

Yes, those market dots represent stock market peaks. However, why did the stock market top at those particular points?

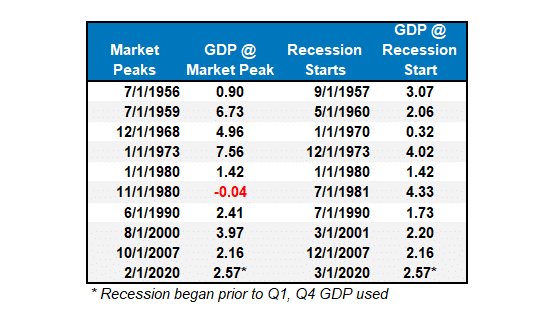

Let’s take a look at the data below of real (inflation-adjusted) economic growth rates:

Each of the dates above shows the economy’s growth rate immediately before the onset of a recession. The table above notes that in 7 of the last 10 recessions, real GDP growth was 2% or above. In other words, according to the media, there was NO indication of a recession.

But the next month, one began.

With that understanding,let’ss return to those”“interesting blue dot”” in the S&P 500 chart above. Each dot represents the market peak before the onset of a recession. The S&P 500 peaked and turned lower in nine of ten instances before a recession was recognized, anywhere from 6 to 16 months later.

The crucial point is that the stock market was signaling a coming recession in the months ahead, but the economic data didn’t reflect it. (The only exception was 1980 when they coincided in the same month.) The table below shows the date of the market peak and real GDP versus the start of the recession and GDP growth at that time.

The problem for investors is waiting for the data to catch up.

Moving Average Signals

Understanding that the market tends to lead the economy by six months or more, we can use longer-term market signals to help us navigate the risk of a recessionary downturn.

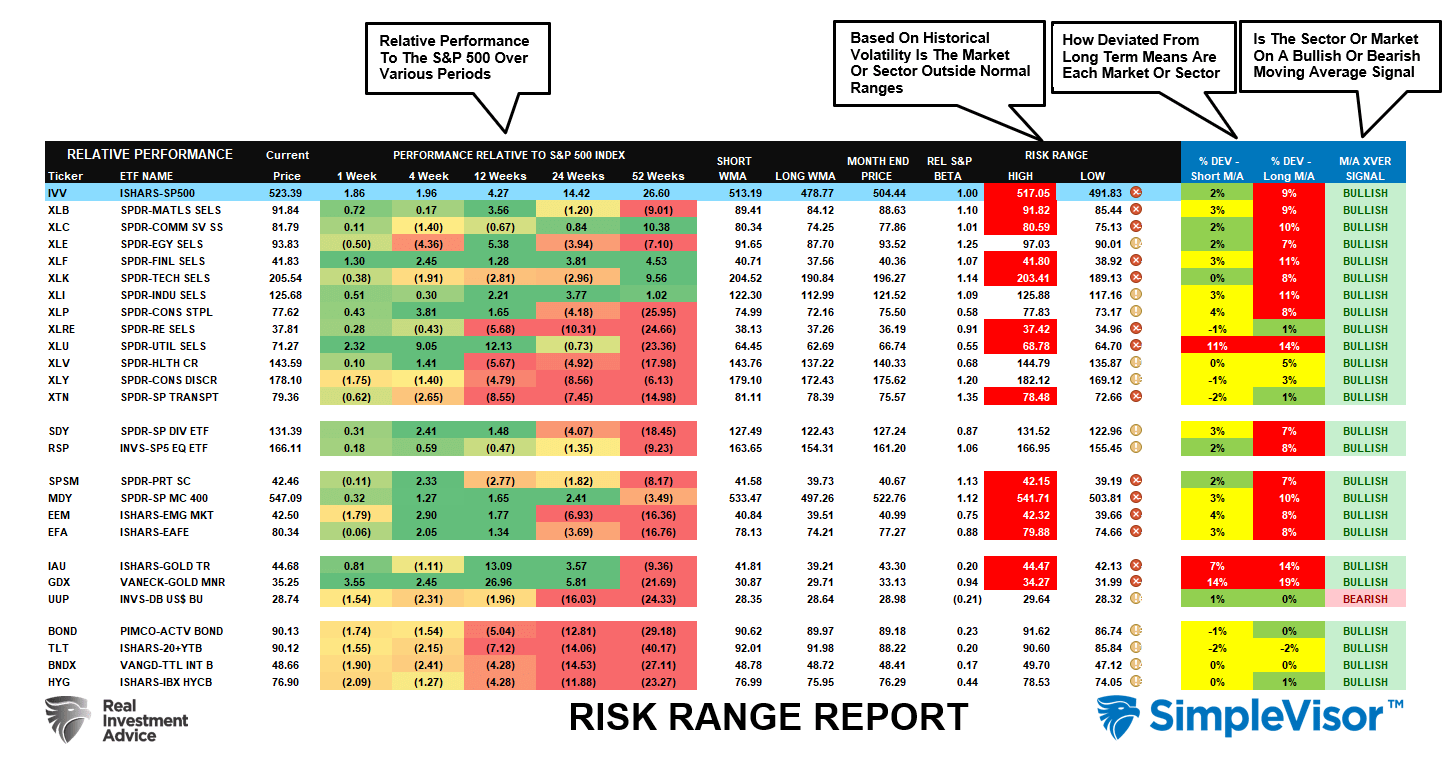

We have produced a weekly”“risk range repor”” in the Bull Bear Report for several years. That report contains several measures of analysis, as shown below.

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVE”” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the”“bet”” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

For this analysis, we will focus on the far right column. Every major market and sector (except for the U.S. dollar) is currently on a bullish moving average crossover. Given this is weekly data, it is slower to move, which tends to provide better signals for both increasing and reducing portfolio risk.

A Simple Chart

However, are these signals useful in safeguarding against the onset of a recession or just a more protracted market downturn like the one we saw in 2022? The chart below uses a simple weekly moving average crossover analysis to determine where investors should consider increasing or reducing risk to equity exposure.

In 2000 and 2008, the moving average crossover signal warned investors that a recessionary onset was coming 9 and 12 months ahead of actual recognition. The weekly moving average signals also triggered a sell signal in early 2022 ahead of the ~20 decline, although the NBER has not recognized a recession yet.

Notably, these signals are not always perfect. The drawdown was so swift in 2020 during the pandemic shutdown that the signals to reduce and increase exposure coincided with the market. However, paying attention to these moving average signals over the longer term can provide investors with a valuable roadmap to follow.

Bullish Buy Signals Tend To Be Correct

Returning to the”“risk range repor”” above, a review of late 2021 warned our readers that market deterioration was increasing. The report below is from the October 6th, 2022, Bull Bear Report:

“The selling pressure continued this week, taking almost every sector and market into double-digit deviations below long-term weekly moving averages. Such extremes are not sustainable, and when all markets and sectors are this oversold, a reflexive rally becomes highly probable.”

The table below shows that almost every sector and market had bearish moving average sell signals triggered. At the time, however, media headlines were filled with “death of the dollar,” recession warnings, and bear market alerts. However, such negative extremes are often coincident with market bottoms.

Furthermore, investor sentiment and allocations were likewise extremely negative.

Of course, as we now know in hindsight, October 2022 marked the bottom of the market, and the recession predictions have faded into the midst.

The market has recovered since then, and those bearish moving average sell signals have reversed to bullish buy signals. As discussed in this past weekend’s Bull Bear Report, while the market is overbought, and consolidation or correction is likely, with every major equity and bond market on bullish buy signals, the market is not predicting the onset of a recession.

Furthermore, investor sentiment and allocations are also bullish, which supports higher prices.

Corrections Tend To Opportunities

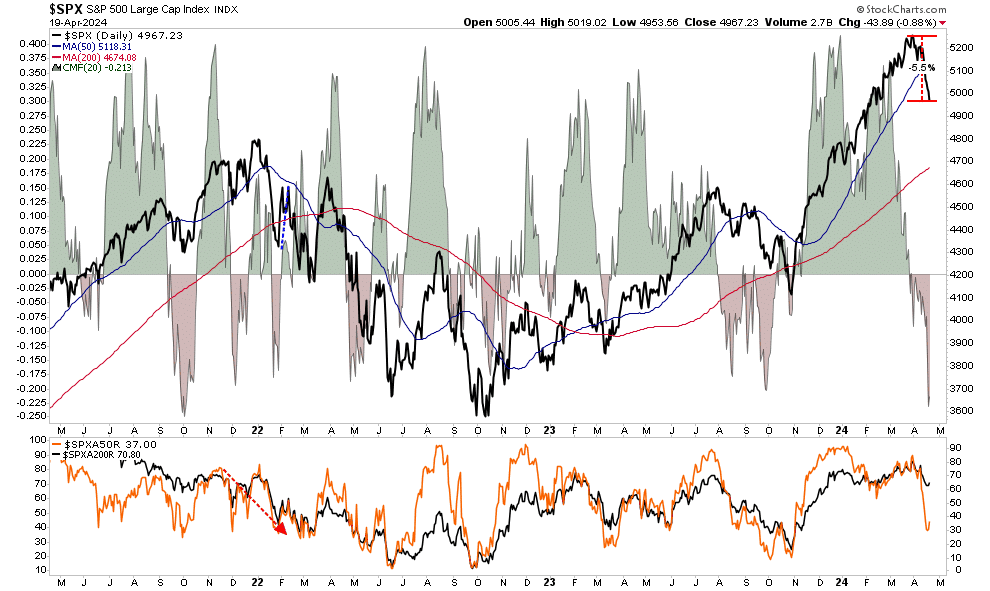

Does this mean that markets will be devoid of any short-term corrections? Of course not. We just experienced a 5.5% correction in April. Furthermore, corrections during market advances happen every year and tend to be opportunities to increase equity exposure as needed.

While some unexpected, exogenous events could send markets reeling, the market has a long history of anticipating recessionary onsets well before economists and the mainstream media recognize them.

With the plethora of “armchair commentators” pointing at every piece of data as an indicator of economic doom to get more clicks and views, we suggest sitting back and paying attention to the markets. Given that the market represents a vast group of individuals analyzing every possible data point, the signals the market provides tend to be a more reliable signal to follow.

When those bullish weekly moving average buy signals begin to reverse, with one following another, we will know it’s time to become increasingly more conscious of risk.

As of now, the market suggests that sitting in cash may be a mistake when it comes to reaching retirement goals.

The post Moving Average Crossovers Suggest The Bull Is Back appeared first on RIA.

The Investment “Holy Grail” Doesn’t Exist

When it comes to the financial markets, investors have a litany of investment vehicles to choose from. The choices are nearly unlimited, from brokered certificates of deposit to complex derivative instruments. Of course, investment vehicles’ proliferation comes from investors’ demand for everything from excess benchmark returns to income generation to downside protection.

Of course, every investor wants “all the upside, with none of the downside.” While there are vehicles, like indexed annuities, that can provide no downside risk, they cap the upside return. If you buy an index fund, you can get “all the upside” and “all the risk.”

However, an email from a reader last week got me thinking about the perfect “investment vehicle” and the search for the “holy grail” of investing.

“My wife and I are looking for a place to position some of our ’emergency funds’ for a better return. Our requirements are pretty simplistic:

- Guarantee at least a 4% rate of return.

- Allow me to withdraw cash without penalty when needed.

- Reinvest all income

- If bond yields decline as expected, the value of the investment increases.

At this point, I was confident in just suggesting purchasing a 10-year Treasury bond. At current rates, the investment would yield greater than 4% and guarantee the principal. If yields decline, the bond rises in price, reinvestment of income is an option, and the investment is highly liquid.

Theoretically, this would be the “perfect investment” vehicle for their needs. I said “theoretically” because they added one more requirement just as I was about to spout off my terrific idea.

“Oh, and one more thing, the dollar value of the account must remain stable at all times.”

And that, as they say, quickly ended the “perfect investment” vehicle for their needs.

Why did the addition of “price stability” make their request impossible?

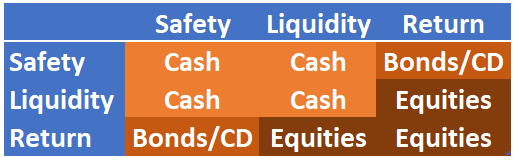

The 3-Components Of All Investments

In portfolio management, you can ONLY have two of three components of any investment or asset class:

- Safety – The return of principal without loss due to price change or fees

- Liquidity – Immediately accessible without penalties or fees

- Return – Appreciation in the price of the investment

The table below is the matrix of your options.

The takeaway is that cash is the only asset class that provides safety and liquidity. Safety comes at the cost of return. Equities are liquid and provide returns but can suffer a significant loss of principal. Bonds can offer returns through income and safety if held to maturity. But in exchange for that safety, investors must forego liquidity.

In other words, no investment can provide all three factors simultaneously. While the table above uses only Equities, Bonds, and Cash, those three factors apply to any investment vehicle you may consider.

- Fixed Annuities (Indexed) – safety and return, no liquidity.

- Certificates of Deposit – safety and return, no liquidity.

- ETFs – liquidity and return, no safety.

- Mutual Funds – liquidity and return, no safety.

- Real Estate – safety and return, no liquidity.

- Traded REITs – liquidity and return, no safety.

- Commodities – liquidity and return, no safety.

- Gold – liquidity and return, no safety.

You get the idea.

Let’s revisit our email question.

While I initially focused on the cash requirements, these were also funds set aside for an “emergency.” In other words, these funds must be readily available when an unexpected event arises. Since “unexpected events” tend to happen at the worst possible time, these funds should never be put at risk. The need for “safety” and “liquidity” eliminates the third factor: Return.

No matter what investment vehicle you choose, you can only have two of the three components. Such is an essential and often overlooked consideration when determining portfolio construction and allocation.

8-Reasons To Focus On Liquidity

Liquidity is the most essential factor in making any investment. Without liquidity, I can not invest. Therefore, liquidity should always remain a high priority when managing your portfolio.

I learned a long time ago that while a “rising tide lifts all boats,” eventually, the “tide recedes.” Over the years, I made a straightforward adjustment to my portfolio management, which has served me well. When risks begin to outweigh the potential for reward, I raise cash.

The great thing about holding extra cash is that if I’m wrong, I simply make the proper adjustments to increase the risk in my portfolios. However, if I am right, I protect investment capital from destruction and spend far less time ‘getting back to even.’ Despite media commentary to the contrary, regaining losses is not an investment strategy.

Here are 8-reasons why you should focus on liquidity first:

1) We are speculators, not investors. We buy pieces of paper at one price with hopes of selling at a higher price. Such is speculation in its purest form. When risk outweighs rewards, cash is a good option.

2) 80% of stocks move in the direction of the market. If the market is falling, regardless of the fundamentals, the majority of stocks will decline also.

3) The best traders understand the value of cash. From Jesse Livermore to Gerald Loeb, each believed in “buying low and selling high.” If you “sell high,” you have raised cash to “buy low.”

4) Roughly 90% of what we think about investing is wrong. Two 50% declines since 2000 should have taught us to respect investment risks.

5) 80% of individual traders lose money over ANY 10-year period. Why? Investor psychology, emotional biases, lack of capital, etc. Repeated studies by Dalbar prove this.

6) Raising cash is often a better hedge than shorting. While shorting the market, or a position, to hedge risk in a portfolio is reasonable, it also merely transfers the “risk of being wrong” from one side of the ledger to the other. Cash protects capital and eliminates risk.

7) You can’t “buy low” if you don’t have anything to “buy with.” While the media chastises individuals for holding cash, it should be somewhat evident that without cash you can’t take advantage of opportunities.

8) Cash protects against forced liquidations. One of the biggest problems for Americans is a lack of cash to meet emergencies. Having a cash cushion allows for handling life’s “curve-balls,” without being forced to liquidate retirement plans.Layoffs, employment changes, etc. are economically driven and tend to occur with downturns that coincide with market losses. Having cash allows you to weather the storms.

Importantly, I want to stress that I am not talking about being 100% in cash.

I suggest that holding higher cash levels during periods of uncertainty provides both stability and opportunity.

With the political, fundamental, and economic backdrop becoming much more hostile toward investors in the intermediate term, understanding the value of cash as a “hedge” against loss becomes much more critical.

Chasing yield at any cost has typically not ended well for most.

Of course, since Wall Street does not make fees on investors holding cash, maybe there is another reason they are so adamant that you remain invested all the time.

The post The Investment “Holy Grail” Doesn’t Exist appeared first on RIA.

Finding The Next Apple Using Buffetts Logic

On the heels of Apple’s latest earnings report, the Wall Street Journal shared an article discussing how Apple became such an oversized investment of Warren Buffett’s company, Berkshire Hathaway. Given their success with Apple shares we think it is worth understanding the logic that drove Buffett to accumulate such a large position in Apple.

Unbeknownst to most, Todd Combs, a member of the Berkshire portfolio management team, is responsible for bringing Apple to Buffett’s attention. However, not all credit goes to Combs. Buffett presented Combs with a challenge that ultimately highlighted Apple’s value proposition. With this same challenge, we will take a stab at finding the next Apple.

The inspiration for our challenge and a few quotes in this article come from a Wall Street Journal article entitled Apple is Buffett’s Best Investment.

Berkshires Massive Stake Of Apple

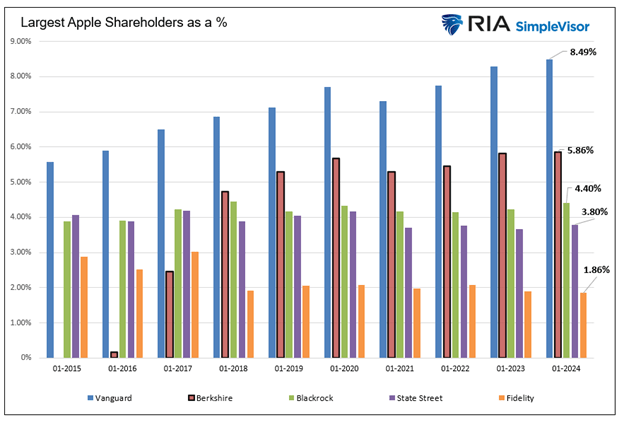

Before finding the next Apple stock, it’s worth visualizing how Berkshire’s investment in Apple has grown over time as a percentage of Berkshire Hathaway and of Apple’s total shares outstanding.

The bar graph below compares Berkshire’s percentage ownership of Apple to that of the four largest mutual fund and ETF complexes. Berkshire had no position in Apple in 2015 and now holds over 5% of the company. Only Vanguard has a more significant position.

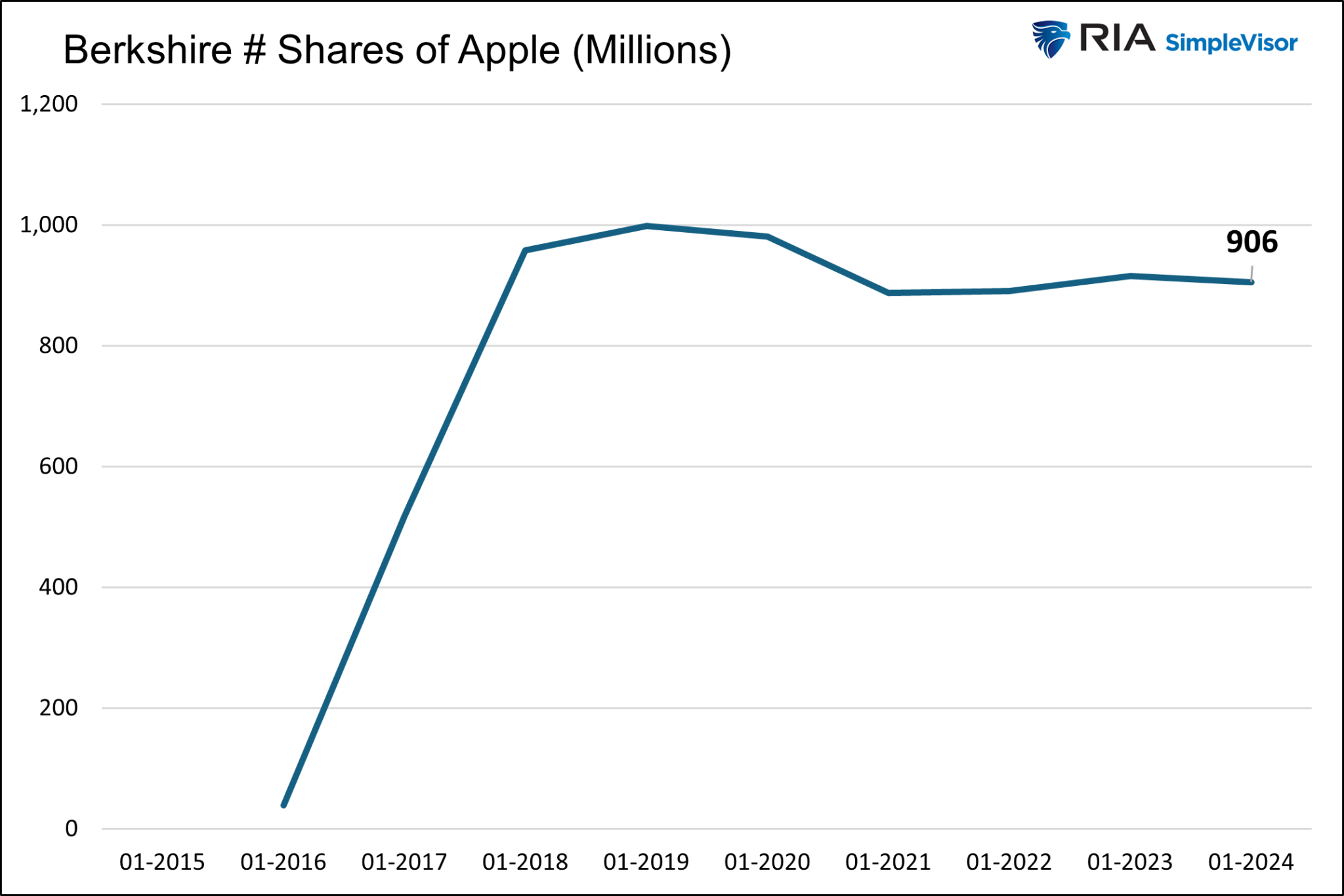

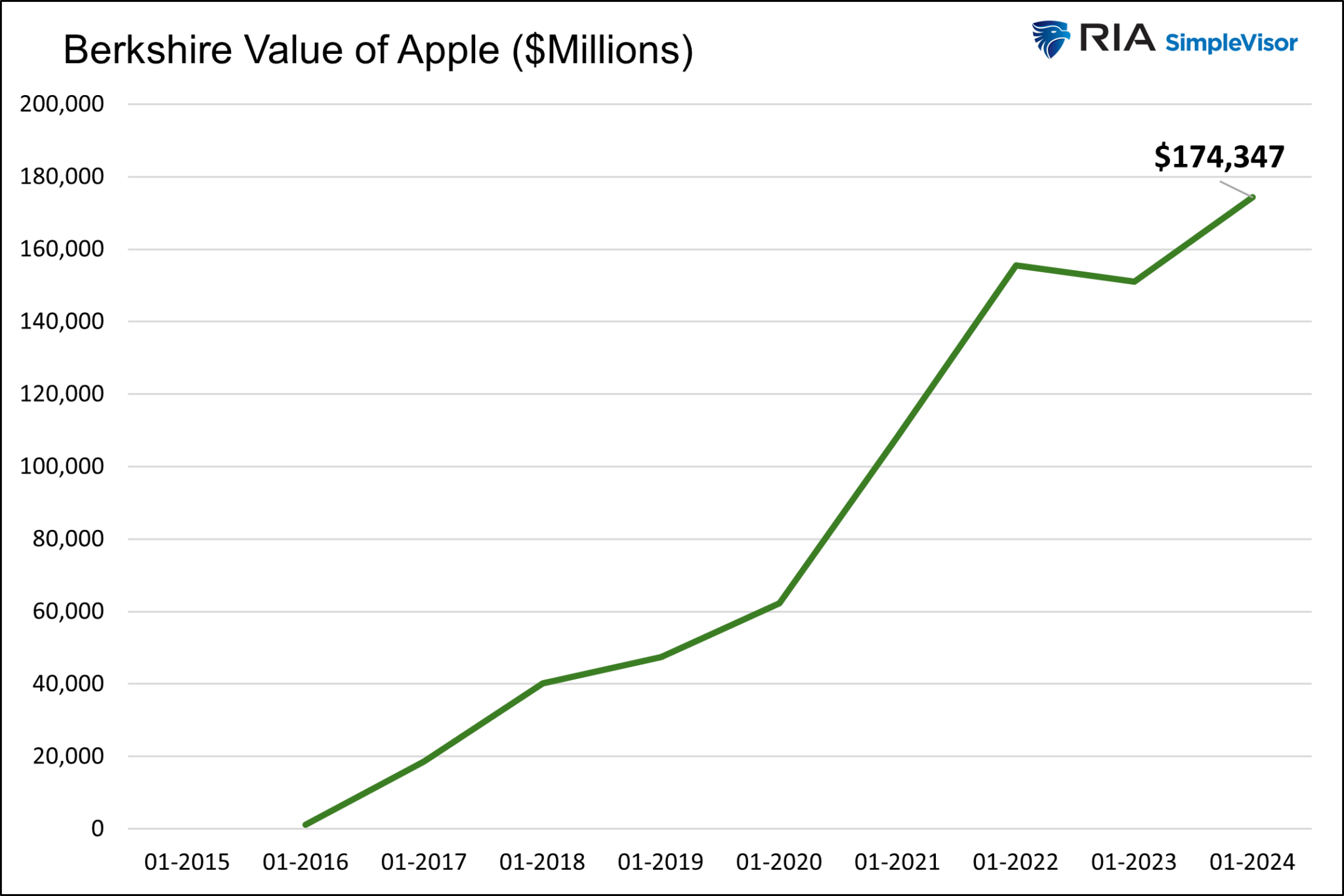

The following graphs plot the surge in the number of shares owned by Berkshire and the value of its shares.

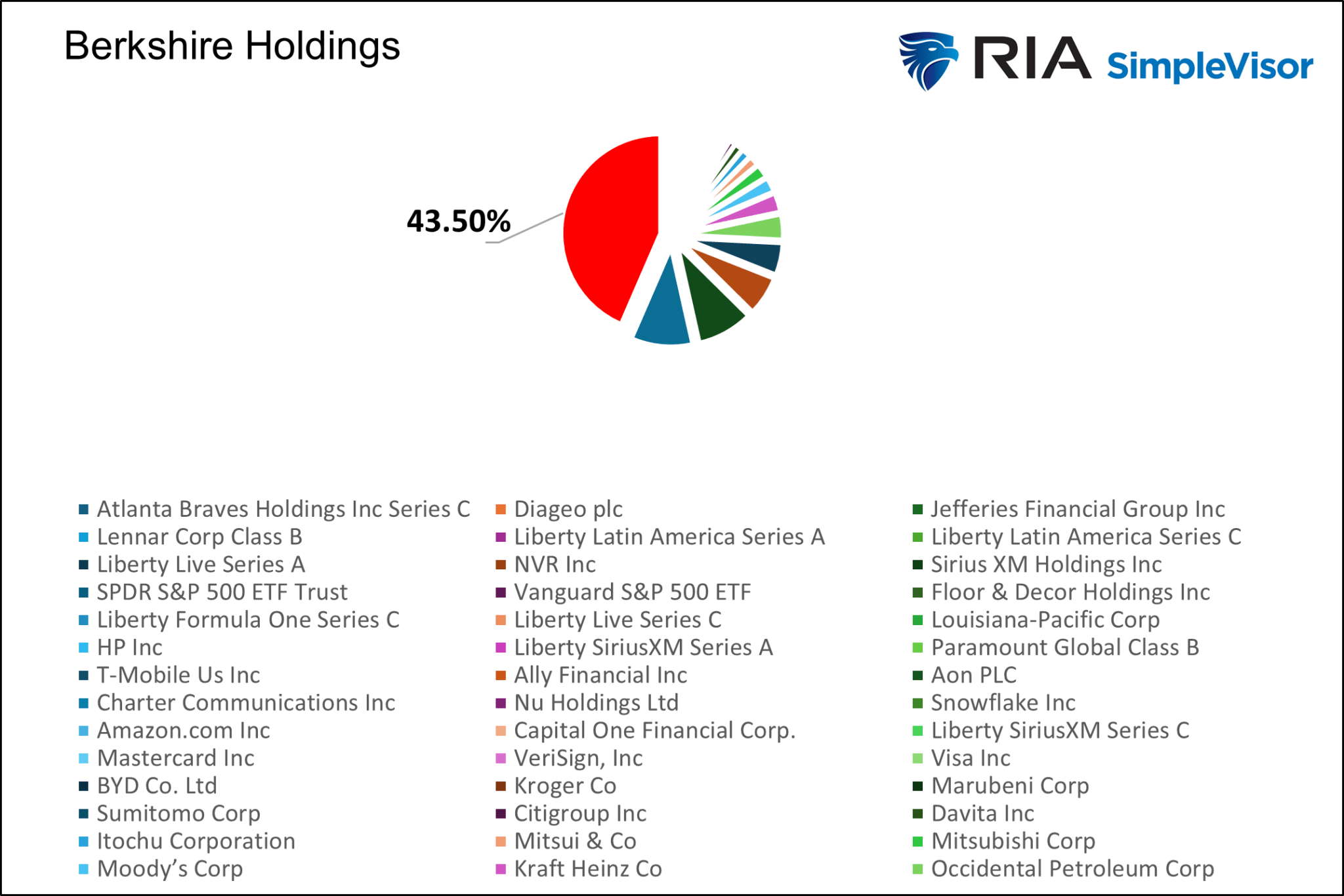

The pie chart below shows that Apple comprises almost half of Berkshire’s portfolio. The next largest holding is Bank of America at 10%.

Buffett Doesn’t Like Tech

Ironically, when Berkshire started buying Apple shares, Warren Buffett had an aversion to technology stocks. When asked why, he said he didn’t invest in companies he didn’t understand. He now admits that was a mistake.

While it may have been a mistake not to buy more technology companies in the mid twenty-teens, Buffett was able to appreciate what Apple truly was. While it is classified as and widely considered a technology company, Buffett got his head around Apple by likening it to a consumer goods company. Per the aforementioned Wall Street Journal article:

Considering the stock, though, Buffett began to see it as a consumer-goods company with enviable, latent pricing power, rather than as a tech or an electronic-device maker, according to people who have spoken to him. The loyalty consumers had for Apple products, especially the iPhone, suggested to Buffett that they would be willing to pay much more for upgraded versions of the phone in the years ahead, a sure way to boost profits.

Todd Combs- The Unknown Mastermind

The Wall Street Journal article introduces Todd Combs, one of Berkshire Hathaway’s lesser-known portfolio managers. According to the article, around 2016, Buffett challenged Combs to find a stock that met specific criteria.

Among the stocks Combs found meeting the fundamental criteria and large enough for Berkshire to purchase was Apple. The rest is history. Since they started accumulating Apple in 2015, it has gained 650%, more than four times the S&P 500 over the same period.

Given Combs’ success, we thought it would be interesting to use the logic Buffett challenged Combs with and produce a similar scan. Let’s see if we can find the next Apple.

Buffett’s Logic

The following paragraph from the WSJ article is the logic Buffett imparted to Combs, leading to their ownership of Apple.

This time, Buffett asked Combs to identify a stock in the S&P 500 that met three criteria. The first: a reasonably cheap price/earnings multiple of no more than 15, based on the next 12 months’ projected earnings. The stock also had to be one the managers were at least 90% sure would enjoy higher earnings over the next five years. And they had to be at least 50% confident that the company’s earnings would grow by at least 7% annually for five years or longer.

What made the search a little more difficult was that the companies that met the criteria also had to have a market cap large enough so Berkshire could buy enough of to move the needle of its portfolio but not overly impact the demand for the stock.

The Combs Scan

In addition to the criteria in Buffett’s challenge, we added sales growth of at least 5% over the last five years. This helps us thin the list of companies to those already exhibiting strong top-line growth. We also removed financial, limited partnerships, REITs, and real estate stocks as their valuations and growth rates are not as easily comparable using traditional valuation metrics. Lastly, we disqualified Chinese companies due to the potential for political implications.

The following are the factors we used to screen for the next Apple.

- Market cap > $50 billion

- Price to Forward Earnings <15

- Five-year expected earnings growth >5%

- Sales growth in last five years > 5%

- No financial, limited partnerships, REITs, real estate, or Chinese companies.

Many stocks meet the size, earnings, and sales growth criteria. But only two companies have cheap enough valuations to make the cut as shown below.

Currently, Berkshire has 5.242 million shares of T-Mobile, which is .20% of the portfolio. T-Mobile met our criteria, but its 5-year expected earnings growth is slightly below Buffett’s 7% bogey.

Berkshire does not hold EOG but has other oil and gas exploration companies, including Occidental Petroleum and Chevron.

Summary

Warren Buffett is an investing legend and one of the wealthiest people in the world. He takes a value orientation with a long-term investment horizon.

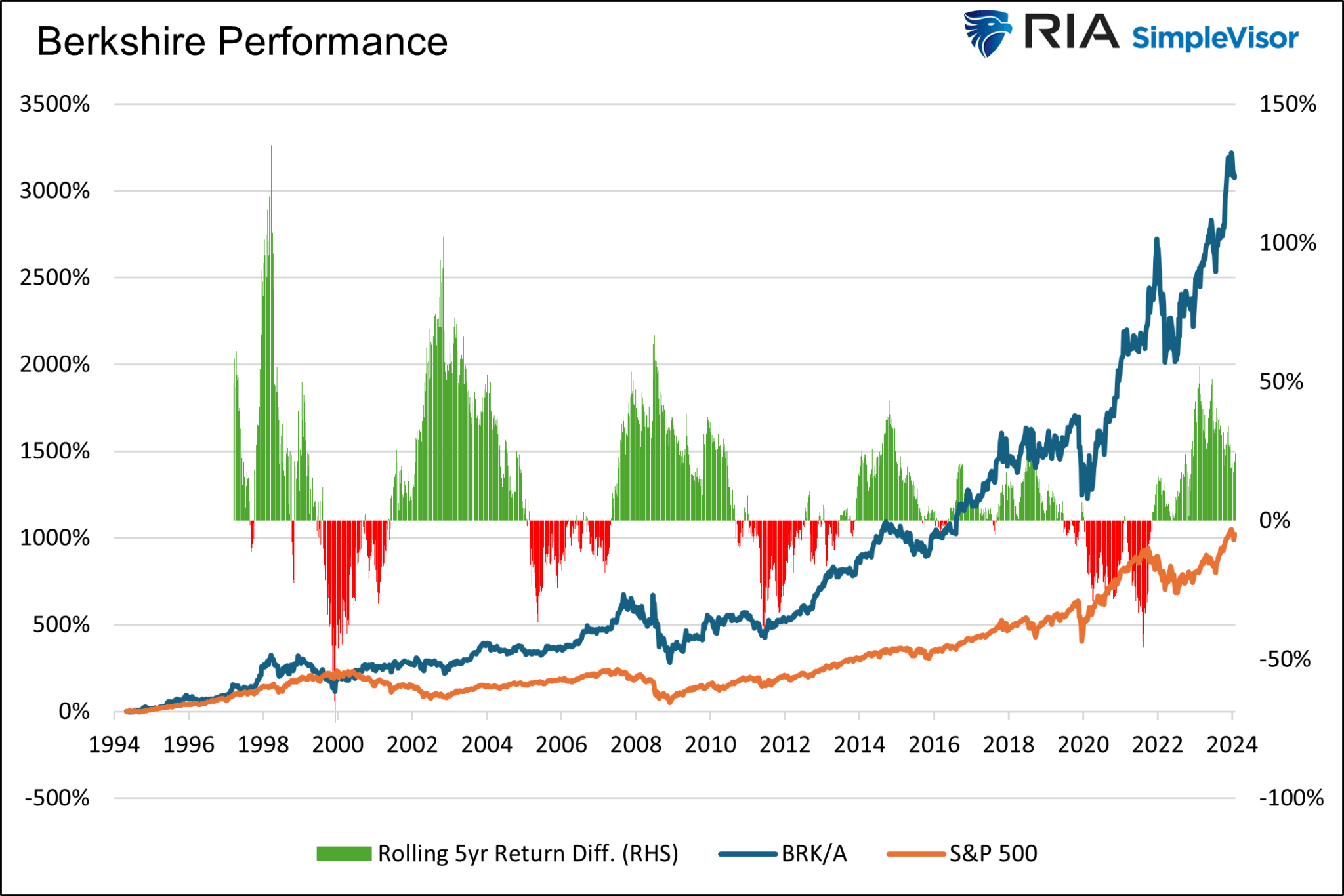

The Berkshire Hathaway portfolio, which also owns private companies, has done exceptionally well versus the market, as shown below. However, he goes through prolonged periods of poor relative performance versus the market.

The graph shows that over the last 30 years, Berkshire’s price return has tripled that of the S&P 500. However, there are four notable extended periods where he grossly underperformed the market. Also of note is that Berkshire handily beat the market in the recession and drawdowns of the dot com bubble and financial crisis. Such attests to his value orientation.

The post Finding The Next Apple Using Buffetts Logic appeared first on RIA.

Stock Rally As Powell Sparks A Buying Frenzy

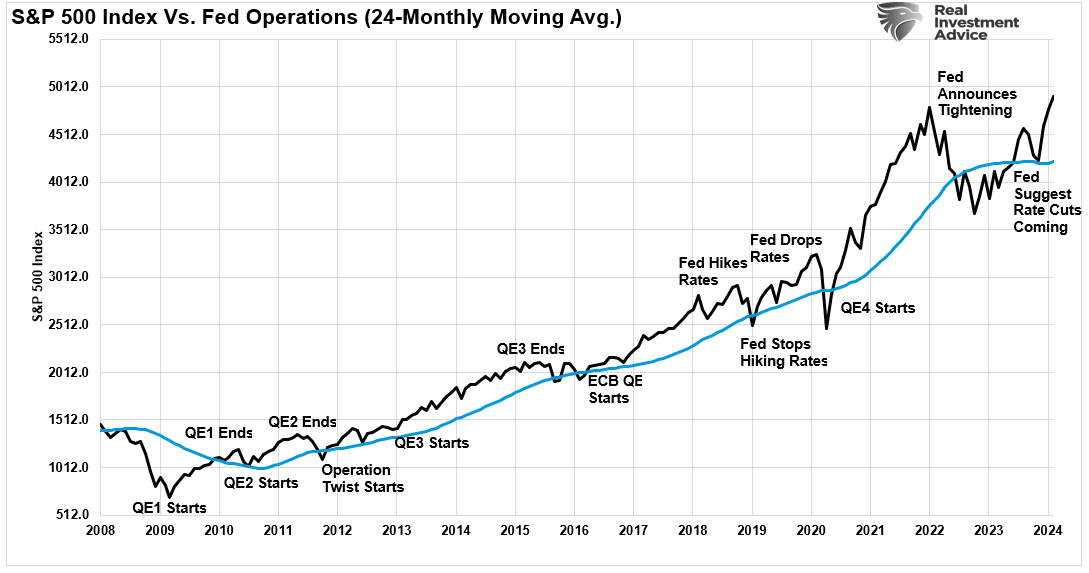

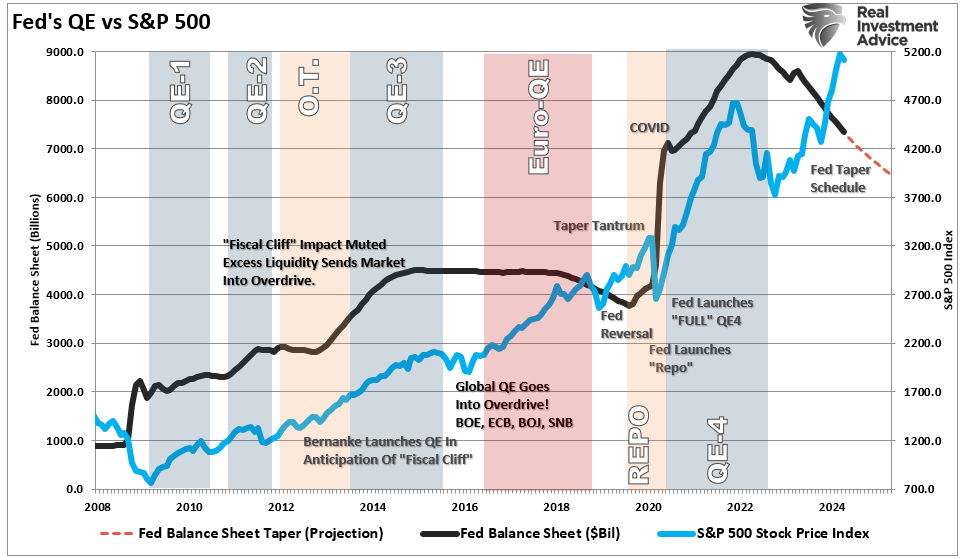

The latest FOMC meeting caused a stock rally as Jerome Powell turned more “dovish” than expected. While Powell did note that progress on inflation has been lackluster, the announcement of the reversal of “Quantitative Tightening” (QT) excited the bulls.

Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage‑backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities”

Of course, the reversal of QT means a buyer of Treasury bonds is returning to the market, increasing overall market liquidity. It also means the Treasury will issue $105 billion less in gross in Q3. The bond market also got the memo, as the Fed’s return to the bond market suggests lower yields in the months ahead, easing financing pressure in the economy.

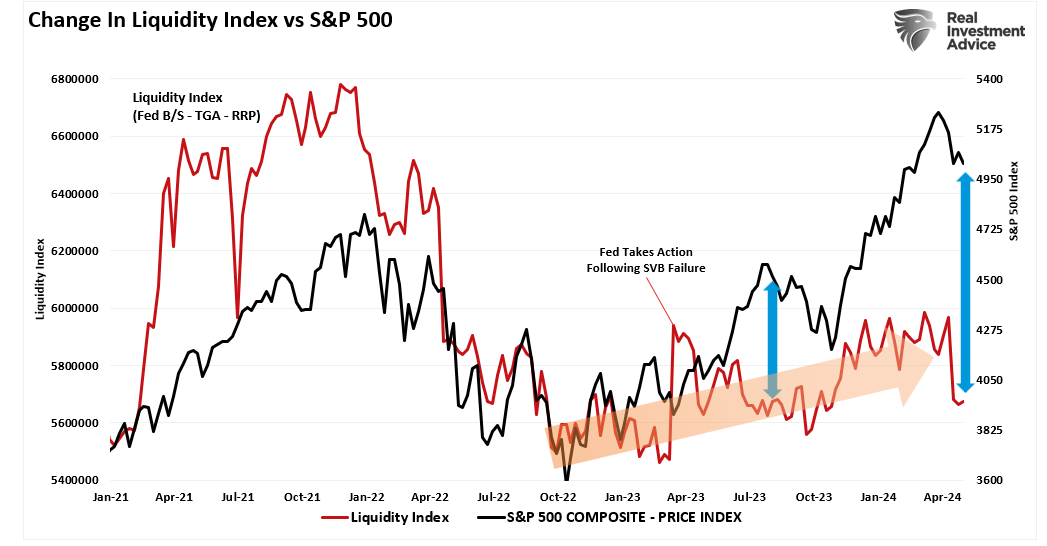

We have previously discussed the following chart of “liquidity,” which subtracts the Treasury General Account and Reverse Repo from the Federal Reserve’s balance sheet. The recent market decline coincided with a sharp drop in liquidity as the TGA account surged to almost $1 trillion from April tax receipts. Over the next few months, that liquidity in the TGA will get released into the economy. At the same time, the Federal Reserve will reduce its balance sheet runoff, which will further add to overall liquidity.

Notably, the market has weathered the reduction in liquidity to date. While higher rates and the reversal of “Quantitative Easing” led to a 20% market decline in 2022, investors began to “front run” the Fed in anticipation of rate cuts and a return to balance sheet expansion.

Given that “QE” programs increase bank reserves by crediting their reserve accounts for bonds bought, the introduction of the tapering of “QT” is the first step in increasing system liquidity.

This is why there was a vicious stock rally last week. For the markets, this rang “Pavlov’s Bell.”

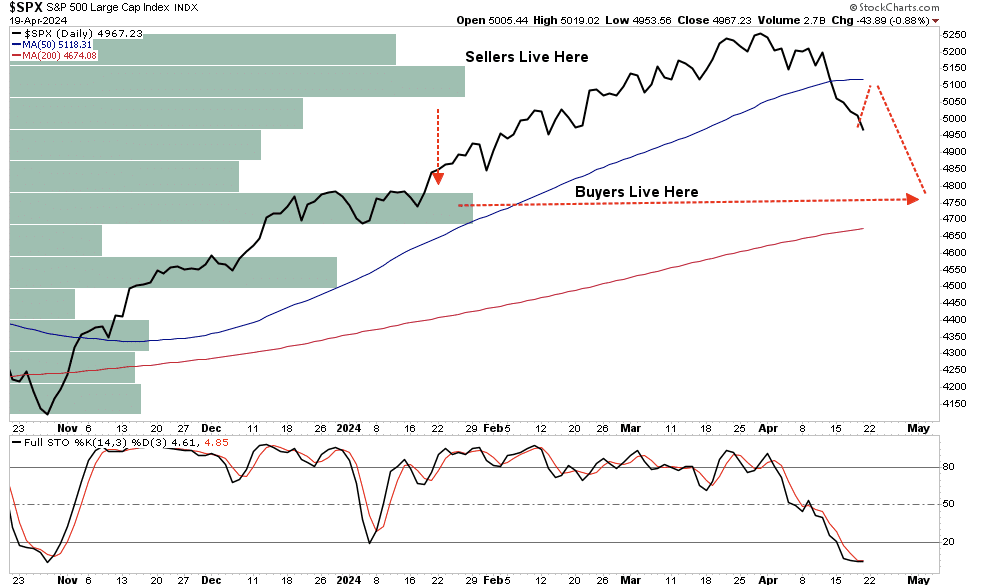

The Correction May Not Be Over Just Yet

While the stock rally last week certainly surprised many, given the weaker-than-expected economic data, there are some reasons to suspect the correction may not be complete just yet.

In mid-March, we suggested that due to the “buyback blackout” window, a 5-10% correction was likely. To wit:

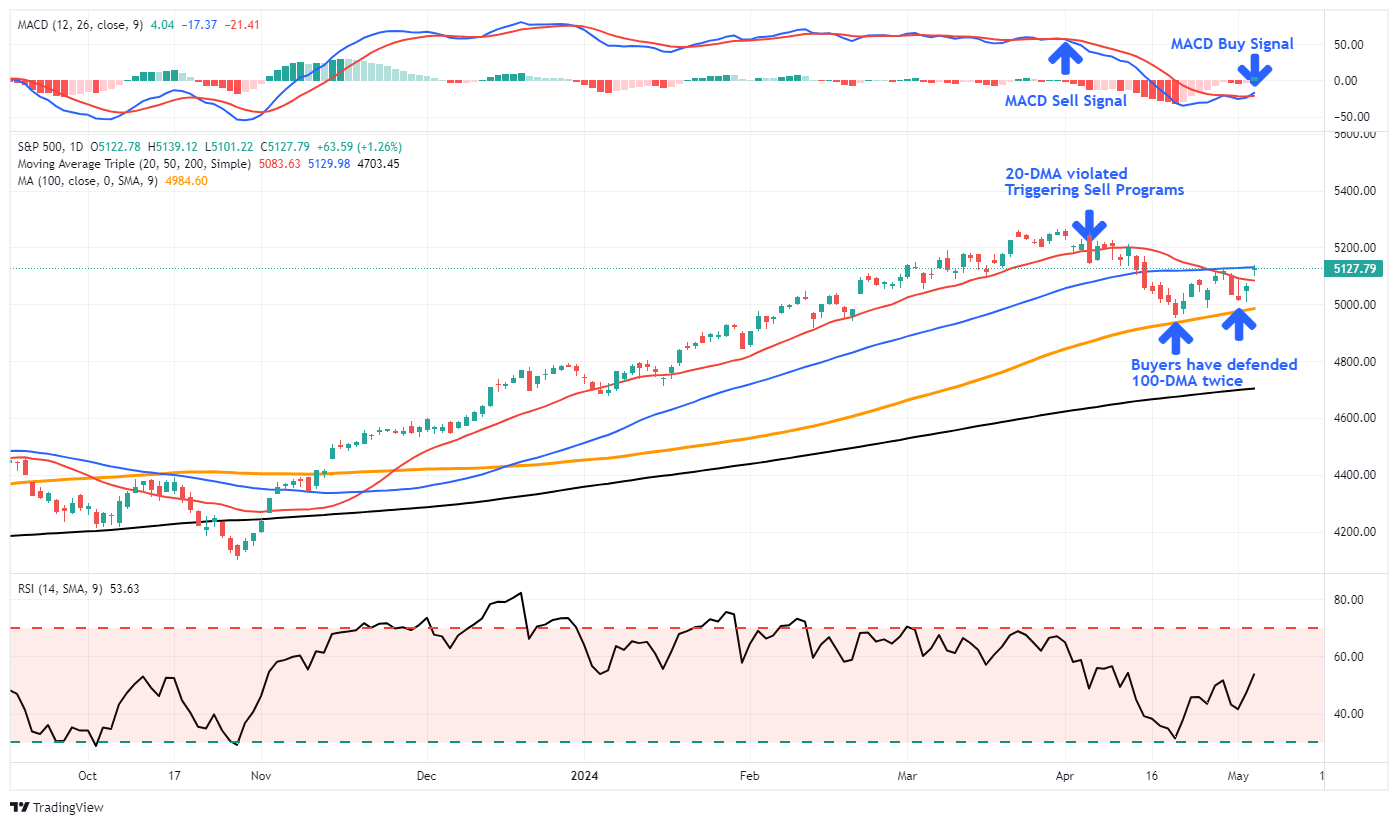

“As noted, the market remains in a bullish trend. The 20-DMA, the bottom of the trend channel, will likely serve as an initial warning sign to reduce risk when it is violated. That level has repeatedly seen ‘buying programs’ kick in and suggests that breaking that support will cause the algos to start selling. Such a switch in market dynamics would likely lead to a 5-10% correction over a few months.“

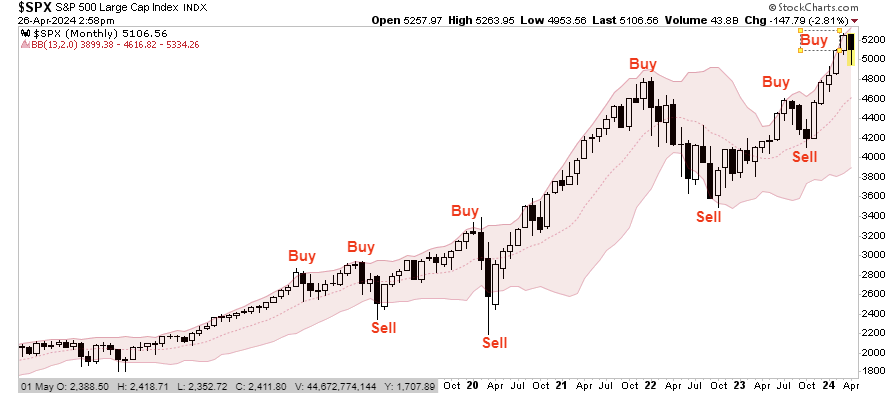

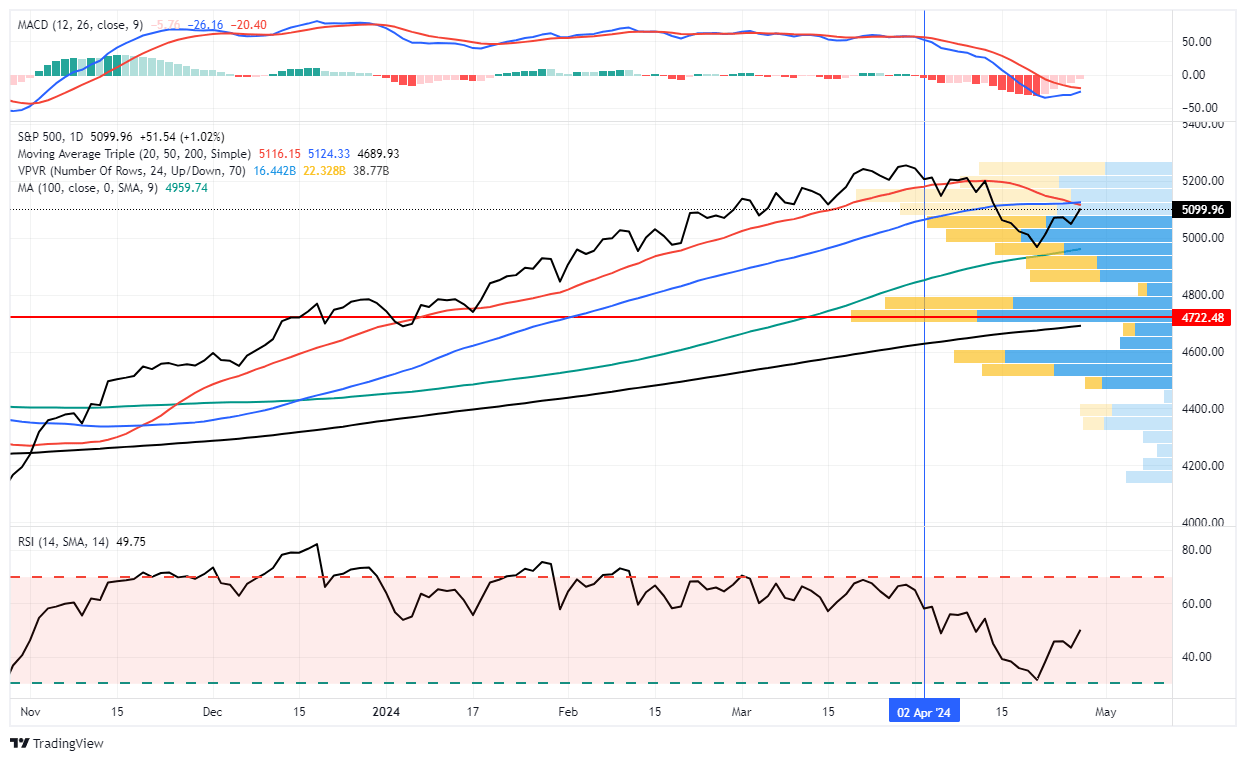

The following month, the market violated that 20-DMA, and selling commenced, leading to a 5.5% drawdown. However, buyers initially stepped back in at the 100-DMA, which has now acted as support over the last two weeks. With the rally last week, the stock rally is now testing crucial resistance at the 50-DMA.

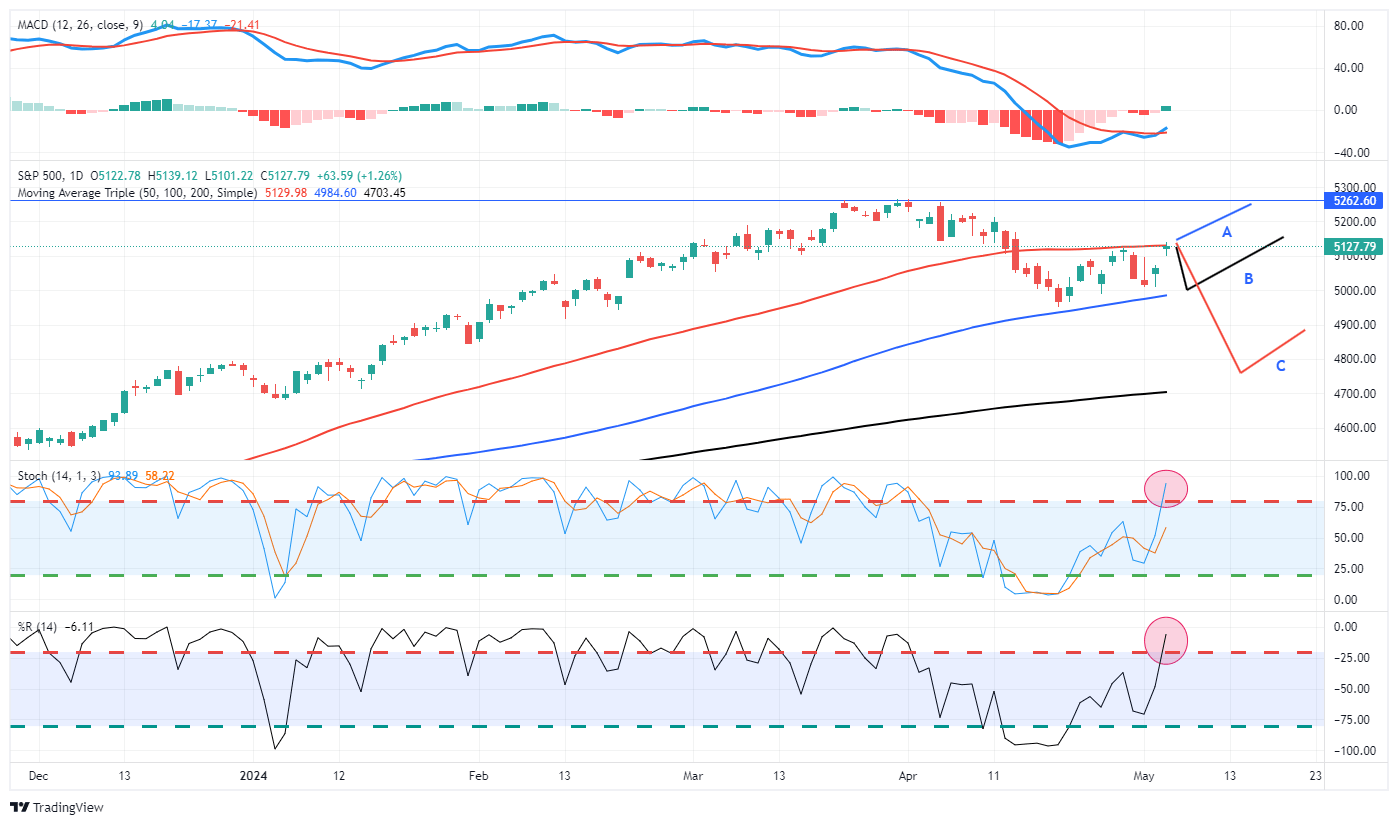

The stock rally is at a critical juncture, and what happens next will determine whether the current market correction is over. Three possible scenarios over the next month or so exist.

Path A: The market breaks above the 50-DMA and retests previous highs. While this path is indeed possible, the markets are overbought on a very short-term basis, suggesting further price appreciation will become more challenging.

Path B: Many investors were surprised by the recent market decline. As such, these “trapped longs” will likely use the current stock rally as an opportunity to reduce risk. Another retest of the 100-DMA seems probable before the next leg of the current bull rally ensues.

Path C: With earnings season mostly behind us and stock buybacks set to resume, a reversion to the 200-DMA seems the least probable. However, as is always the case, it is a risk that we should not ignore. A sharp uptick in inflation or stronger-than-expected economic data could spark concerns about a “higher for longer” Fed policy. Such an event would likely lead to a further repricing of risk assets.

I am less concerned about “Path C” for three reasons.

Little Evidence Of Market Stress

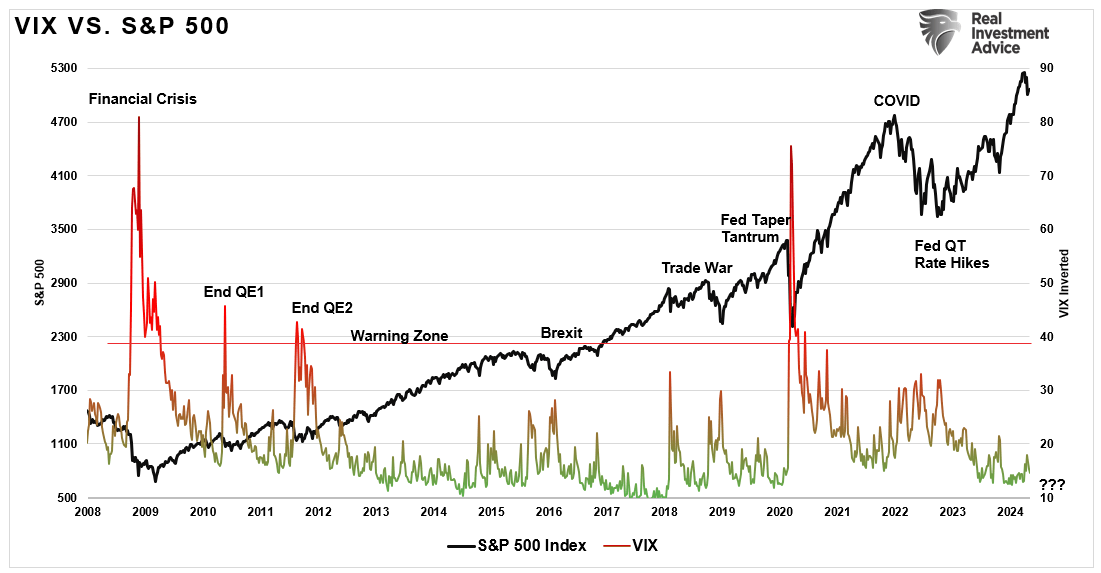

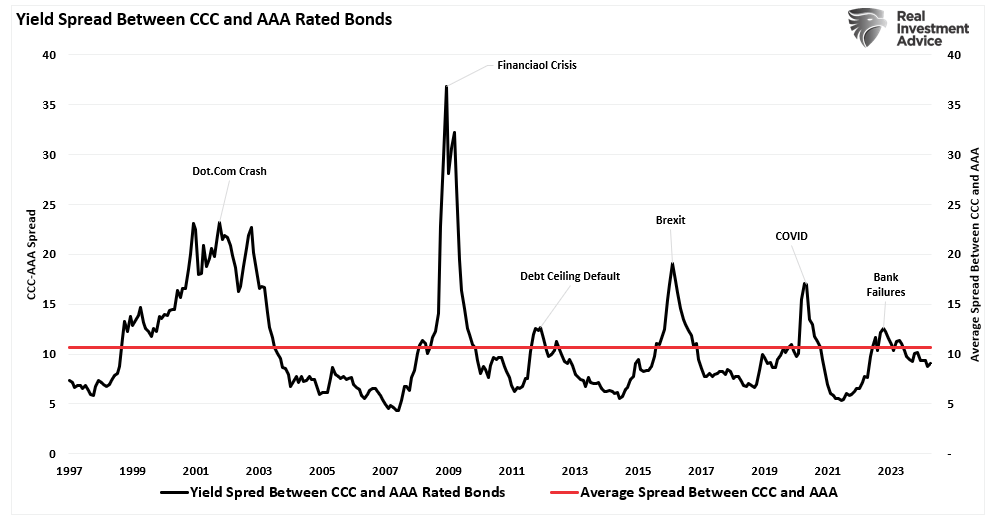

While a more profound decline is certainly possible, there is little evidence of market stress. For example, even during the latest correction, volatility remained very subdued. Yes, volatility increased during the decline but failed to reach the levels witnessed during the 10% correction last summer.

Secondly, a substantially deeper market decline would likely widen credit spreads between junk bonds and treasuries. That was not evident during the latest market decline, as spreads remain well below the long-term average. Watching credit spreads is the best indicator for investors to determine market risks.

Third, the window for stock buybacks reopens this week, and with Apple and Google announcing $110 and $70 billion programs, respectively, those two companies alone will account for roughly 18% of this year’s slated activity.

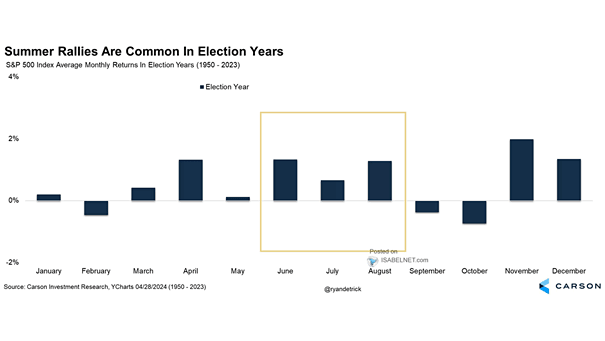

Combining current sentiment, buybacks, and liquidity hopes makes the stock rally over the last two weeks logical. Furthermore, given that early summer months tend to be bullish for markets during election years, it is likely too soon to be overly bearish.

However, we are also not completely oblivious to the numerous risks that lie ahead. Weaker economic data, the lag effect from higher rates, and sticker inflation pose portfolio risks worth monitoring. Furthermore, in the two months before the election, investors tend to de-risk their portfolios. This year, we could see a larger-than-normal event, given the risks associated with the current matchup.

While Powell’s “dovish” twist fueled the current stock rally, continue to manage risk accordingly. There is a reasonable chance this correction is not over just yet.

The post Stock Rally As Powell Sparks A Buying Frenzy appeared first on RIA.

Behavioral Traits That Are Killing Your Portfolio Returns

Investor psychology is one of the most significant reasons individuals consistently fall short of their investment goals. While one of the most common truisms is that “investors buy high and sell low,” the underlying reason is the behavioral traits that plague our investment decision-making.

George Dvorsky once wrote that:

“The human brain is capable of 1016 processes per second, which makes it far more powerful than any computer currently in existence. But that doesn’t mean our brains don’t have major limitations. The lowly calculator can do math thousands of times better than we can, and our memories are often less than useless — plus, we’re subject to cognitive biases, those annoying glitches in our thinking that cause us to make questionable decisions and reach erroneous conclusions.“

Behavioral traits and cognitive biases are anathemas to portfolio management as they impair our ability to remain emotionally disconnected from our money. As history all too clearly shows, investors always do the “opposite” of what they should when it comes to investing their own money. They “buy high” as the emotion of “greed” overtakes logic and “sell low” as “fear” impairs the decision-making process.

In other words:

“The most dangerous element to our success as investors…is ourselves.”

Here are the top five most insidious behavioral traits keeping us from achieving our long-term investment goals.

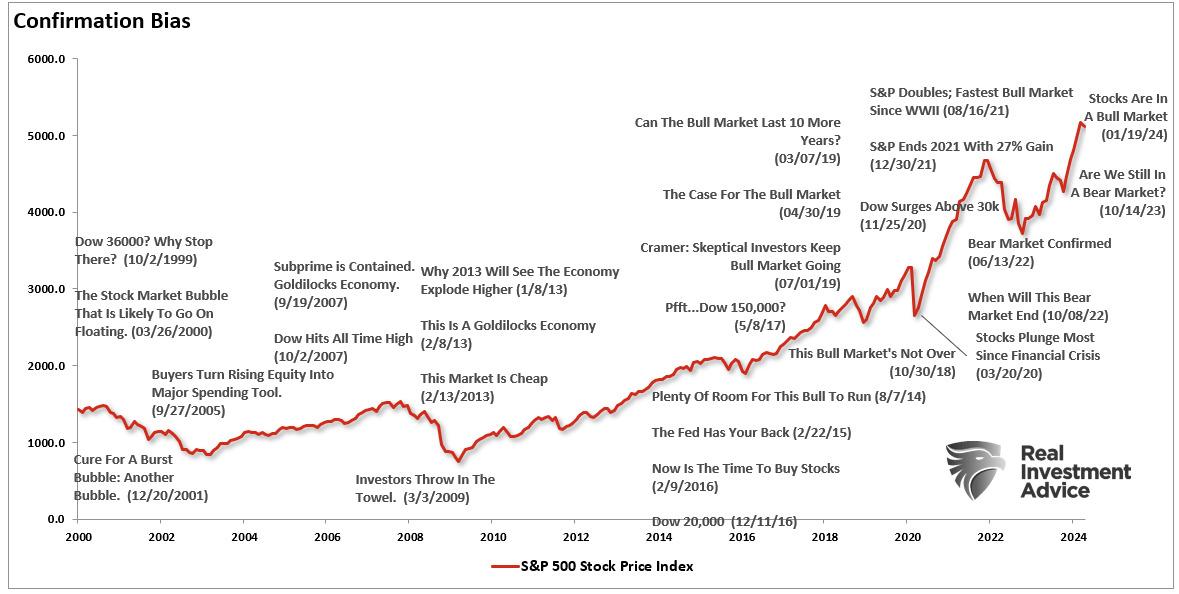

Confirmation Bias

Probably one of the most insidious behavioral traits is “confirmation bias.” Confirmation bias is a term from cognitive psychology that describes how people naturally favor information that confirms their previously existing beliefs.

“Experts in behavioral finance find that this fundamental principle applies to investors in notable ways. Because investors seek out information that confirms their opinions and ignore facts or data that refutes them, they may skew the value of their decisions based on their cognitive biases. This psychological phenomenon occurs when investors filter out potentially useful facts and opinions contradicting their preconceived notions.” – Investopedia

In other words, investors tend to seek information that confirms their beliefs. If they believe the stock market will rise, they tend only to read news and information that supports that view. This confirmation bias is a primary driver of individuals’ psychological investing cycles. As shown below, there are always “headlines” from the media to “confirm” an investor’s opinion, whether it’s bullish or bearish.

As investors, we want “affirmation” that our current thought process is correct. That is why we tend to join groups on social media that confirm our thoughts and ideals. Therefore, since we hate being wrong, we subconsciously avoid contradicting sources of information.

For investors, it is crucial to weigh both sides of each debate equally and analyze the data accordingly.

Being right and making money are not mutually exclusive.

Gambler’s Fallacy

The “Gambler’s Fallacy” is another of the more common behavioral traits. As emotionally driven human beings, we tend to put tremendous weight on previous events, believing that future outcomes will be the same.

At the bottom of every piece of financial literature, Wall Street addresses that behavioral trait.

“Past performance is no guarantee of future results.”

However, despite that statement being plastered everywhere in the financial universe, individuals consistently dismiss the warning and focus on past returns, expecting similar results in the future.

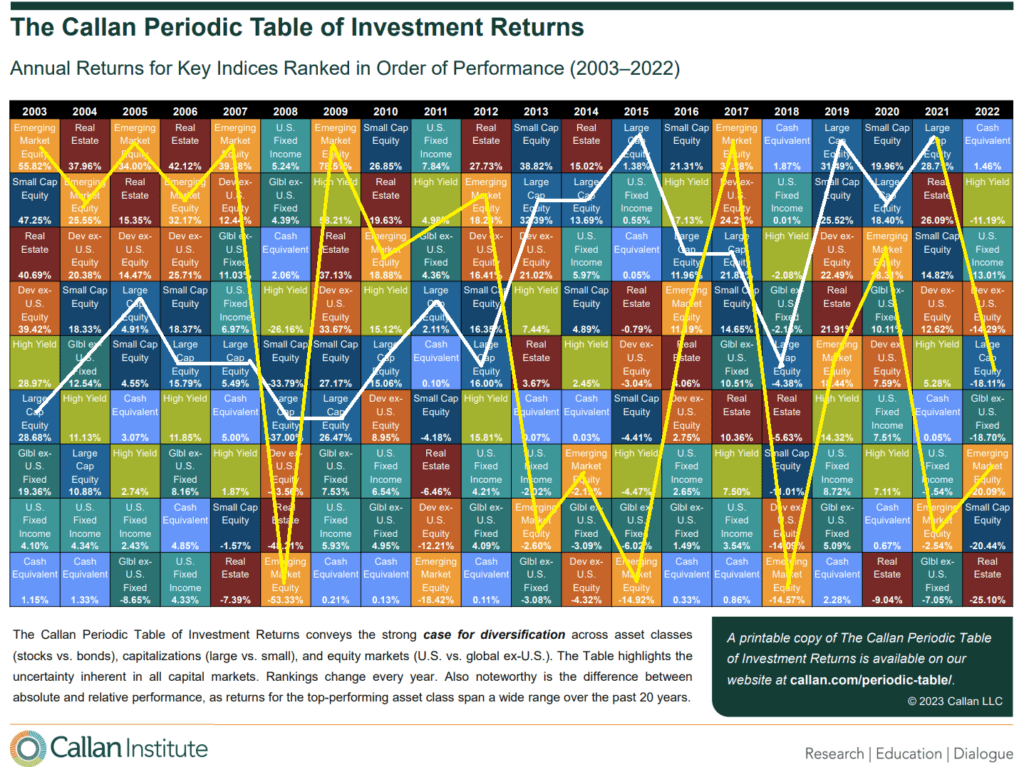

This particular behavioral trait is a critical issue affecting investors’ long-term returns. Performance chasing has a high propensity to fail, pushing individuals to jump from one late-cycle strategy to the next. The periodic table of returns below shows this. Historically, “hot hands” last 2-3 years before going “cold.”

I highlighted the annual returns of both Emerging and Large-Cap markets for illustrative purposes. Importantly, you should notice that whatever is at the top of the list in some years tends to fall to the bottom in subsequent years.

“Performance chasing” is a significant detraction from investors’ long-term investment returns.

Probability Neglect

Third, when it comes to “risk-taking,” there are two ways to assess the potential outcome.

There are “possibilities” and “probabilities.”

When it comes to humans, we tend to lean toward what is possible, such as playing the “lottery.” The statistical probabilities of winning the lottery are astronomical. You are more likely to die on the way to purchasing the ticket than winning it. However, it is the “possibility” of being fabulously wealthy that makes the lottery so successful as a “tax on poor people.”

As investors, we neglect the “probabilities” of any given action. Such is specifically the statistical measure of “risk” undertaken with any given investment. As individuals, our behavioral trait is to “chase” stocks that have already shown the largest increase in price as it is “possible” they could move even higher. However, the “probability” is that the price reflects investor exuberance, and most gains have already occurred.

Probability neglect is another contributory factor as to why investors consistently “buy high and sell low.”

Herd Bias

Though we are often unconscious of this particular behavioral trait, humans tend to “go with the crowd.” Much of this behavior relates to “confirmation” of our decisions and the need for acceptance. The thought process is rooted in the belief that if “everyone else” is doing something, I must do it also if I want to be accepted.

In life, “conforming” to the norm is socially accepted and, in many ways, expected. However, the “herding” behavior drives market excesses during advances and declines in the financial markets.

As Howard Marks once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

Investors generate the most profits in the long term by moving against the “herd.” Unfortunately, most individuals have difficulty knowing when to “bet” against the stampede.

Anchoring Effect

Lastly, “Anchoring,” also known as the “relativity trap,” is the tendency to compare our current situation within the scope of our limited experiences. For example, I would be willing to bet that you could tell me exactly what you paid for your first home and what you eventually sold it for. However, can you tell me exactly what you paid for your first soap bar, hamburger, or pair of shoes? Probably not.

The reason is that the home purchase was a major “life” event. Therefore, we attach particular significance to that event and remember it vividly. If there was a gain between the purchase and sale price of the home, it was a positive event, and therefore, we assume that the next home purchase will have a similar result. We are mentally “anchored” to that event and base our future decisions around very limited data.

When it comes to investing, we do very much the same thing. If we buy a stock that goes up, we remember that event. Therefore, we become anchored to that stock instead of one that lost value. Individuals tend to “shun” stocks that lost value even if they were bought and sold at the wrong times due to investor error.

After all, it is not “our” fault that the investment lost money; it was just a bad stock. Right?

Make Better Bad Choices

My nutrition coach had a great saying about dieting; “make better bad choices.”

We are all going to make bad choices from time to time. The goal is to try and make bad choices that don’t have an outsized effect on our plan. When it comes to dieting, if you eat a burger, order it without cheese and mayonnaise.

If you make speculative bets in your portfolio, do it in smaller amounts. Or, if you are leaning towards “panic selling” everything, start by selling some but not all of your holdings.

Importantly, focus on the rules and your investment discipline.

- Do more of what is working and less of what isn’t.

- Remember that the “Trend Is My Friend.”

- Be either bullish or bearish, but not “hoggish.” (Hogs get slaughtered)

- Remember, it is “Okay” to pay taxes.

- Maximize profits by staging buys, working orders, and getting the best price.

- Look to buy damaged opportunities, not damaged investments.

- Diversify to control risk.

- Control risk by always having pre-determined sell levels and stop-losses.

- Do your homework.

- Not allow panic to influence buy/sell decisions.

- Remember that “cash” is for winners.

- Expect, but do not fear, corrections.

- Expect to be wrong, and will correct errors quickly.

- Check “hope” at the door.

- Be flexible.

- Have the patience to allow your discipline and strategy to work.

- Turn off the television, put down the newspaper, and focus on your analysis.

Importantly, keep your market perspectives and behavioral traits in check. Our goal is to ensure that our decisions are influenced by reliable data and psychological emotions.

Most importantly, if you don’t have an investment strategy and discipline you are stringently following, that is an ideal place to begin.

The post Behavioral Traits That Are Killing Your Portfolio Returns appeared first on RIA.

Fed Policies Turn The Wealth Gap Into A Chasm

In an op-ed for the Washington Post on November 5, 2010, Ben Bernanke did a victory lap, praising the Fed’s efforts in stemming the financial crisis. In the article, he discusses how QE and other Fed policies eased financial conditions, bolstering investor confidence.

And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.

If Bernanke wants credit for his Fed policies that boosted stock prices, he should also take responsibility for the costs. Those same monetary policies, which have been repeated many times since 2008, have played an important role in exacerbating the wealth gap in America. Accordingly, we should question his use of the term “virtuous circle” to describe how modern monetary policy works.

Graphing The Wealth Gap

Inspiration for this article comes from our recent article, Wealth Gap and the Road to Serfdom.

Before discussing the Fed’s role in widening the wealth gap, we put context to the problem. The graphs and quote below are from the article.

For 80% of Americans, the end game of too much debt, an aging demographic, and the push for “socialistic policies” is the continued extraction of wealth from the “middle class” to the “rich.”

Trickledown Economics and Monetary Policy

“Trickledown economics” was coined by John Kenneth Galbreth in 1982 and made famous by President Ronald Reagan. The expression is another name for supply-side economic policy. The policy theorizes that the populace benefits when government interference in the economy is minimal. For example, lower taxes and reduced regulations should promote economic activity and prosperity for the entire populace.

The theory is logical, but politicians have done a poor job enacting it.

In 2008, the Fed took a page from the supply-side economic playbook to stem the financial crisis. From that point forward, the Fed’s modus operandi has been trickle-down monetary policies.

Does QE Trickle Down?

Ben Bernanke wasn’t the first Fed Chair or central banker to use QE. But he did make it a household name and seemingly a permanent tool in the Fed’s toolbox.

QE has two significant impacts on the financial markets and the banking system.

First, removing assets from financial markets alters the supply-demand balance in favor of higher prices. Additionally, when investors believe QE is positive for asset prices, as is the case, demand increases, which provides even more impetus for higher asset prices.

Second, the Fed buys bonds from the banks with reserves. Reserves are a form of money that is only viable in transactions between banks or with the Fed. Reserves support bank loans and asset purchases. Therefore, when more reserves are available, banks can more easily make loans and buy assets. Further, some bank loans, specifically margin or repo loans, generate additional demand for assets.

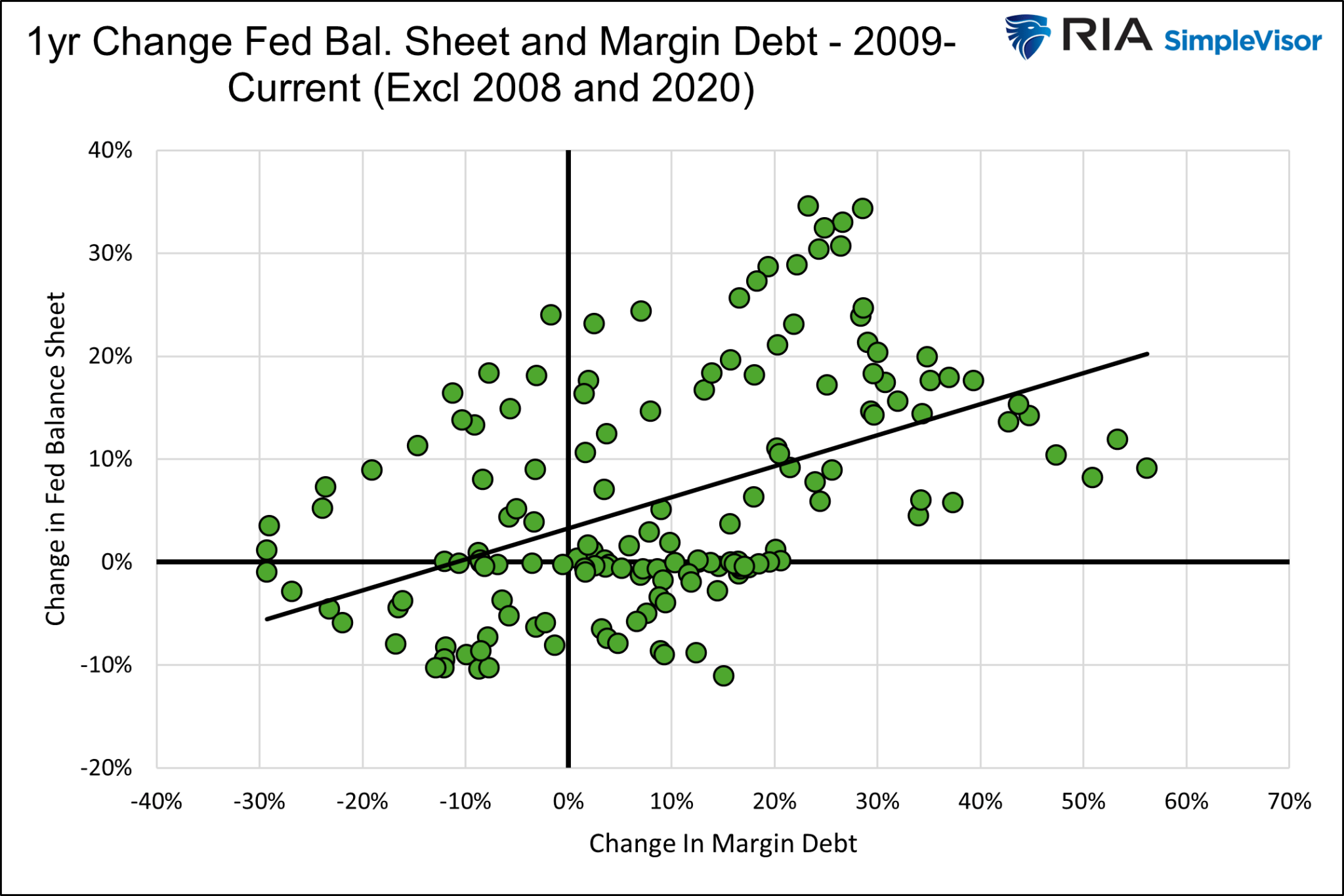

The scatter plot below shows the positive correlation between the one-year percentage change in margin debt and the Fed’s balance sheet.

Higher stock and asset prices coupled with more leverage is a winning combination for investors.

The Graph of All Graphs

With that explanation of how trickledown monetary policy bolsters asset prices to accomplish the Fed’s goals, we share a graph explaining why the Fed’s policies widen the wealth gap.

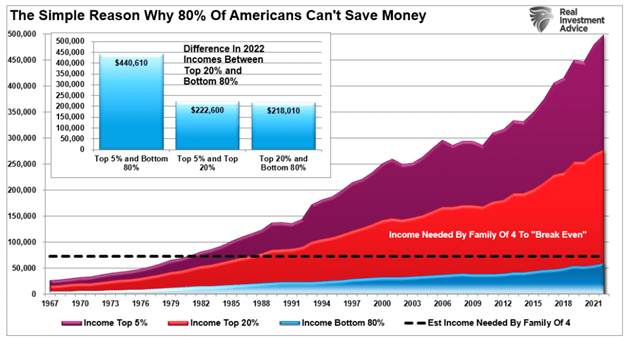

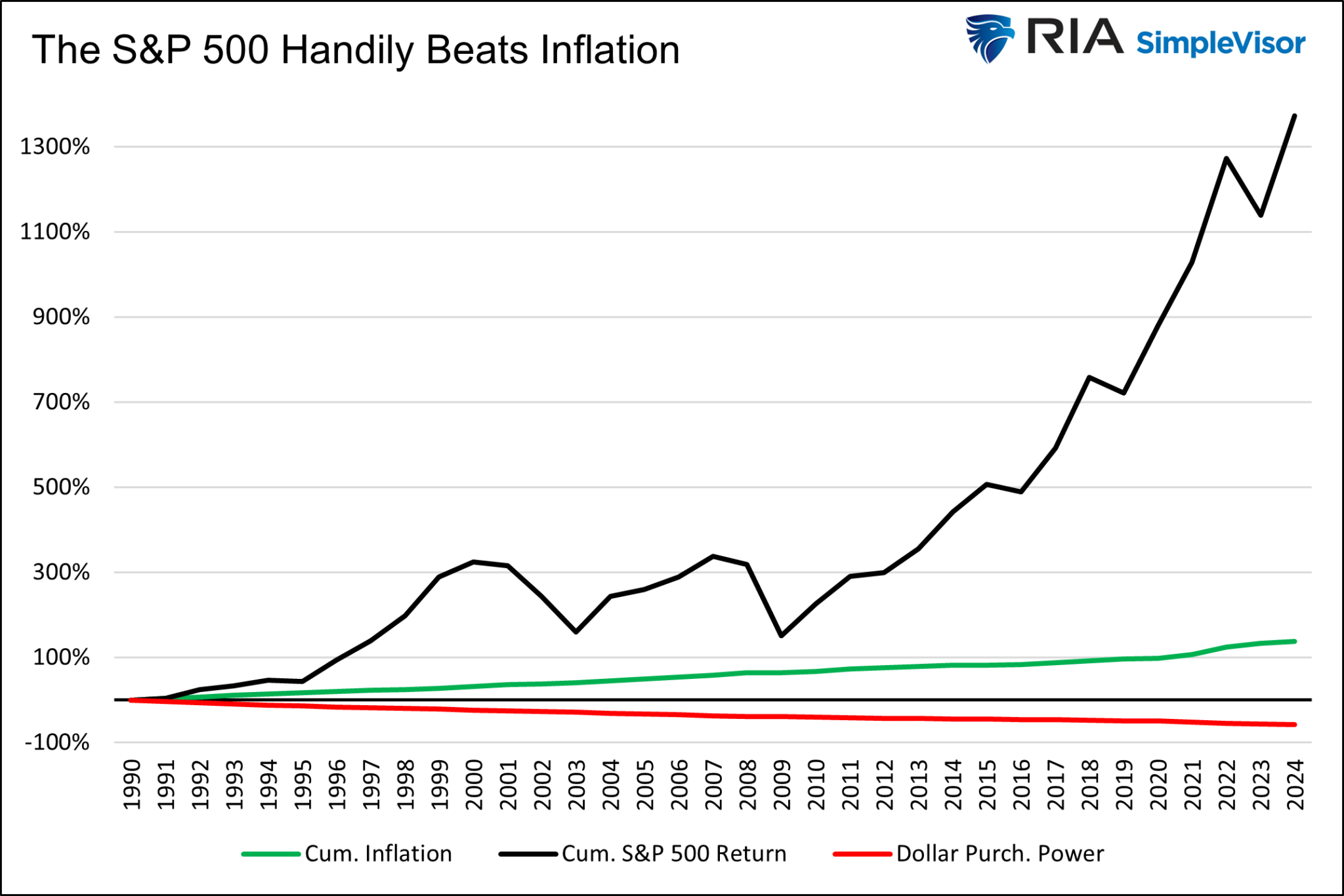

Since 1990, the dollar’s purchasing power has declined by over 50%. At the same time, the S&P 500 has risen by over 1,300%. Those with a sufficient portfolio of stocks could more than offset the decline in the dollar’s purchasing power. Those without stocks are left behind.

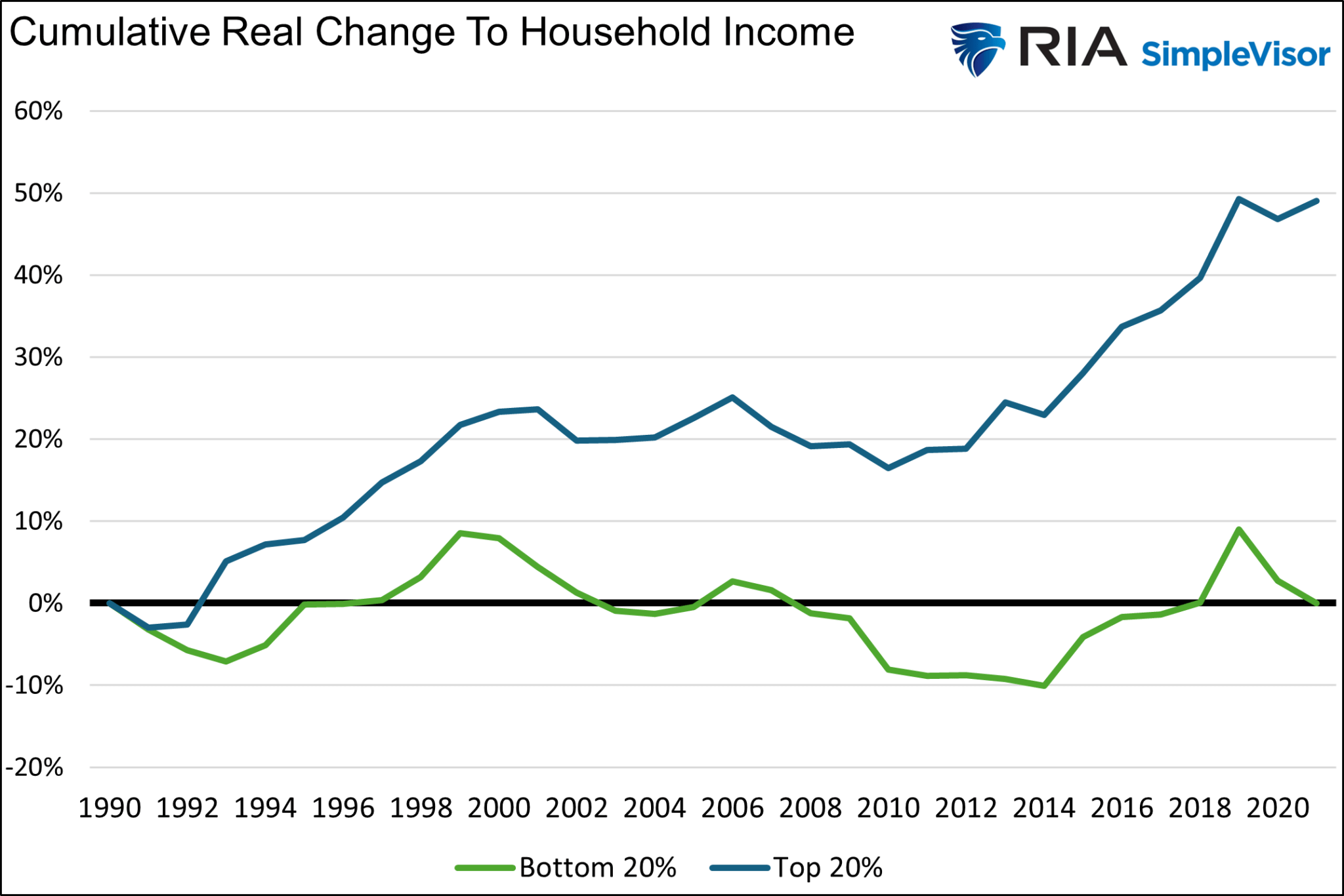

Further, it doesn’t help that real household income for the lowest 20% has been unchanged since 1990. Over the same period, they have risen by about 50% for those in the upper 20% of incomes.

Share Of Wealth

The wealthier have seen their wages and the value of their financial assets rise much more than inflation. At the same time, the lower wealth and income classes have seen marginal real income gains at best and little in the way of benefits from rising stock prices.

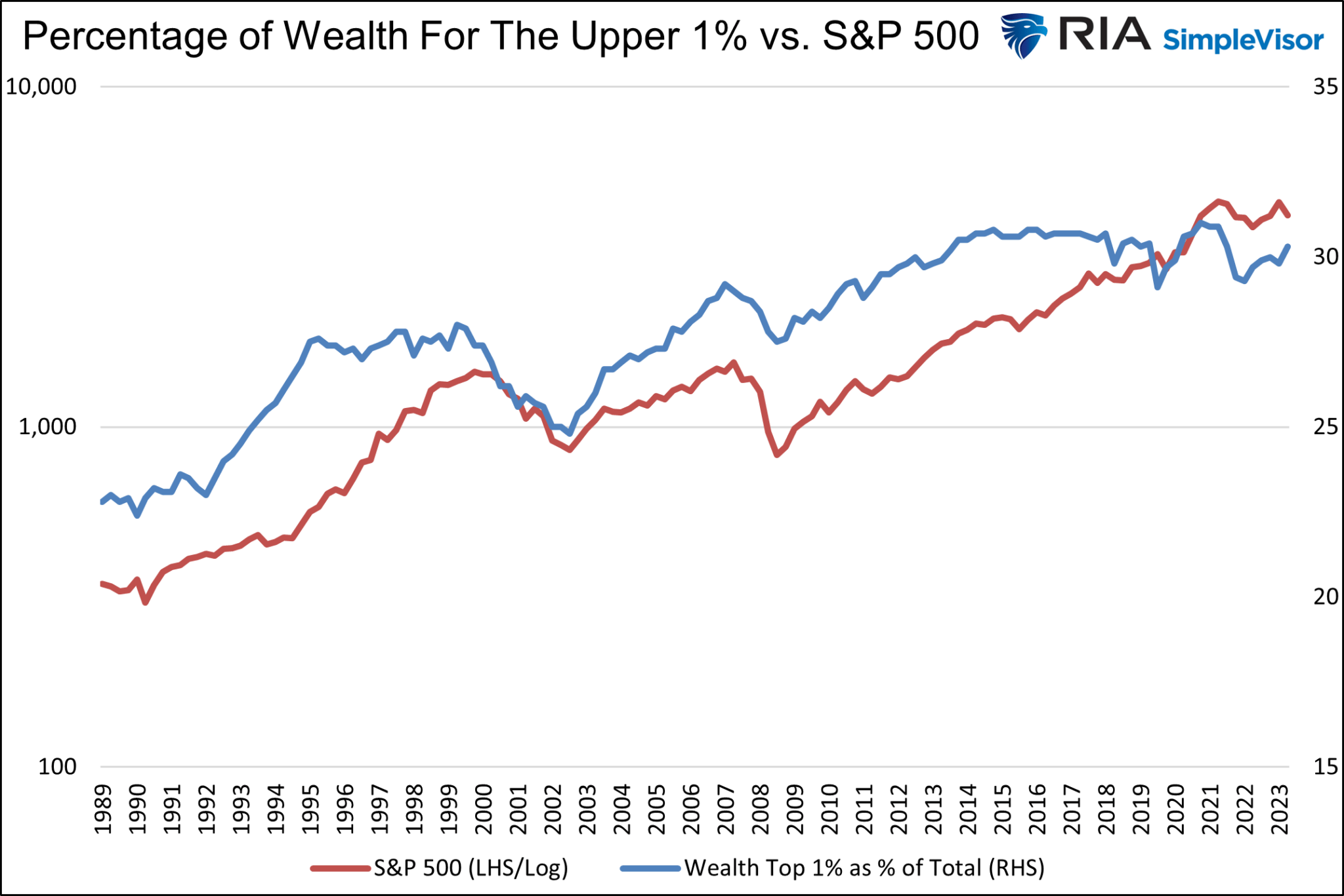

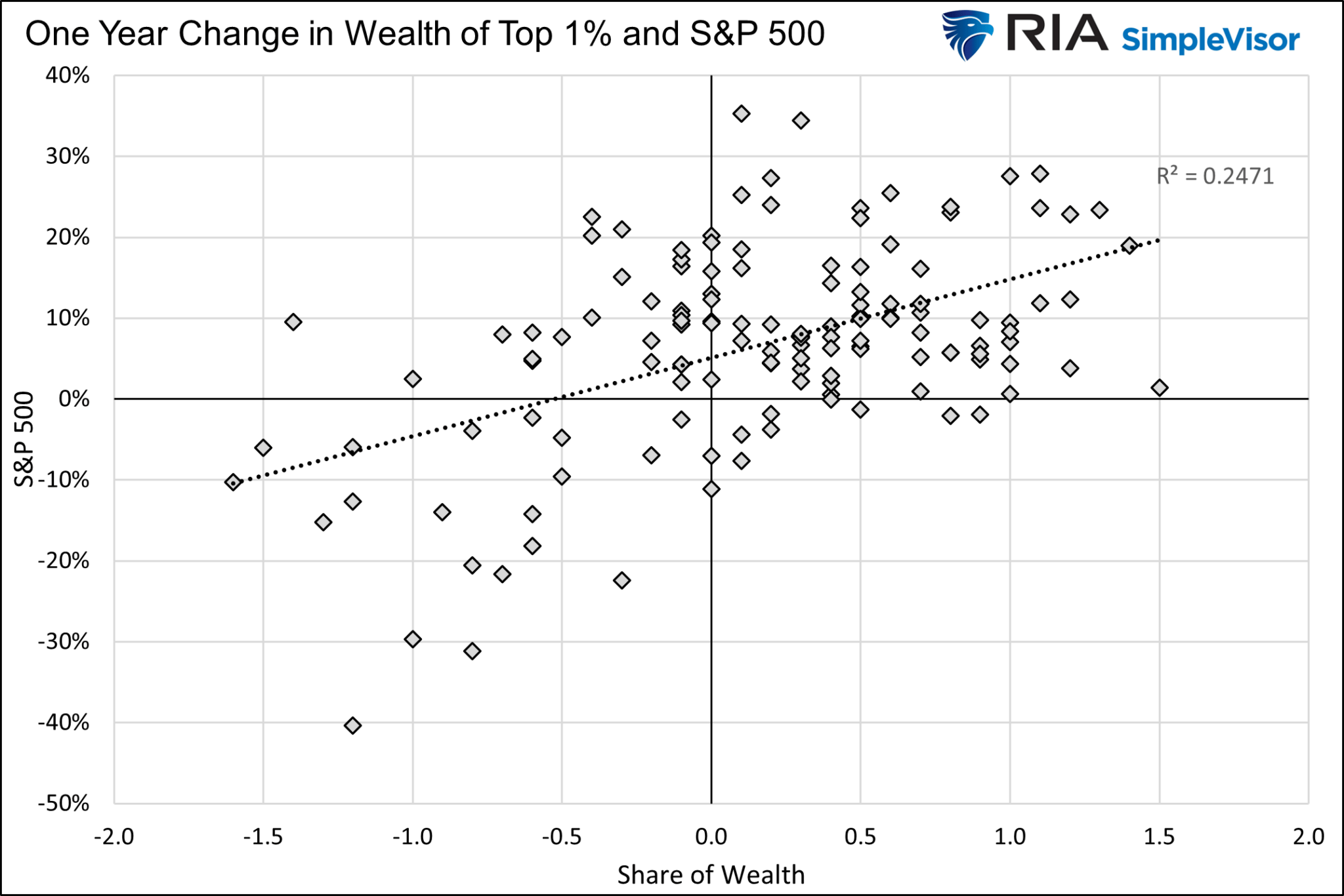

The two graphs below show how the percentage of the wealth owned by the top 1% and the change in the S&P 500 are well correlated.

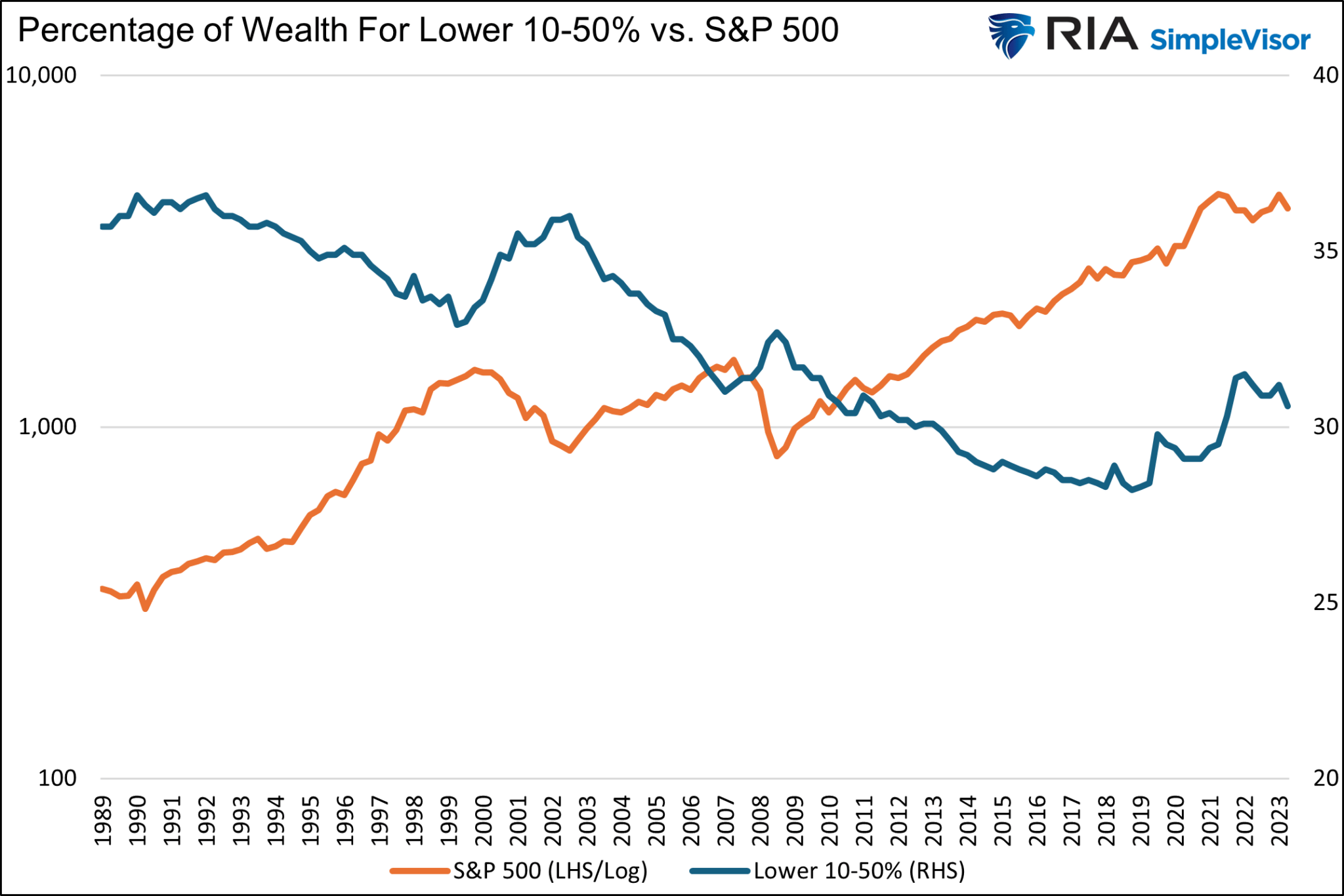

On the contrary, the aggregate wealth of much of the bottom half of the nation, as a percentage of total wealth, has a negative relationship with the S&P 500.

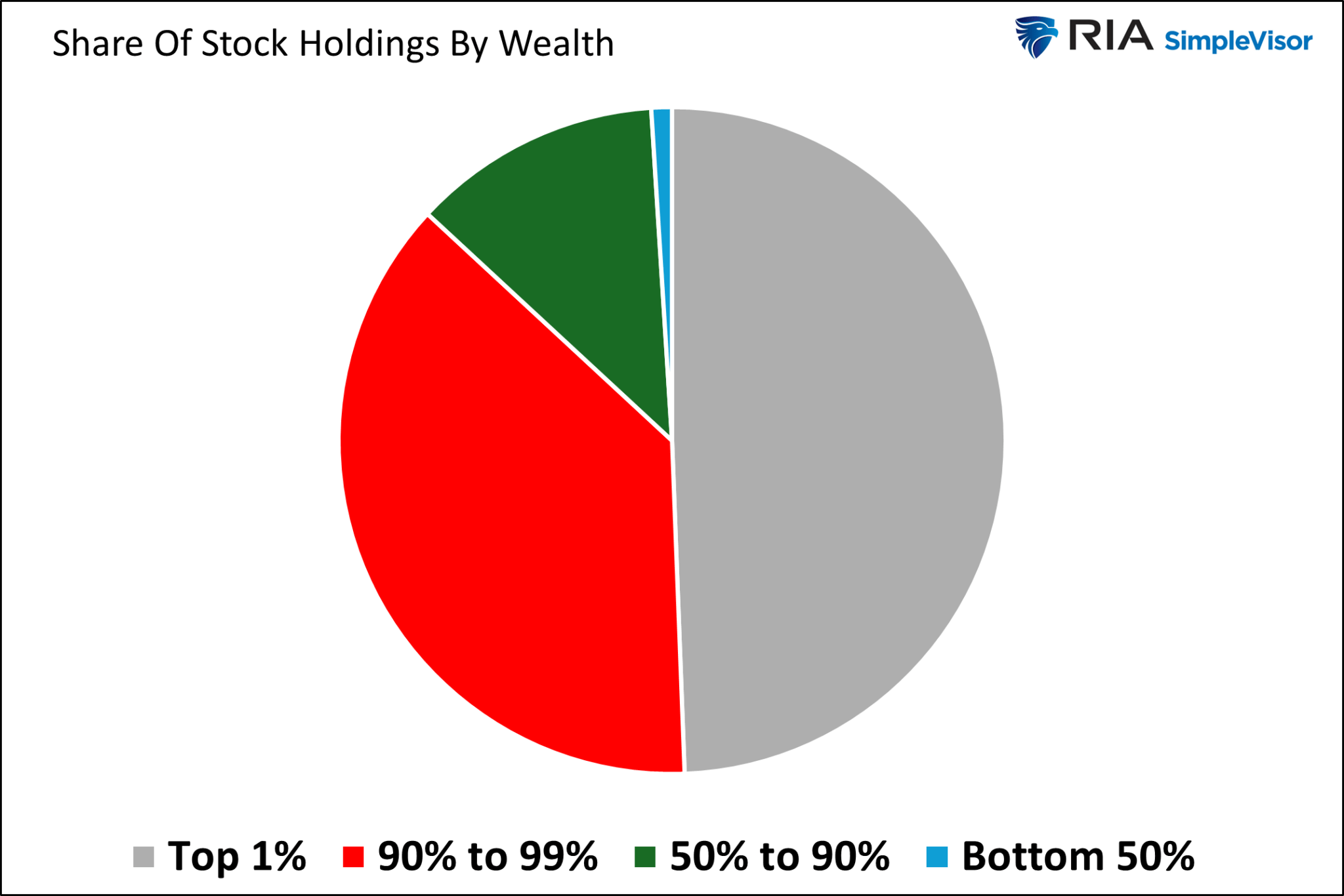

There is a straightforward explanation as to why the correlation between the share of the wealth of the rich versus that of the rest of the population has opposing correlations to the S&P 500. 10% of the population holds nearly 90% of the stocks.

Trickledown Monetary Policy Handicaps Capitalism

QE and other Fed policies may help the economy on the margin and save some jobs. However, there is little evidence that, over the longer term, the economic benefits increase the prosperity of most of the populace. Further, as we share, there is compelling evidence it further exacerbates the wealth gap.

Capitalism has proven to be the best economic system for growing the wealth of the entire population. A key tenant of capitalism promises financial incentives for those who work hard and have unique skill sets. That incentive results in productivity gains, which benefit economic growth and allow for higher wages and a broad distribution of wealth.

Unfortunately, when financial incentives are not only a function of capitalism but also an offshoot of government and Fed policies, the benefits of capitalism are reduced.

For example, Elon Musk is extraordinarily wealthy and should be rewarded handsomely for everything he has accomplished. However, how much of his wealth is based on his hard work and ingenuity, and how much was gifted to him by the Fed via their stock-boosting monetary policies. While slightly off-topic, we should also question how much of his wealth is attributable to government subsidies for electric vehicles.

Summary

President Biden’s poll numbers on economic confidence are poor despite robust economic growth and a historically low unemployment rate. While there are many reasons for the odd divergence, we think it’s fair to say that the benefits of the post-pandemic growth spurt have disproportionately accrued to those in higher-income classes and those with stocks. Those left behind, representing a large majority of the population, are not confident in Biden’s handling of the economy and suffer from higher prices.

Most Americans continue to see wages that cannot combat inflation and have little to no wealth invested in the stock market. Can you blame them for lacking confidence?

QE may have served as an emergency way to add bank reserves to the system and boost confidence. However, its continued use, even during economic prosperity periods, only makes the wealth gap wider.

The post Fed Policies Turn The Wealth Gap Into A Chasm appeared first on RIA.

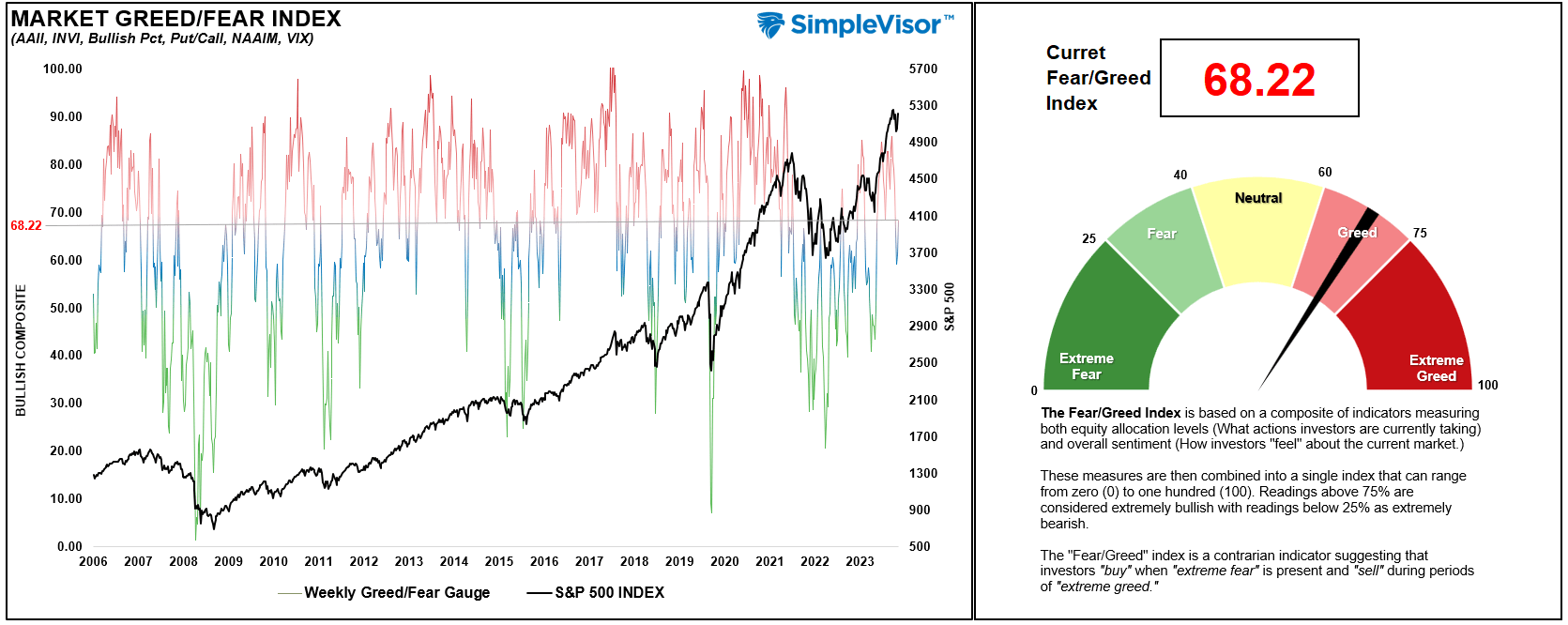

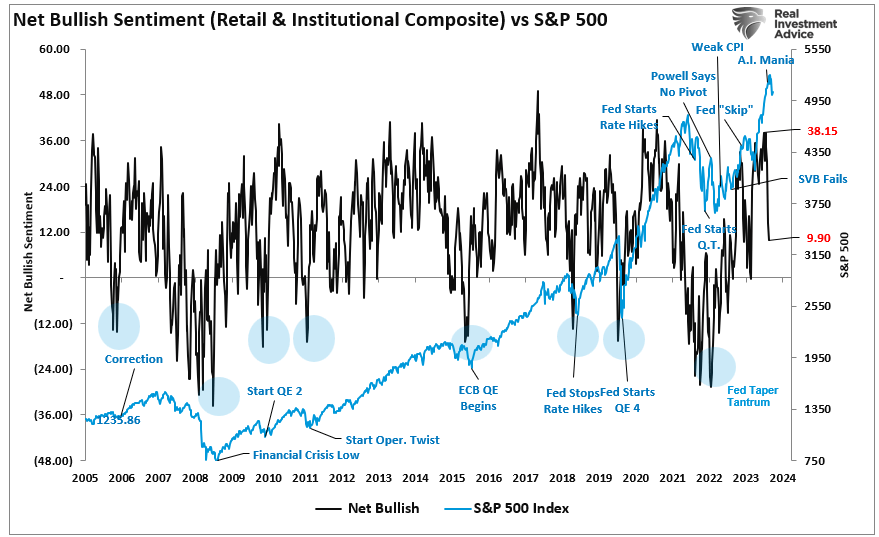

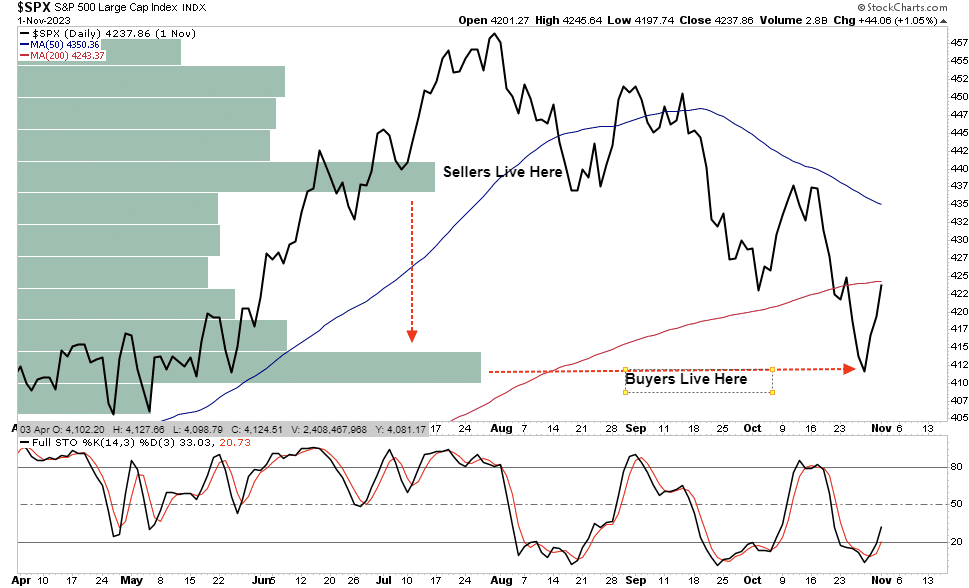

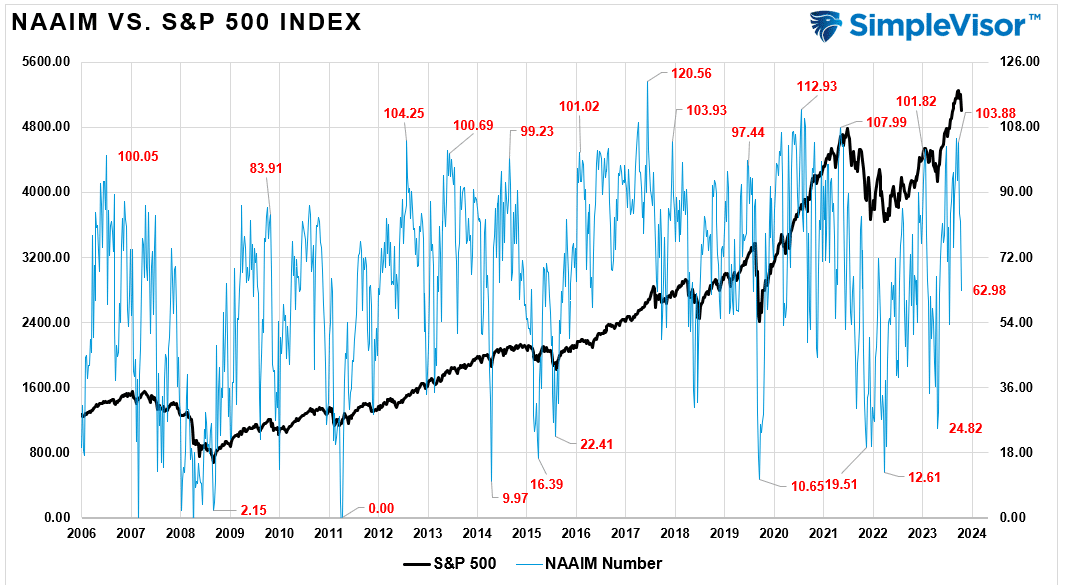

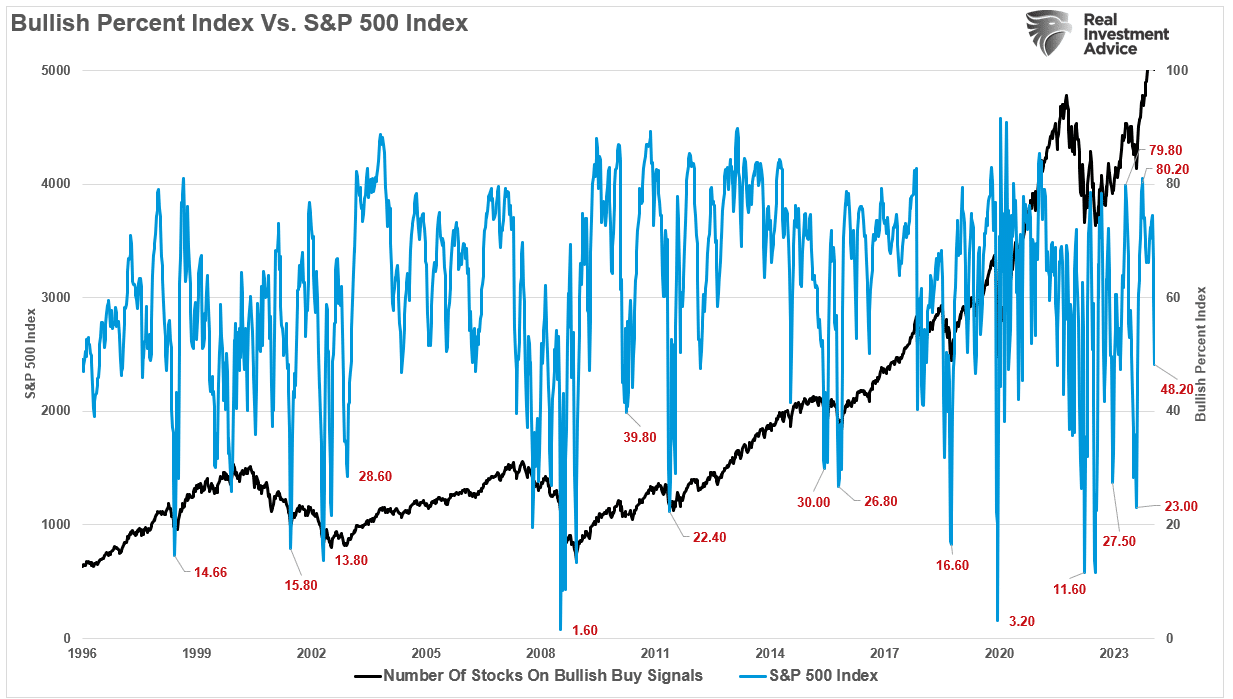

Bullish Sentiment Index Reverses With Buybacks Resuming

Over the last two weeks, the bullish sentiment index has reversed from extreme greed to fear. The composite net bullish sentiment index, comprised of professional and retail investors, fell from 38.15 to 9.9 in two weeks. The previous drop between July and October last year was similar and marked the bottom of the correction.

While the bullish sentiment index can indeed fall further, what is notable is the sharp reversal of market “exuberance” in such a short span. However, as discussed in “Just A Correction,” there was a significant gap between buyers and sellers.

“However, at some point, for whatever reason, this dynamic will change. Buyers will become more scarce as they refuse to pay a higher price. When sellers realize the change, they will rush to sell to a diminishing pool of buyers. Eventually, sellers will begin to “panic sell” as buyers evaporate and prices plunge.”

Like clockwork, that correction came quickly, with the market finding initial support at the 100-DMA. With solid earnings from GOOG and MSFT, the market rallied to initial resistance at the convergence of the 20- and 50-DMA. It would be unsurprising if the market failed this initial resistance test and ultimately retested the 100-DMA soon. Such a pullback would solidify that support and complete the reversal of the bullish sentiment index.

“Whatever trigger causes a reversal in the bullish signals, we will act accordingly to reduce risk and rebalance exposures. But one thing is sure: investor sentiment is extremely bullish, which has almost always been a good “bearish signal” to be more cautious.

While we have warned of a potential correction over the past few weeks, it reminds us much of June and July last year, where similar warnings for a 10% correction went unheeded. We are now seeing many individuals ‘jumping into the pool’ in some of the most speculative areas of the market. Such is usually a sign we are closer to a market peak than not. As such, we want to make adjustments before the correction comes.”

Very quickly, as supported by the bullish sentiment index, those bulls are turning bearish and are now calling for a more profound decline.

While such is possible, I suspect most of this correction is complete for two reasons.

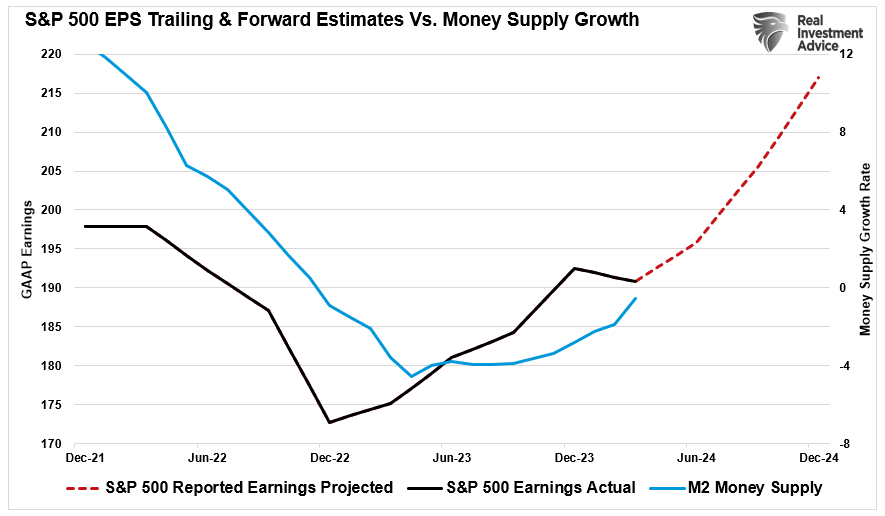

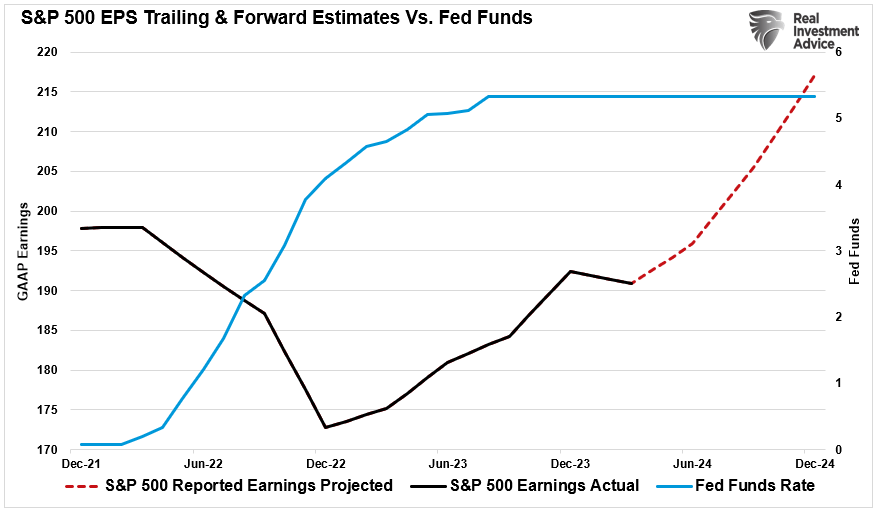

Earnings Continue To Remain Strong

The first reason is that despite higher interest rates, earnings growth continues to remain robust, at least among the “Magnificent 7,” where Google (GOOG) and Microsoft (MSFT), in particular, exceeded estimates by a wide margin. However, overall, and most importantly, earnings growth has continued since the October lows of 2022. Notably, the support for improving earnings comes from the increased fiscal policies such as the Inflation Reduction Act and CHIPS Act.

While those policies will eventually fade, making forward estimates subject to downward revisions, the current earnings environment remains relatively robust. Furthermore, forward estimates remain optimistic that the Federal Reserve will cut rates later this year, lowering borrowing costs and supporting economic activity.

Notably, the increase in earnings, at least for now, remains a strong indicator of rising asset prices. The risk of a deeper market correction (greater than 10%) is significantly reduced during previous periods of improving earnings. While such does not mean a deeper correction can not happen, historically, corrections between 5% and 10% in an earnings growth environment tend to be buying opportunities and limit deeper reversal in the bullish sentiment index.

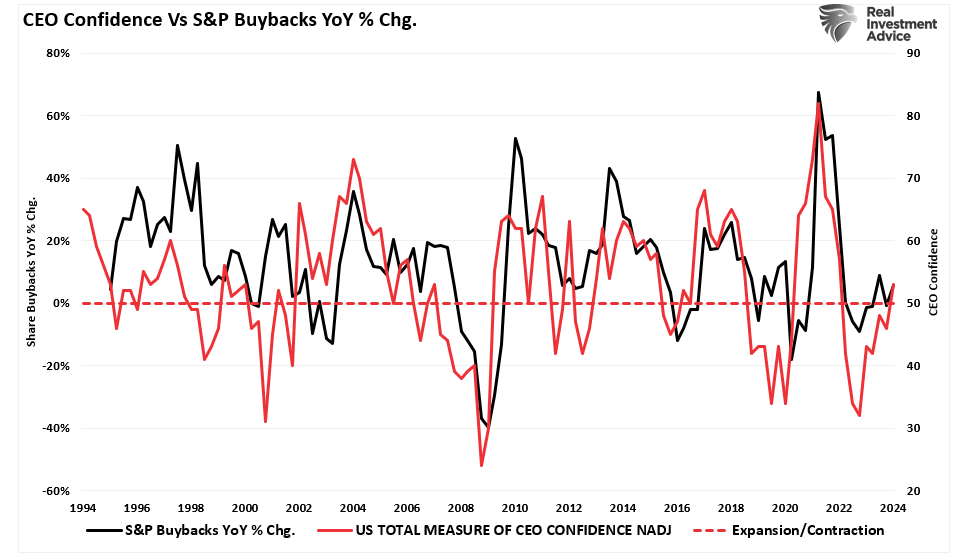

Improving earnings also precedes improving CEO confidence, which has provided pivotal support to financial markets since 2000.

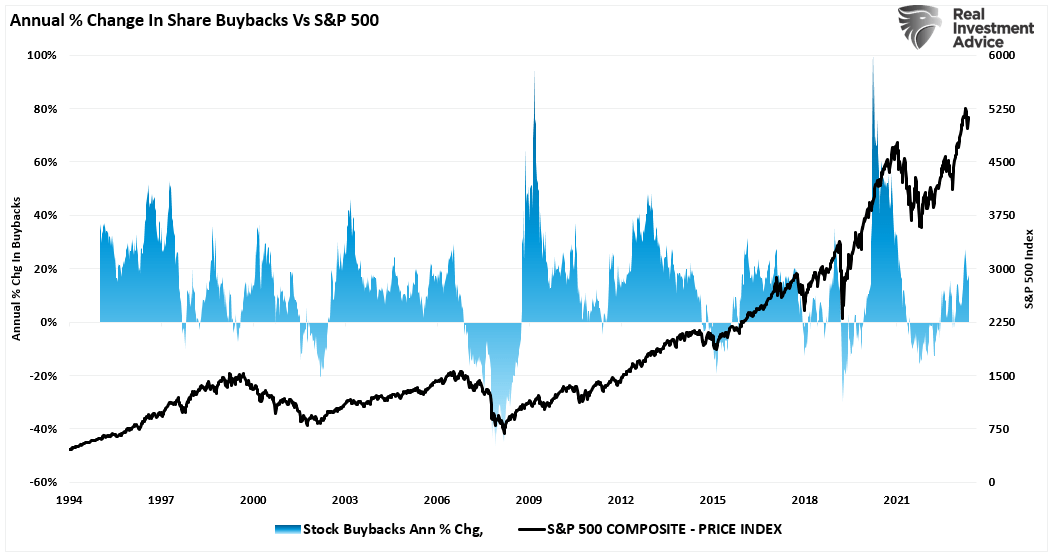

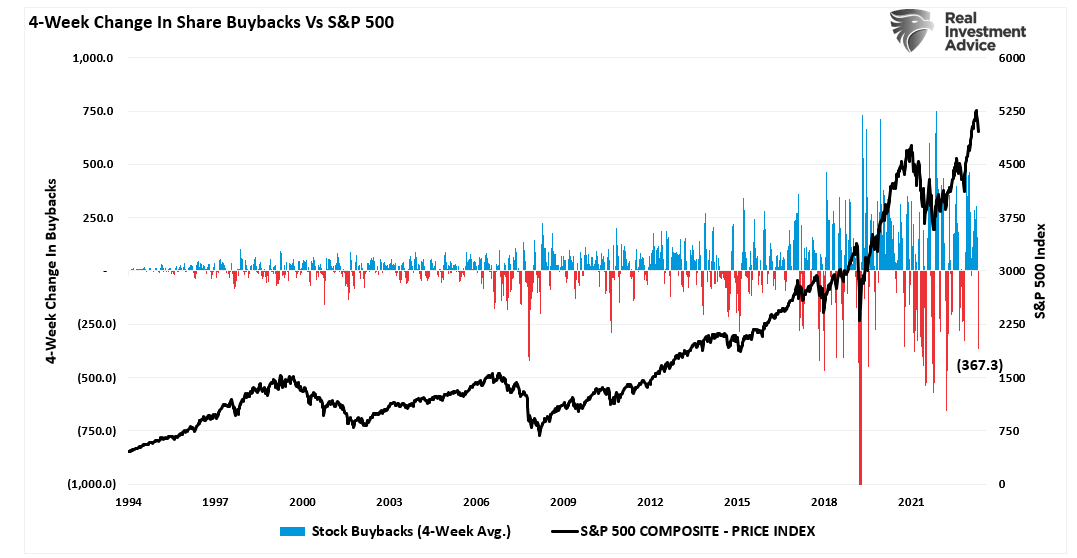

Buybacks Returning

We discussed the most critical reason we expected a market correction in mid-March. To wit:

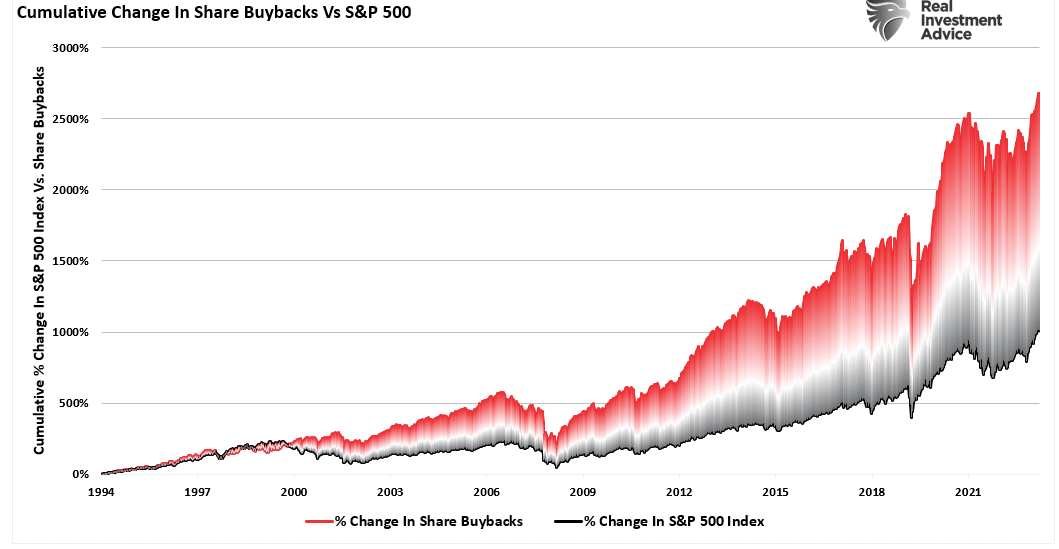

“Notably, since 2009, and accelerating starting in 2012, the percentage change in buybacks has far outstripped the increase in asset prices. As we will discuss, it is more than just a casual correlation, and the upcoming blackout window may be more critical to the rally than many think.” – March 19, 2024

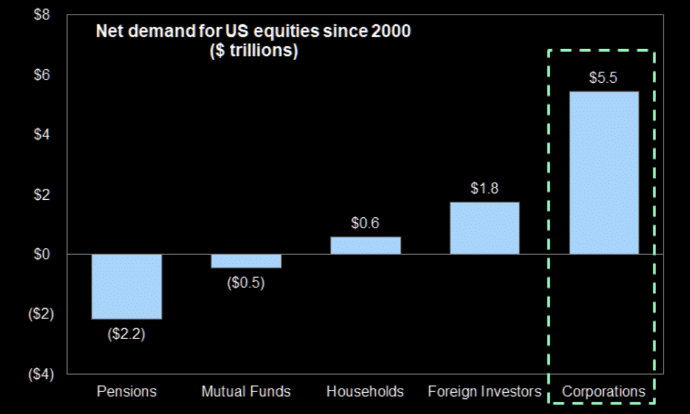

Furthermore, the “blackout” of corporate buybacks coincided with more extreme readings in the bullish sentiment index. Buybacks are crucial to the market because corporations have accounted for roughly 100% of net equity purchases over the last two decades.

Here is the math of net flows if you don’t believe the chart:

- Pensions and Mutual Funds = (-$2.7 Trillion)

- Households and Foreign Investors = +$2.4 Trillion

- Sub Total = (-$0.3 T)

- Corporations (Buybacks) = $5.5T

- Net Total = $5.2 Trillion = Or 100% of all equities purchased

Unsurprisingly, that blackout window coincided with a sharp contraction of more than $367 billion in buybacks over the last 4-weeks. Consequently, when you remove a critical “buyer” from the market, the ensuing correction is unsurprising.

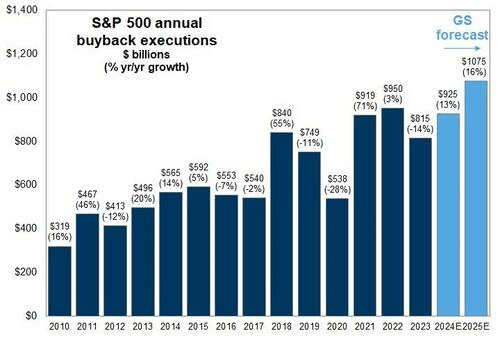

However, corporate share buybacks will resume in the next couple of weeks, and with more than $1 trillion slated for 2024, many buybacks remain to complete. Such is particularly the case with Google adding another $70 billion to that total.

As noted above, improving earnings and a decent outlook for the rest of this year also boost CEO confidence. (If you don’t understand why buybacks benefit insiders and not shareholders, read this.)

With robust economic activity supporting earnings growth, that improvement boosts CEO confidence. As CEOs are more confident about their business, they accelerate share buybacks to increase executive compensation.

The liquidity boost from buybacks and stronger earnings will likely provide a floor below the market. This doesn’t mean the current correction doesn’t have more work to do. However, it is unlikely that it will resolve into something more significant.

At least for now.

The post Bullish Sentiment Index Reverses With Buybacks Resuming appeared first on RIA.

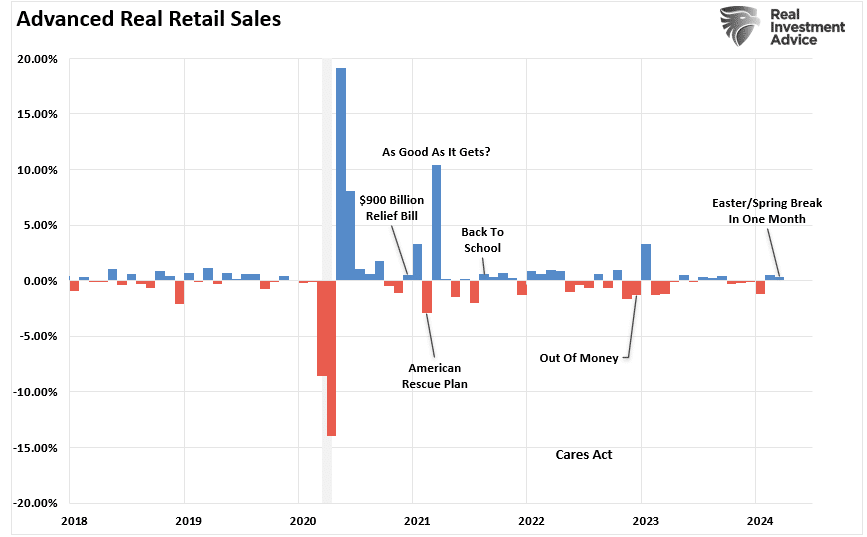

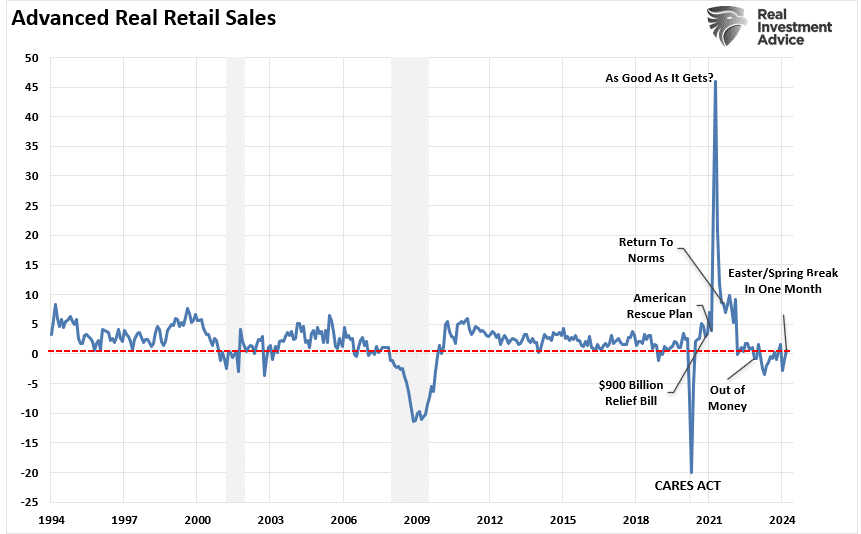

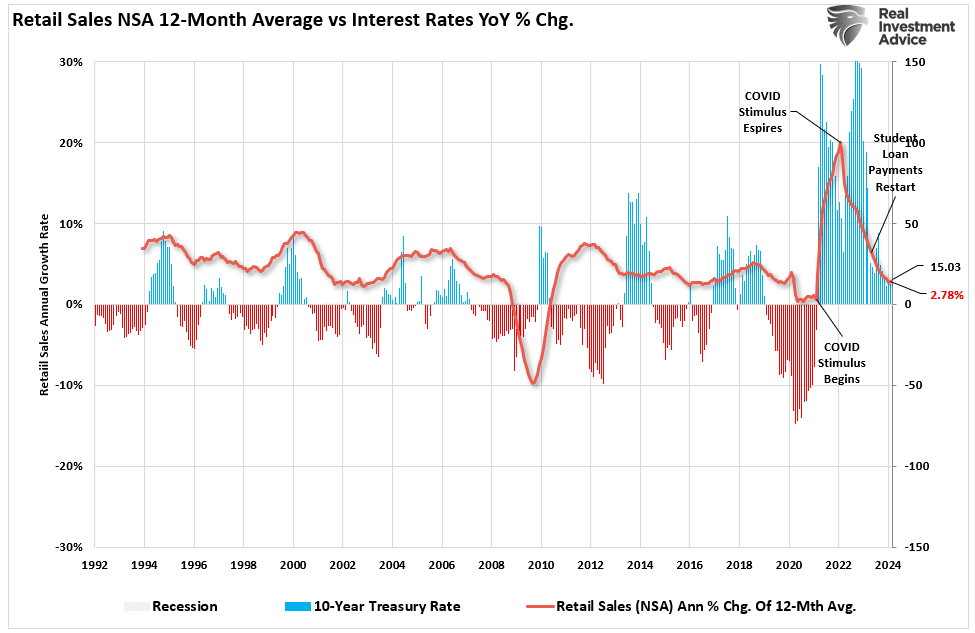

Retail Sales Data Suggests A Strong Consumer Or Does It

The latest retail sales data suggests a robust consumer, leading economists to become even more optimistic about more robust economic growth this year. To wit:

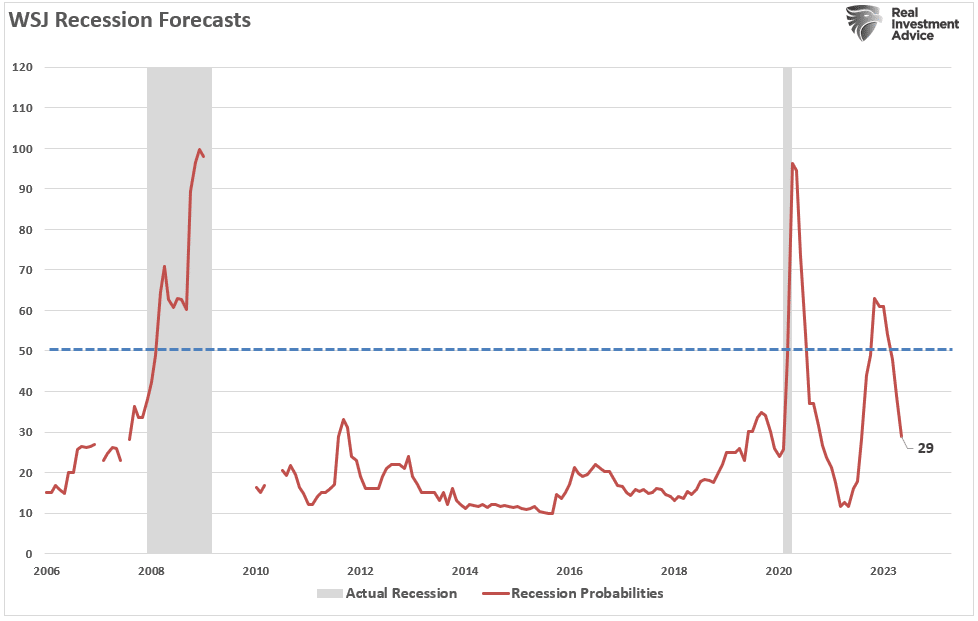

“It has been two years since forecasters felt this good about the economic outlook. In the latest quarterly survey by The Wall Street Journal, business and academic economists lowered the chances of a recession within the next year to 29% from 39% in the January survey. That was the lowest probability since April 2022, when the chances of a recession were set at 28%.

Economists don’t think the economy will get even close to a recession. In January, they, on average, forecast sub-1% growth in each of the first three quarters of this year. Now, they expect growth to bottom out this year at an inflation-adjusted 1.4% in the third quarter.” – WSJ

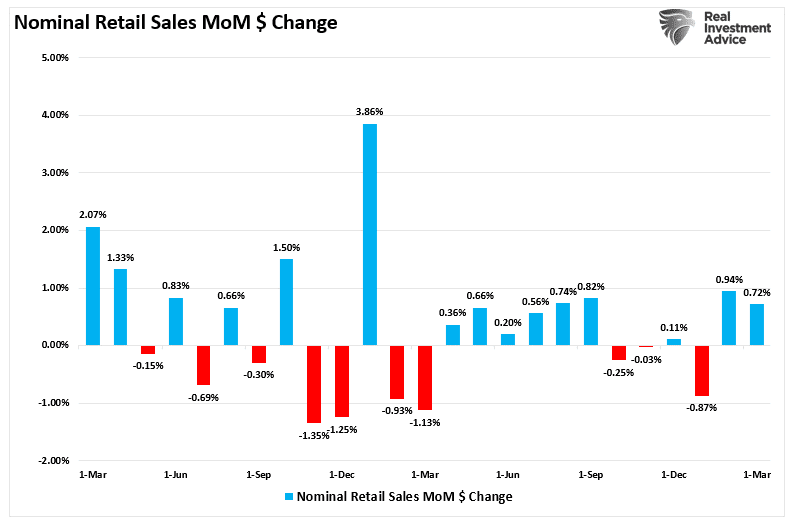

According to the March retail sales data, consumer spending added “fuel” to economists’ exuberance about this year.

Rising inflation in March didn’t deter consumers, who continued shopping at a more rapid pace than anticipated, the Commerce Department reported Monday. Retail sales increased 0.7% for the month, considerably faster than the Dow Jones consensus forecast for a 0.3% rise though below the upwardly revised 0.9% in February, according to Census Bureau data that is adjusted for seasonality but not for inflation.” – CNBC

The chart below shows the monthly change in the retail sales data over the last two years.

While mainstream economists trumpeted the strength of the consumer, the March retail sales data had some interesting points worth noting.

First, retail sales data was extraordinarily weak from October to January, the traditionally strongest shopping months of the year. That period included Halloween, Thanksgiving, Christmas, and NYear’sr’s. So, to some degree, the strength of spending over the last two months is unsurprising as, eventually, consumers need to buy goods or services previously postponed.

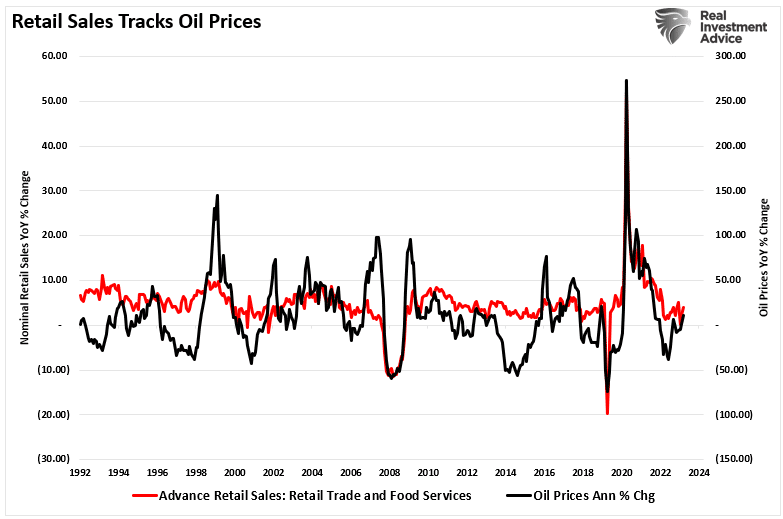

Secondly, while the March retail sales data was strong, it was weaker than February. However, March contained two significant spending periods, Spring Break and Easter, which generally don’t occur. Since Spring Break and Easter are considerable travel and shopping periods, it is unsurprising that the retail sales data increased with oil prices rising. As shown below, there is a very high correlation between nominal retail sales and oil prices.

Paying More For The Same Amount

Economists often overlook another important point about the retail sales data. As noted above, the March retail sales report was NOT adjusted for inflation. Furthermore, the report is in nominal “dollar volume” and not the amount of goods or services sold. Oil and gasoline prices are an excellent example of the issue with the retail sales data.

Let’s assume you own a car with 18-gallon fuel tank. Your daily activities are mostly going to work, going to the grocery store, eating out, having entertainment, etc. As such, you consume one tank of gas each week. Here is the math:

Week 1: 18-gallons of gas @ $3/gallon = $54.

That week, the store adds $54 to the monthly retail sales total for selling 18 gallons of gasoline. However, the price will increase to $4 per gallon next week.

Week 2: 18-gallons of gas @ $4/gallon = $72.

Here is the question.

While the retail sales data increased by $18 in week two, did the consumer purchase more gasoline? In other words, if the economy’s strength is ultimately measured by how much we produce (gross domestic product), then does spending more for the same amount of goods or services equate to a stronger economy?

The picture is quite different if we adjust the nominal retail sales data for inflation. Again, it is unsurprising that even on an inflation-adjusted basis, retail sales rose in February after declining for four months previously. However, with March containing Spring Break and Easter, the data suggests a weaker consumer that headlines tout.

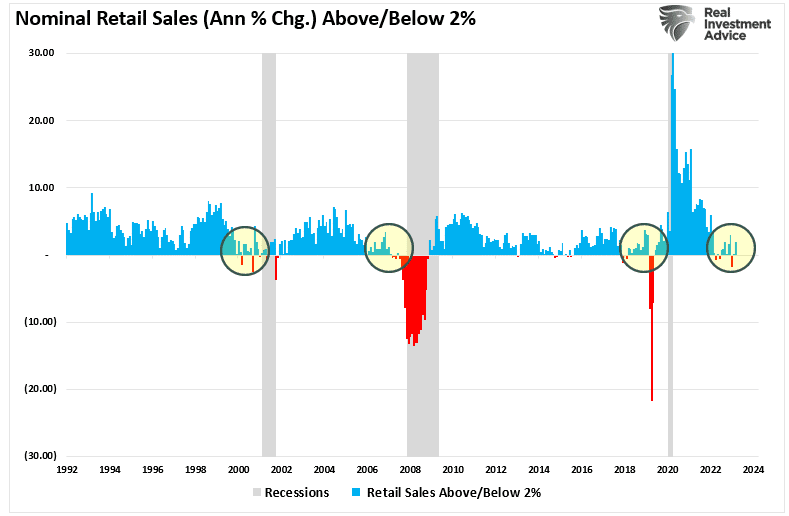

It is worth noting that retail sales data is not very useful in determining whether the economy is nearing a recession. As shown below, an annual growth rate of 2% has been a good marker for economic growth. As such, retail sales should grow at roughly 2% annually as well, given that personal consumption expenditures comprise approximately 70% of the economic equation. However, other than 2007, retail sales did not clarify economic strength.

In other words, spending more for the same amount of goods and services is not a sign of economic strength.

Economic Forecasts Tend To Be Erroneous

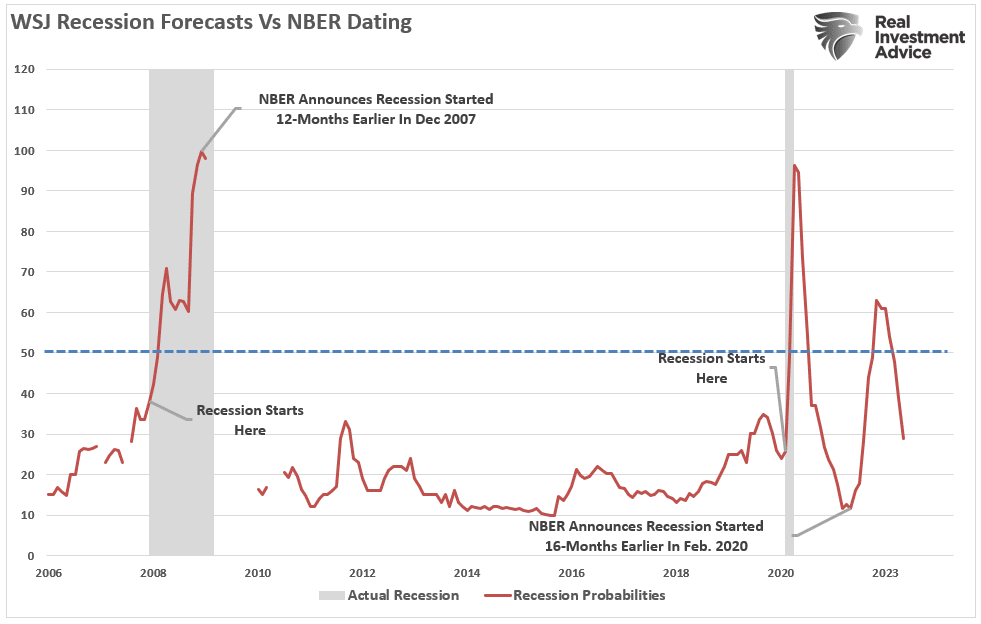

Furthermore, while the recent nominal sales data was robust, it is crucial to remember the economic data has a significant lag. Each of the dates below shows the economy’s growth rate immediately before the onset of a recession. You will note in the table that in 7 of the last 10 recessions, real GDP growth was running at 2% or above. In other words, according to the media, there was NO indication of a recession. But the next month, one began.

Crucially, I am not saying a recession is starting next month. However, I suggest that relying heavily on one month’s retail sales data to claim the economy avoided a recession is not likely ideal. Let’s revisit that chart of the WSJ economic forecast. I have added two notations: the start and end of recessions and when the NBER officially dated that period. As shown in both previous recessions, WSJ economists had a very low probability of the economy entering a recession just before it occurred.

The reality is that on an inflation-adjusted basis, the retail sales data suggests the consumer remains weak. While spending more to buy the same amount of goods or services may look good on paper, the average household has less money to spend elsewhere. As shown, the annual rate of change in real retail sales is near some of the lowest levels outside of a recession.

Lastly, consumer credit supporting retail sales will become more problematic with rising interest rates. Higher interest rates tend to reduce the average growth rate of retail sales data.

Our advice is to remain cautious about economic exuberance. Those forecasts are often disappointing.

The post Retail Sales Data Suggests A Strong Consumer Or Does It appeared first on RIA.

Overconfidence In NFL Drafts: A Lesson For Investors

Most NFL general managers (GMs) are optimistic and displaying overconfidence today as they prepare for tomorrow’s NFL draft. The draft is a once-a-year opportunity for GMs to acquire talent.

Like investors, GMs often think they are smarter than their competitors, aka the market. Yet, they frequently have similar mindsets and follow the same narratives that drive their competition.

As we will share, overconfidence and groupthink among football GMs and investors are behavioral flaws that often harm performance. Having the tools and strategies to mitigate our behavioral traits is extremely valuable and can lead you to better returns.

Overconfidence In The NFL

Four of the first five picks in the draft are expected to be quarterbacks. Not only is the quarterback the most important position on the field but this year’s draft is hyped as having several future greats.

Based on data from Warren Sharp, an NFL analyst, most of the quarterbacks taken in the early rounds will be average. His Fox Sports article entitled The success rate of first round QBs makes Lamar Jackson’s case for him, quantifies just how poor the odds are of drafting the next Super Bowl-winning quarterback.

There have been 38 quarterbacks drafted in the first round since 2011, the year the NFL changed the collective bargaining agreement.

These 38 first-round quarterbacks have made a total of 1,909 starts. Their record? 1034-1035-7.

He claims that of those 38 quarterbacks, only one, Patrick Mahomes, has won a Super Bowl. Furthermore, of the 28 from that group who are no longer on their initial contracts, the average time they were a starter was a mere 3.4 years.

Despite the proven mediocrity of quarterbacks taken in the first round, we have little doubt that overconfidence will be on full display by the GMs drafting quarterbacks with their top picks after they make their selections.

Groupthink In The NFL

This behavioral trait arises when people seeking conformity think and act similarly. Typically, groups reach a consensus opinion without proper evaluation and with minimal alternative viewpoints.

For instance, it is widely accepted that the four quarterbacks likely to go in the top five, Williams, Daniels, Maye, and McCarthy, will be excellent pros. Most NFL analysts offer differences between the quarterbacks but praise the physical and mental traits they believe will make them NFL starts. Very few analysts have poor ratings on any of those four quarterbacks.

Choosing one of the four quarterbacks is comforting. Simply, GMs have cover if their pick is a dud. Who could have known? Every expert thought he would be a superstar!

Investor Overconfidence And Groupthink

Replace players with investment ideas and GMs with investors. The overconfidence and groupthink mentality impacting GM draft day decisions are similar to those investors always face.

We quantified the odds of GMs picking above-average quarterbacks earlier. Per DFA Funds, the odds of an investor outperforming the market are even more daunting.

We saw from the data above that an investor has about a 75% chance of underperforming the market in any given year, which means you have a 25% chance of beating the market in any given year.

The message to take away from that statistic is to leave your confidence at the door!

Regarding groupthink, most investors, like GMs, find comfort in knowing that many other investors are doing the same thing. Market narratives are a form of groupthink. Narratives help explain market movements and trends. Often, a narrative develops after a trend has started. In other words, rightly or wrongly, the narrative is the rationale.

Today, narratives appear to be quicker to form and longer lasting. Maybe the advent of social media has allowed for their quicker dissemination and growth.

Narratives describe the mindset of a group of investors. When you unknowingly invest based on a narrative, you are likely setting yourself up for failure.

Strategies To Combat Behavioral Traits

Appreciating that GMs have a one in three chance of successfully using a precious top-five draft pick on a quarterback or that only a quarter of investors will beat the market, we best have tools to manage our behavioral traits and improve our odds of success.

Zig

Warren Sharp advises GMs to “zig while others zag.”

To zig is to have a contrarian mindset. For instance, it’s important for your portfolio to have popular stocks leading the market higher. But at the same time, understand that confidence can wane quickly, and a new set of stocks will take the throne soon enough. Don’t overstay your welcome in a narrative.

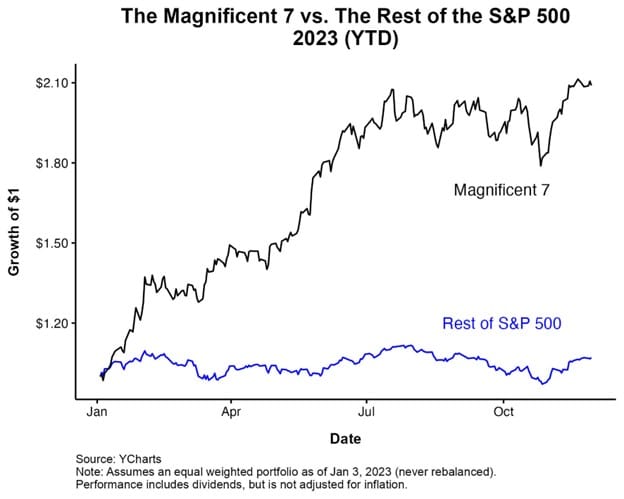

It wasn’t that long ago that the Magnificent Seven stocks were all the rage. Their returns handily beat almost every stock and index. Holding a meaningful subset of the seven stocks was vital to keep up with the broad market indexes. However, the Magnificent Seven’s period of outperformance has either ended or is on pause. But, the narrative still thrives, and whether it’s already happening or will occur shortly, investing in the aged groupthink will catch many investors offside.

Take Profits

It’s hard to sell when others are buying. Still, when the narrative-driven stocks fall out of favor, the prior profits and reduced position sizes will bolster returns and lessen the risk of underperforming the market.

Appreciating what the market, and not popular narratives, tell you is equally vital. For instance, have you noticed that utilities and energy are the best-performing sectors lately? Those solely holding the Magnificent Seven and neglecting other sectors are falling behind.